Our regular readers know that we have a certain love/hate relationship with the whole Bank On Yourself®, Infinite Banking, and their various iterations. We certainly enjoy their work in furthering the cause, the notion that one really can use cash value life insurance as a means to accumulate wealth and that the products actually do make for an incredibly stable and predictable asset.

But…

Our good friends at their respective camps also tend to make a few claims that we think are a tad over the top. While the notion that whole life insurance and/or universal life insurance can be used as a means to acquire the funds for major purchases, and that the use of life insurance to do so has a much smaller economic impact on the individual are certainly all valid, we’ve pointed out numerous times in the past that these systems are totally off base in their suggestion that one can enrich his or her life further by virtue of using their life insurance policy for policy loans. In other words, it’s good…but it’s not that good.

We’ve been asked quite a few times to put the logical discussion into more concrete terms with a numerical example. Our delay in doing so has nothing to do with our unwillingness, and everything to do with lack of time to focus energy on putting the numbers together, that all comes to an end today.

Spend Money, Get Rich!

It sounds like a dream combination. Make money for spending money? Where do I sign up? But surely most of you would raise a suspicious eye to any claims that you can have your cake and eat it, too. But this is precisely what some would have you believe when they make statements like Spend and Grow Wealthy®. And for a number of years now, certain advisors of respective programs have carried a set of ledgers around to paint the picture of just how one goes about becoming a millionaire by visiting Saks and Bloomingdales.

How does one Become a Millionaire by Spending Money?

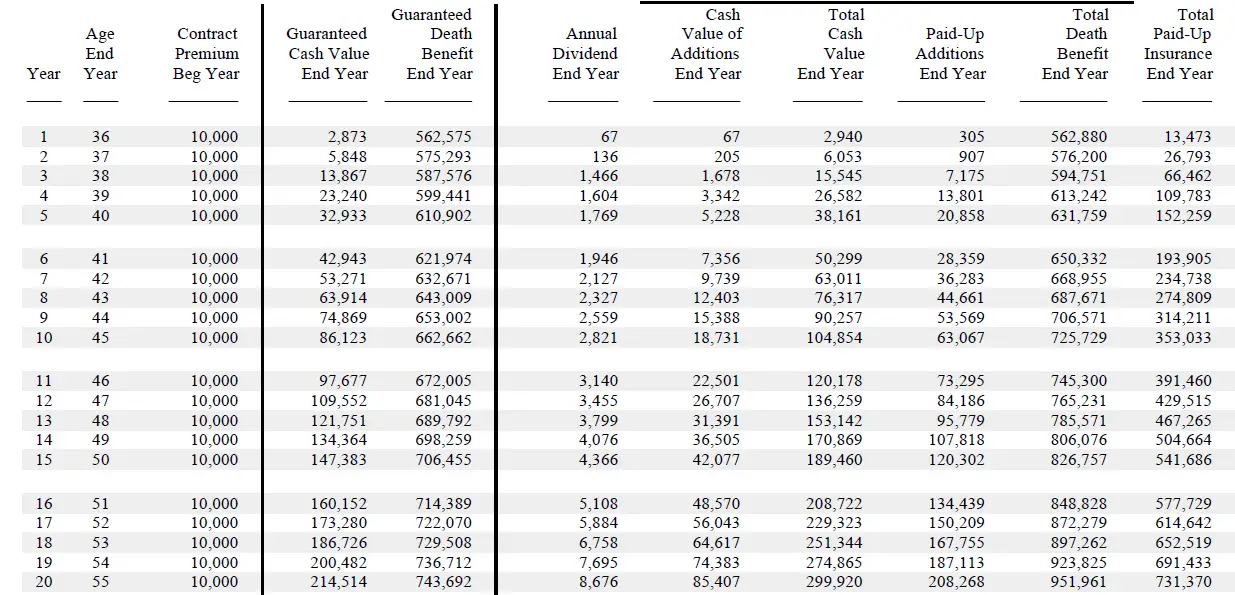

Let’s go through the motions, shall we? We’ll start with a basic whole life insurance ledger. We’ve chosen to do this with a well-known issuer of participating whole life insurance and specifically a company that issues non-direct recognition contracts. The infinite banking et. al. crows would have you believe this is the only way to go. We’d suggest there may be some nuance to that suggestion, but as you’ll learn in the next few minutes, they don’t exactly have a penchant for details.

We’ll start the policy with a planned outlay of $10,000. For simplicity’s sake, we haven’t blended the policy with term insurance, but we have thrown a paid-up additions rider on, the premium breaks down to 60/40 base whole life insurance to paid-up additions, this is actually pretty close to what a lot of the infinite banking crowd would do if you asked them to put a policy together for you.

The ledger looks as follows:

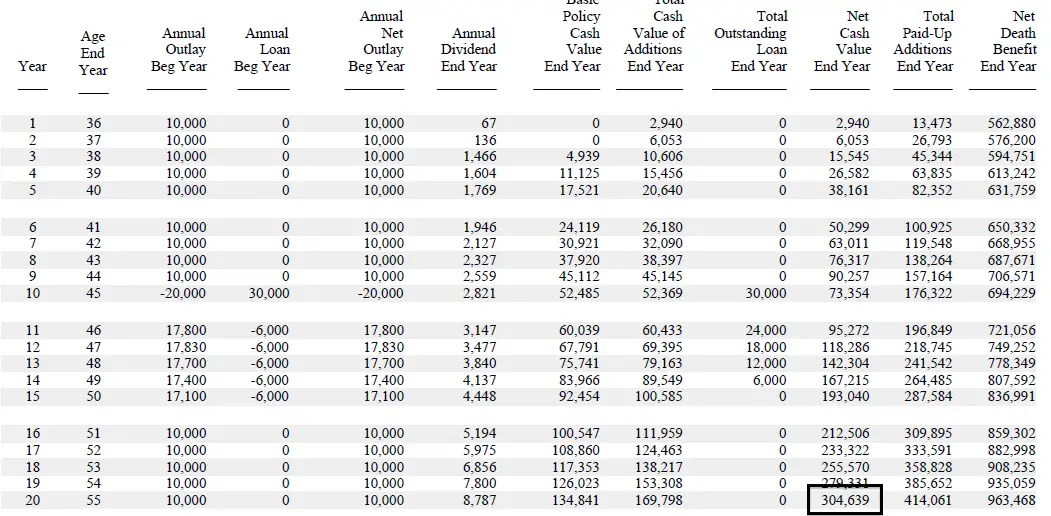

Now let’s assume that in year 10 (chosen for no real reason in particular) we’d like to take out a $30,000 loan. The reason for that loan, if you really like the background story and if you found Pam Yellen’s book the least bit interesting you probably do, is so we can buy a car. Hell let’s put a bow on this thing and get real descriptive.

You aren’t just buying any car, you’ve found yourself one of those sweet post facelift 2011 Saab 9-5’s that never found its way outside of the dealership sales lot. And now at a $15,000 discount from the sticker, it’s time to buy. Now, I know what you’re thinking. Who would be dumb enough to buy an automobile from a car company that’s now three years defunct? There couldn’t possibly be someone dumb enough to do that! But no worries, we’re going to gamble on the Swedish Automobile one last time and get rich doing it.

The Numbers

Our chosen whole life policy has an interest rate of 5%, so we’ll follow R. Nelson Nash’s advice and charge ourselves an extra 2%. According to the TI-83 Plus, this will require repayment of $6,800/year if we plan to pay the loan back in 5 years—I rounded up to the nearest 100th.

You may notice that there are some idiosyncrasies to the examples, chiefly that we didn’t make any loan repayments in the first year. This is due to illustration software limitations. There’s nothing that would stop someone from repaying a loan in the first year, the software just doesn’t let us show that.

First if we do this the old fashion way, simply pay the interest due on the policy loan, we’ll end up with the following result:

This simply shows us that if we repay the loan in 5 years at $6,800/year we’ll have exactly the same amount of money if we didn’t take the loan. Go ahead and compare year 20 (and sorry that I copied some of these going out to year 25 on accident) and compare to the original ledger, this is non-direct recognition at work.

But this process doesn’t follow the guidance of Banking on oneself. No, in order to do that, you should place that extra interest not into your repayment plan, but rather into the paid-up additions rider. If you do that, your policy will blow your hair back as if that 9-5 came in a convertible model (it doesn’t) as it speeds towards affluence. Now just a quick note, due to paid-up additions rider restrictions, we couldn’t get the entire amount in there as we would have wanted to in the first year, but that’s okay because our outlay remains pretty much the same since we’ve opted to pay loan interest instead of capitalize it if our loan repayment isn’t large enough to cover it.

And here’s the ledger to prove it:

We can plainly see that come year 20, you have more money. And here is where the infinite banking peeps tell us they’ve proved their concept. Put down the book, write the check, and let’s get you on the cover of Millionaire Weekly.

But what if…

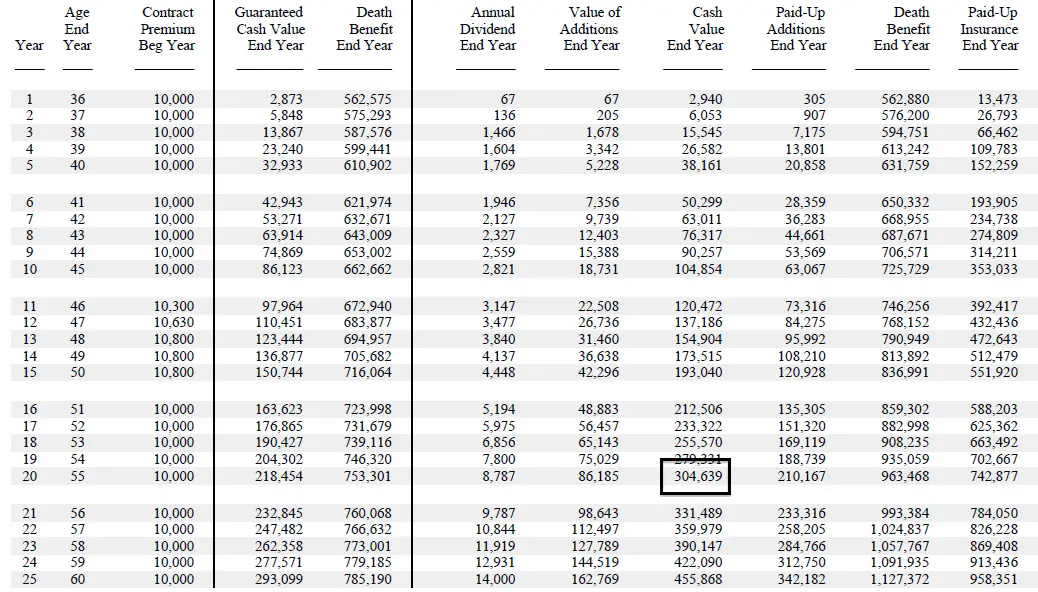

If this thought hasn’t crossed your mind yet, let us introduce it. What if you didn’t take the loan and you simply put the extra money into the policy? We’ll, here’s what that looks like:

Oh dear, it turns out this method works just as well for supercharging your policy, and your outlay is less (i.e. higher internal rate of return on cash value) because you didn’t take out a loan. Notice also that we didn’t change anything regarding this paid-up additions rider vs. the loan scenario. It’s the same amount of paid-up additions. We just don’t have an actual loan payment to make.

Additional Complications

There are two additional problems with the suggestion that you place more paid-up additions into the policy as pretend interest when you take out a loan.

- If the policy is already being funded at or near the modified endowment contract limit, the chances that you’ll be able to place additional premiums into the policy are small.

- All of the non-direct recognition carriers have much more rigid paid-up addition rider policies, meaning increasing the rider to account for fake interest is a bit tougher than you might first realize, this is the reason we can’t show it as high in the example we used as we would have liked.

Still some Important things to keep in Mind

I’m not here to torpedo that entire idea, just to bring a little sanity to it. You aren’t going to spend and grow wealthy, and you aren’t going to directly receive every dollar you put into the policy loan interest payment back and then some. You will however be able to borrow money at a much lower economic cost than will likely be available to you elsewhere.

Also, the fact that you can acquire a loan at any time for any reason and have no set required schedule to pay it back makes this the most flexible access to capital I’m aware of. And since the cash in your policy stays put (meaning it continues to earn guaranteed interest and dividends, or just guaranteed and non-guaranteed interest if using universal life insurance) the ability to continuously grow your networth still exists.

But I can borrow against other accounts, like brokerage accounts and my real estate

Yes you can, and you can even apply a similar principle. However life insurance is infinitely more stable and predictable than the securities in brokerage account and real estate. Fluctuating account values can create margin calls, and real estate equity loans require credit worthiness and mortgage underwriting time.

Life insurance loans are lighting fast. In fact, I processed two for some clients just last week. In less than 30 seconds we had the request completed and they received their money in a couple of days.

We also have to keep in mind that a policy loan is a non-amortized simple interest loan. You pay principal down through the year, and once the policy anniversary comes up, the insurer will tell you what the interest due. You can decide to pay it, or capitalize it as part of the loan and continue paying as planned.

And don’t get hung up on the over ambitious one product love affair. Both whole life and universal life insurance will work just fine for this concept. You just have to pick the right product and design is properly.

So to reiterate, Bank on Yourself®, infinite banking, et. al. are commendable for their efforts to spread the word about what we can use cash value life insurance to accomplish. But we have to temper their claims to establish appropriate expectations. And you can’t get rich by spending money.

You nailed it with your last paragraph…”But we have to temper their claims to establish appropriate expectations. And you can’t get rich by spending money.”

This nails it for me. As an avid user of high cash value life insurance all the hype turns me off. I see it as a safe, tax advantaged place to store my money and if I need/want I can borrow against my cash value with some advantages I wouldn’t get from borrowing money from elsewhere.

Good post. It won’t make the “IB = free money!” crowd happy, nor will it please those who hate IB/whole life. I’d like to see a strong proponent of Nash/BOY respond, but won’t hold my breath.

Like Rick said, the banking aspect is a good tool of permanent insurance that you’ll never hear about from traditional financial planners. It’s not a money-making perpetual motion machine, though. I wish there was a program to compare policy loans vs. other loan sources, paying with cash, etc. I guess a lot depends on interest rates, dividends and individual circumstances, though.

If I take a loan out of a policy, will I be charged interest immediately? or only at the policy anniversary date?

Hi Brian,

This depends on the company with whom you have a policy. Some charge interest in advance, meaning they will assess the interest charge as soon as the policy is taken. Others charge interest in arrears, and will not charge interest until the end of the policy year on whatever amount is outstanding at that time.

I’m a little lost. In the last illustration where there was no loan but the increase via PUA is realized, how did that “overfunding” get in the policy? I can see that the annual premium outlay is increased slightly more than 10k in years 11-15, but how can that happen? I thought you could only pay in the premium amount. If the annual premium is 10k, and let’s say the MEC limit is 11k, then are you saying you can pay in up to that 11k limit (1k over premium)? And how did you direct that extra money to the PUA instead of the base premium? Please explain.

Hi Jimmy,

You can add additional money to a whole life contract so it is not correct that just because the premium is a given amount, that is all you can pay. This is additional payment is done through a paid-up additions rider and that’s exactly what we’re doing with the last ledger.

Okay. Just so I’m understanding correctly after reading the link you provided, you’re saying the policy is both directing dividends to purchase more PUAs and also has the PUA rider. Got it. So, then my question becomes: If you design a policy this way, unblended with a PUA rider that allows for a 60/40 base/PUA split premium allocation with dividends going to purchase PUA also, then how exactly can you squeeze in any more money? Aren’t the terms of the contract, like the PUA rider, fixed at issue and unchangeable (other than dropping it later on)? How can you make changes to increase cash flows to PUA after the policy is issued and in force? So if you design that policy in the manner described and the premium is 10k/year, but MEC limit is 11k, can you still pay up to just shy of 11k/year to “overfund”? Am I still missing something here?

Hi Jimmy,

Some PUA riders are fixed and cannot be changed or cannot be changed without additional underwriting to increase the premium.

But, other companies allow PUA’s to be changed (up and down) within a certain bound without restriction. So with this sort of contract, yes you could increase to that limit in any year you wanted and also pull back in any year you wanted.

Maybe I’m missing something, but one important difference I see between the two illustrations is the CAR. In the first one, not only have you “earned/saved” more money, but you own a car that you can use. In the second illustration you’d need to make extra “payments” to the policy as well as payments toa bank for a car loan just to get the same benefit.

Am I missing something?

Hi Kristen,

The point is that wether you buy the car or not you do not magically end up with more money by shear virtue of taking a policy loan. One can accomplish the same thing if they simply placed more money into the policy. A loan is not required and the outlay (i.e. out of pocket from the policyholder) is the same in either case.

Now if one wants to buy a car with a life insurance policy loan and replay the loan in this fashion, he or she is more than welcome to do so. Financing such a purchase in this fashion might be less costly than traditional bank lending and certainly comes with a multitude of flexibility that a traditional loan would never afford. However, and this is the key point not to miss, borrowing from the life insurance policy does not magically make you richer.

I’m currently studying both books from Nash and Yellen. As I understand it (correct me if I’m wrong), the interest(s) from the loan(s) is added to your cumulative outlay, thus increasing the dividend yields, thus buying more PUAR, which in turn leads to more death benefit and more Cash Value. So in effect, more loans equals more death benefit and Cash Value above and beyond the limitations of the initial Premium and PUAR contract. This has been the hardest part of the ‘banking system’ to understand. Am I in the right direction?

Hi Ven–your basic understanding is solid. The problem we have with this strategy is that there’s no magic in taking policy loans and paying them back with more money than you actually borrowed (as both Nash and Yellen recommend). Turns out if you pay more money into the policy, you have more cash value. You could do without taking a loan–that’s the crux of this post.

Also, I would add that if your policy is designed properly from the beginning, you really won’t have much room to pay more money into the policy as they suggest. If you design a policy to maximize cash value accumulation from the beginning, your total premium (base+term+PUAs) should be very close to the 7-pay premium. That means if you are not funding the policy right up to that 7-pay limit, you are paying for more death benefit than you need to avoid MEC status. The “extra” death benefit, in this case, would create a drag on the cash value performance.

What software did you use to create these models

Hi Alisha,

These are MassMutual policy illustrations using the NDR option for loans.