Back in 2011, when the world was very different than today, selling life insurance from home seemed like a crazy idea.

How do we know?

Because everyone that we spoke with about what we were doing and our idea to work with clients across the country told us it would not work. Those people would never trust paying large premiums on a policy that was offered to them from someone they couldn’t see or smell.

But in fact, this website started as an attempt to do just that…to attract clients that would be interested in purchasing life insurance. And that a vast majority of the business conducted would be done so in a virtual environment.

Until that time, our efforts to sell life insurance were largely conducted in face-to-face meetings, often in someone’s office or at their kitchen table in the evenings after they were done with their workday.

Is selling life insurance a good career opportunity?

That is the million-dollar question, isn’t it? Most people who sell life insurance from home certainly make it a career. To be honest, selling life insurance part-time seems like a difficult task as it is not the type of work that fits neatly into compartmentalized time blocks.

That is the million-dollar question, isn’t it? Most people who sell life insurance from home certainly make it a career. To be honest, selling life insurance part-time seems like a difficult task as it is not the type of work that fits neatly into compartmentalized time blocks.

Obviously, that will depend on what type of life insurance selling you decide to focus on for your career. Speaking from experience, the time and energy it takes to educate, guide, and direct the sale of blended (term riders with paid-up additions) whole life insurance policies or indexed universal life insurance would be tough to manage on a part-time basis.

Many times when you are designing a whole life insurance policy, for example, there is an extensive phone call or web conference that needs to take place. As you may or may not know, these types of life insurance have illustrations that must be signed and acknowledged when applying.

Most people, want to understand what is going on before signing it, which is reasonable. Remember, with cash value life insurance policies many times people are spending many $20k+ every year in premium and they plan to do it for many years.

That’s a substantial commitment and they need to be sure that they understand all the pros and cons of the particular whole life policy you are recommending to them.

The same can be said for index universal life insurance—some even claim it requires more explanation. That’s a matter of opinion but it requires a slightly different discussion than whole life for sure with just as much detail for clients to reach a certain comfort level to make a final decision.

Can you really make money selling life insurance?

Yes, you can definitely make money selling life insurance from home. It’s a relatively simple business depending on what type of life insurance you are selling and the needs of your clients. One thing that has not yet been discussed in this article is that many people who sell life insurance from home are focused on selling term life insurance.

Selling term insurance from home certainly is less complex than welling blended whole life insurance and indexed universal life insurance. Mainly because term insurance is a very simple product to understand. You pay a reasonable premium to whatever company will give you the best price for the death benefit you’d like to have given your health profile.

This is not to say that it is easy, just less complexity in the product, its design, and ongoing maintenance that needs to be done after the sale. The big challenge with selling only term insurance is that for the majority of agents, there is no renewal commission. That means you will only be paid commission on the first year’s premium. After that, you will receive nothing in compensation.

That is not necessarily a bad thing, just the reality here with selling mostly term insurance. You will need to process a much higher volume of business each year and with much greater regularity. To break that down into its most vital activity—you’d better have a way to fresh leads in the door every day or at the very least a couple times each week.

We have colleagues that sell life insurance from home that earn barely enough to get by and we have some that make upwards of $1million each year. Your level of success will be determined largely by your commitment to whatever model you choose—the type of life insurance you focus on will dictate how you construct your business to be most effective and how much money you will make.

How much does a life insurance agent make per policy?

There is no set amount that a life insurance agent makes on each policy. Your first-year commission is typically a percentage of the annual premium for the policy. The percentages can vary from company to company and from agent to agent.

There is no set amount that a life insurance agent makes on each policy. Your first-year commission is typically a percentage of the annual premium for the policy. The percentages can vary from company to company and from agent to agent.

As a general rule, you will start off earning around 80% commission as a new agent. Someone is going to write to tell us how wrong this number is and that you can make much more or much less. Agreed, there is no real parity in the marketplace but the 80% number is generally true for most new agents.

That means if you sell a policy that has a $1,000 annual premium, you will be paid $800 in commission on the policy. If the client pays monthly, you will be paid your commission each month.

There is also something known as a commission advance that some companies will offer but I would caution against it if at all possible. You could easily end up in a situation where a client stops paying their premium in the first year and you (agent) owe the life insurance company for the money that was advanced to you.

How much can you make selling life insurance?

If you are working as an independent agent and being paid as a 1099 contractor, as most of us are, the sky is the limit. How much can you make depends on how much you can sell.

Are you able to develop a systematic way of getting new potential clients in the front door, assessing their needs, persuading them to move forward, and having back-end processes in place to process the application, underwriting, policy delivery, and getting your new client to make the first premium payment? Remember you will not be paid your commission until the client’s policy is approved and they have paid their first premium.

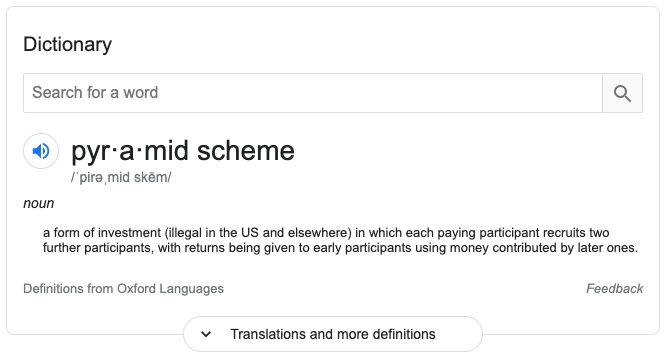

Is selling life insurance a pyramid scheme?

That is an interesting question for sure and one that may have a little nuance in providing the correct answer. Here’s what google tells us is the full definition of a pyramid scheme:

Based on the dictionary definition, no, selling life insurance is not a pyramid scheme. In fact, this definition is synonymous with a Ponzi scheme. And I can assure you that selling life insurance is neither if you are doing it legally and not acting fraudulently.

On the other hand, based on how we hear most people describe what they believe a pyramid scheme to be, life insurance selling could be recognized as such. That is, a business that is largely based on recruiting and the person who recruited you receiving a piece of commission for every policy you sell.

Most times, that slice is paid directly to your “upline” by the insurance company. That person has proven their competence and skill in the life insurance selling business, thus earning a higher commission than you.

Here’s an example to illustrate the point:

Tom has been in the life insurance business for 12 years. He’s really tired of running around at night and on the weekends meeting with people at their kitchen table. So, he talks to his buddy, Bob, and lets Bob know that he could do really well, selling life insurance. Bob hates his job and is looking to make a career change so he comes to work with Tom.

Tom helps Bob get contracted and appointed with a few life insurance companies. Bob now earns 80% commission on any policy he sells per his contract. What he may not know is that Tom earns 100% on every policy, so that means he’ll get 20% on anything that Bob sells. And you can be sure that whoever recruited Tom into the business makes something on everything Tom and Bob sell as well.

The life insurance business has always worked that way. Most people define that as a pyramid scheme but in reality it really isn’t. It’s actually how most every business works that have a product to sell and distribute. Just think about how many people get a piece of pretty much every product you buy before it reaches your hand. The life insurance business is no different. Every insurance company has a total amount of commission that will be paid on the first year premium—somewhere around 140-150% in aggregate.

Bottom Line About Life Insurance Selling from Home

Selling life insurance from home is a viable career path and one that is certain to grow in popularity in the coming years. More and more traditional life insurance sales and agencies will fall away, making room for those of us that choose to sell life insurance virtually from our home offices.

Just like any other work from home sort of job, it requires self-discipline, determination, and a healthy dose of grit.

Yes this isthe way it is. The real truth however does not disclose the 80 percent agent commission usually comes at the cost of buying leads which always lowers his net commission sometimes dramatically, explaining why his upline can’t retain agents.

I’d like info on selling life insurance from home.

Hi Michael, this blog post was created for informational purposes. We do not currently provide training or other information on selling life insurance from home.

I’m a Licensed Agent in New York. Doing This Business via Zoom is the waive of the Future,especially for Term Insurance. When you realize after you develop an organized system of time management you will double if not triple your sales volume. No more time consuming travel toappointments.

I’m a bit confused. Do you work hired with a company or independently when working from home?

Dani, you could be either working for a company or independent while working from home.