If you are searching for the right life insurance policy to generated cash value quickly or even immediately, you will have a couple of different options. But you should be aware that more important than the type of policy—whole life insurance or universal life insurance are going to be the two types—you need to know that policy design and funding will have the greatest impact.

You can purchase the right type of policy and not achieve the desired outcome of growing cash value immediately. The details very much matter when setting up your life insurance policy for the purpose of rapidly building cash value.

Working with s competent, reputable, and experienced life insurance broker (we fit this description by the way) ensures that you get are purchasing a policy that generates the cash value with the quickness you desire.

Which Types of Life Insurance Have Cash Value?

There are two broad categories of life insurance that have the ability to produce cash value. Those are whole life insurance and indexed universal life insurance.

There are two broad categories of life insurance that have the ability to produce cash value. Those are whole life insurance and indexed universal life insurance.

Of course, there are quite a few iterations of both types of life insurance but broadly speaking those are the two that we use most often for our clients. Particularly for those people looking to accumulate immediate cash value.

Without going too far down the rabbit hole of policy design (as we’ve covered that already here and here) you only need to understand one fundamental truth: to grow immediate cash value, your policy has to minimize the premium you pay toward the most expensive components.

For whole life insurance, the most expensive component is what most life insurance companies call the ‘base death benefit’ or ‘base policy premium’. That is the cost of the permanent death benefit that you are buying before you blend in term insurance and the premium going to the paid-up additions rider. Mind you, all components are important and you must use the term rider and paid-up additions rider to have any chance of accumulating immediate cash value in your whole life policy. Expense structure is what drives the bus here and why it is important to minimize the base policy costs as much as possible.

For indexed universal life insurance, finding the correct policy design is way easier. You can easily design your IUL policy in reverse. That is to decide how much premium you would like to pay and then minimize the death benefit to the lowest possible point without creating a modified endowment contract (MEC).

This technique for designing an index universal life policy is referred to as a ‘minimum non-MEC’ design. You are forcing the policy to accept as much premium as possible for a particular death benefit. Obviously, the insurance company doesn’t need all of that premium to insure the death benefit, so a sizable piece of the premium paid is credited to your cash value and earns index credits based on the underlying index you choose to follow in your policy. Most have several indices to choose from.

How Long Does It Take to Get Cash Value From Life Insurance?

That is a very good question and gets right the heart of the matter with any type of cash value life insurance. Most people want to know how long it’s going to take for them to have cash value available in their policy.

That is a very good question and gets right the heart of the matter with any type of cash value life insurance. Most people want to know how long it’s going to take for them to have cash value available in their policy.

Often that is because they are looking to borrow against the cash value in the form of a policy loan. But obviously, if there is little to no cash value, you are not able to borrow against it.

There is no way to give a definitive answer to the question of how long it takes to get cash value from your life insurance policy. However, the best answer is that it will depend on how much premium you are paying, how old you are, and what health rating class were you given when the policy was issued.

Think about this logically for a moment. If you wanted to have $100k available in cash value to get from your policy six years from now, you would need to pay more than $20k each year in premiums. Life insurance policies offer a nice, decent, stable return over time but it is not a miracle producer of huge returns in the short term. If you have a short time horizon, your policy design and premium funding amount are of the utmost importance.

Typically speaking, if you have a short term desire to get cash value from your life insurance policy, whole life insurance will work better. Now, that is not for any of the reasons that others might claim about it being a superior product to indexed universal life, no it’s just different.

And one of the major differences is that whole life does not have a surrender charge associated with it. That means that whatever cash value you have is immediately (or within a month of policy issue) available to be loaned to you as the policyholder.

Whereas most indexed universal life insurance policies have at least a 10-year surrender charge period. That means that you might have $100k of cash accumulation value in your policy but only have $50k in cash surrender value because you are in the fifth policy year.

If that is the case, your loan availability is limited to the $50k in cash surrender value. To be more precise, it’s typically about 90% of the cash surrender value that will available for policy loans—depending on if you are using a fixed loan or an indexed loan.

Why Limited Pay Whole Life Works to Create Quick Cash Value

Many times over the years, we have seen instances where a limited pay whole life insurance will work quite well at forcing more cash value growth earlier in the policy lifecycle. It’s not magic, just that you are paying much more in premium than required to fund the death benefit but you are doing so in a compacted time frame.

Also, keep in mind that something like a 10-pay whole life policy can also be blended with term insurance and loaded up with paid-up additions. Two things you should absolutely do if you want to use a limited pay whole life policy to grow your cash quickly.

What Is the Cash Value Of A $500,000 Life Insurance Policy?

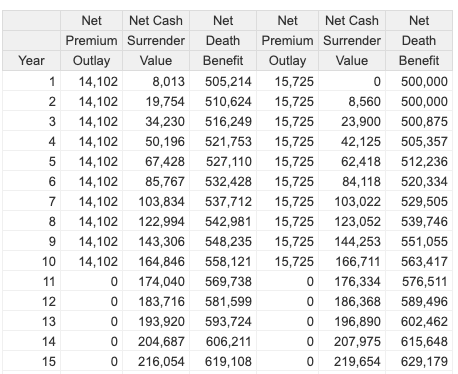

Take a look at this table illustrating a 10-pay whole life policy, the first has no paid-up additions rider and the second has a term rider with a paid-additions rider as well. Both for the same $500,000 death benefit, only a different policy design which demands slightly more premium in option 2:

Interestingly, this policy illustrates a concept that I had no plans of addressing here but the numbers are present so might as well. Notice that the cash value accumulates immediately in the first version (term blend with PUA rider). Whereas the same 10-pay policy with neither of those two features included accumulates cash value much more slowly but has more cash value at the tenth year and beyond. No great mystery, however, as the premium is nearly $1600 more each year for the same death benefit. More money in premium, more cash value created over the long term.

We’re pointing this out to illustrate the point that different designs produce different outcomes and neither is right or wrong. Just depends on what you are trying to accomplish with your policy. In this particular instance, I think most people would choose the option to have more cash value, earlier in the life of their policy but who knows, maybe you have more of a long-term focus and have no plans to access your cash value until much later (like more than 20 years).

Wrapping Up the Immediate Cash Value Discussion

Some may come along and point out that we failed to include a detailed description of indexed universal life insurance in talking about creating immediate cash value. That's a fair critique but using IUL to create cash quickly is tricky because of the surrender charge. Yes, you could add a ‘waiver of surrender charge', ‘liquidity', or ‘cash value surrender enhancement' rider to an index universal life policy but the expense of doing so is prohibitive in most cases. In fact, we've never seen anyone actually buy a policy in that manner. Those benefits were largely created to be used in corporate-owned life insurance and the motivations are different.

If you want to rapidly accumulate cash value that is accessible through a policy loan, a whole life insurance policy with the right design is your best bet. And if you are wondering who would help you get that policy, look no further, we are here and happy to help you get the policy you want, just get in contact with us here.

Would it not make the most sense to start with a max funded high early cash value whole policy and then year 2 or 3 perform a 1035 exchange into an IUL. This way you build cash value immediately and benefit from greater long-term growth without having to wait years for the IUL cash value to ramp up.

Hi Erik, the same mechanism that drags IUL performance for the first few years will still be at play. The 1035 doesn’t do much more than a minimum non-MEC increasing death benefit with a maximum MEC allowable premium would accomplish.