Podcast: Play in new window | Download

There are some insurance agents who suggest the rate of return of a whole life insurance policy doesn't matter. This curious claim is pervasive within the self-banking (e.g. Infinite Banking®, Bank on Yourself®, etc.) circles. So with piqued interest, exploring this notion seems appropriate.

Does the rate of return not matter? Is it all a ruse? If it doesn't matter…what does?

“That” Rate of Return Doesn't Matter

I'm going to tell most of the punch line before the joke on this one (but don't worry, there's plenty of reason to stick around until the end…you'll learn something). The argument that rate of return doesn't matter falls into two potential camps. One camp intends it as a way to call your attention to something you likely overlooked. The other camp…well it's much more sinister.

In the spirit of positivity, let's begin with the much more virtuous reason a life insurance agent might exclaim that rate of return doesn't matter.

In truth, the agent doesn't really mean that rate of return doesn't matter. He/she really means that the specific rate of return doesn't matter.

Let's use an example to put this one into context.

Suppose you sit down with Larry the insurance agent who shows you a proposal to buy whole life insurance. You look at the many pages of this proposal and glance through the numerical delineation of future projected values. At 40 years old, you're particularly interested in the cash value in 25 years when you plan to retire.

Looking at the numerical breakdown of the policy you note that in year 25 the policy will have cash value such that it achieved a 4.5% Internal Rate of Return. You can think of this as the annual interest rate you'd need to earn if you put the premium of this whole life policy somewhere else to arrive at the same value reported as the policy's cash value.

“4.5%?” Your question with a hint of disappointment.

“I can do better than that elsewhere,” you tell Larry.

But Larry, not willing to give up so easily, quickly shoots back that the rate of return of your policy doesn't matter. What he really means is that the rate of return of your policy at this specific juncture isn't all that important.

You see, whether you accumulate the same balance in a stock portfolio, real-estate, or wherever else you plan to save money is largely immaterial without a specific plan about how you go about turning that pile of money into retirement income (or whatever the intended use of the money is).

Larry is alluding to the fact that simply looking at the rate of return at this seemingly arbitrary dot in your timeline might just overlook some very crucial planning you need to do about how you will actually extract value from the assets you seek to accumulate. Not all assets work the same way when it comes to converting them to buying power, and Larry wants you to understand this in a way that doesn't feel like Ben Stein just showed up in your dining room and began a presentation on the significance of the Mandelbrot Set.

So what Larry really means is this specific rate of return doesn't matter as much as you might think it does. There is a much bigger set of data you must look over to arrive at the true rate of return of this decision set against an equally larger set of data you must consider for whatever alternatives you think you might pursue.

When working through this problem, you'll likely find that whole life insurance looks darn good compared to your other options. But myopically looking at year 25 and thinking there are other options that might achieve a larger account balance by then, might lead you to forego a lot of future buying power.

Whole Life Rate of Return Magician

While I find it perfectly reasonable to make Larry's appeal, there is another flavor of the “rate of return doesn't matter” claim that causes considerable concern. This suggestion isn't really an allusion to a bigger world of thinking. Sadly, it's more a tool used to draw your attention away from unflattering facts in the hopes that you'll be wooed by the idea so much that you move forward with a purchase.

For example, let's assume you are again sitting down with an insurance agent (this time Ned…Bing!). Ned presents a similar presentation with many pages and a numerical breakdown of future projected values. You again look at year 25 interested in the results by that point and note the 3.5% Internal Rate of Return.

Not sure what to make of this you ask Ned if this is the best return you can achieve on a whole life policy. Ned perks up and informs you with great enthusiasm that the rate of return doesn't matter.

Ned continues to explain that because you are buying whole life insurance and whole life insurance is a special asset that provides “uninterrupted compounding” and the ability to take your money out of the garage, drive it around town, and then put it back when you're done with it the rate of return isn't important. It's the special powers of whole life insurance that matter.

These references…in case you're new to this…relate to the various platitudes used to sell the concept of self-banking. In truth, they aren't hooey. But we run into a problem when positioned in a way to suggest that they are always superior to any other feature of any other asset and therefore make whole life insurance unquestionable.

In this context, Ned either knows or has reason to believe that you could do better with another whole life product. But Ned doesn't want to sell you that whole life product because he's not contracted with that company, will make less money in commissions, or might miss out on a production bonus if he doesn't sell you this specific whole life product.

So, he crafted a clever plan to redirect your attention away from a truth he cannot argue in his favor. It's a nifty sleight-of-hand that serves as a great reminder. When it looks like magic might be at play…there is no real magic…but there are real magicians.

Why the Rate of Return Does Matter

Whole life insurance can provide numerous benefits that can dramatically improve your financial planning. It can accomplish a myriad of tasks. When designed and executed correctly, one can use whole life insurance to vastly grow his/her wealth.

While I'm not an obligate self-banking practitioner and have no direct relationship with any of the marketing companies created to promote the mainstream concepts of self-banking, I'm more than willing to agree that they all have some degree of truthfulness behind their claim to use whole life insurance to build wealth faster and more efficiently.

But if we believe in the goal of self-banking, then we must also agree that as much as possible is ultimately the best approach. This obviously suggests that rooting out the best performing whole life product for rate of return on cash value is ideal. Suggesting otherwise with some twisted suggestion that the rate of return doesn't matter shows us the agent isn't really committed to helping people through the virtues of such a concept.

It's sort of like the Primerica buy-term-and-invest-the-difference debate. If we agree that such a strategy is the panacea, why are they not looking to sell the cheapest absolute term life insurance they can find? Perhaps it's because the argument is more about how they disrupt someone's life in order to make a sale and not an absolute adherence to what they preach…

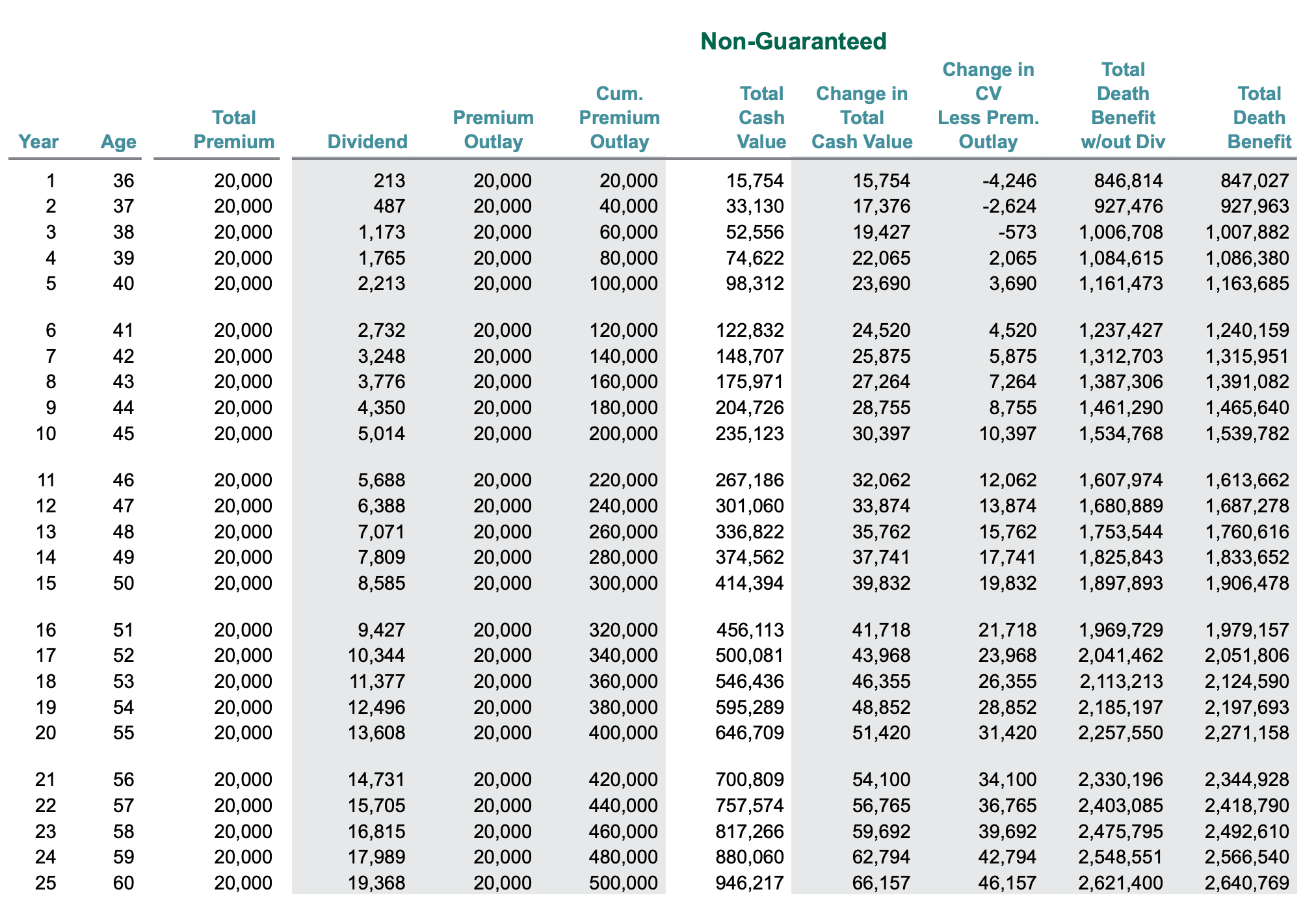

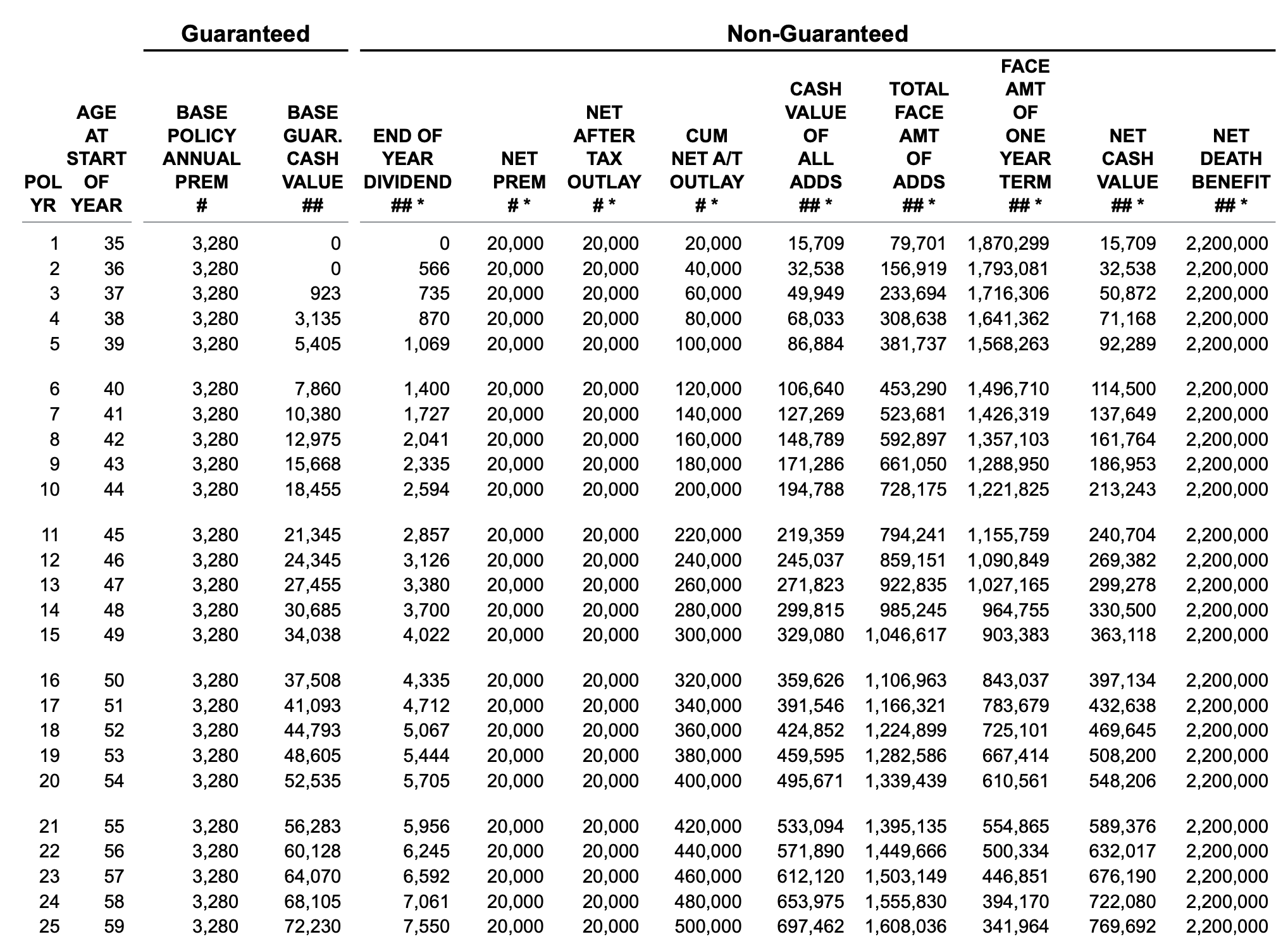

Consider these two examples of policy illustrations:

They are both whole life policies. Both are blended whole life policies. They can both be used for self-banking. But one has $176,525 more cash in year 25. That makes a meaningful difference in the wealth-building and overall self-banking someone can do with the first policy versus the second policy. The rate of return certainly matters so be sure you vet your whole life selection a bit.

So yes the rate of return matters. But the rate of return is a complex discussion and way more nuanced than a lot of people realize. If you hear someone claim it doesn't matter, be wary, but not immediately dismissive. And please consider the overall value certain investment/savings plans can provide for you over your entire life.