A partial surrender of a life insurance policy releases some of its cash value while keeping the policy in force. This means the policy owner can remove some of the cash value in his/her policy without having to cancel the entire policy. Life insurance policy owners most commonly make use of this feature either when they feel less concerned about their total amount of death benefit in force and wish to use the cash value the policy accumulated or when a serious situation arises that requires the policy owner to find money to cover an obligation no matter the consequences.

Partial Surrender versus Withdrawal of Cash Value

In the life insurance world, the terms partial surrender and withdrawal are effectively synonymous. Industry professionals often use the two terms interchangeably. You'll most likely hear and see the term withdrawal more often than surrender as most people feel that terminology has wider understanding/is less confusing to the general public.

What Types of Policies Allow Partial Surrenders

Universal life insurance policies and whole life insurance permit partial surrenders. However, the two policy types approach partial surrenders differently.

Universal life insurance pioneered the ease of surrendering a portion of your policy's cash value with little to no effect on the death benefit. Depending on the death benefit option used at the time of the withdrawal, the death benefit may not change on a universal life insurance policy when a partial surrender takes place.

Universal life insurance policy owners have the ability to withdraw any cash surrender value in their policies whenever they want to. How the cash value arrived in the policy makes has no effect on its eligibility for partial surrender.

Whole life insurance, on the other hand, has some very specific rules about partial surrenders. In general, whole life policy owners can only withdraw cash value created either through the elective paid-up additions rider or dividends used to purchase paid-up additions. Policy owners cannot withdraw cash value accumulated through the guaranteed accumulation of base whole life cash value. Please note, this does not include guaranteed cash value growth of cash value created by paid-up additions. This only applies to the guaranteed cash value attributed to the base whole life policy.

Whole life policy owners can, however, take a partial reduction of death benefit on their base whole life policies to achieve a partial surrender of base guaranteed cash value.

For example, assume you own a $500,000 whole life policy with $20,000 of base guaranteed cash value in it. You'd have the option to release $5,000 of this base guaranteed cash value from the policy if you were willing to accept a $125,000 reduction in base whole life death benefit from the policy. Accomplishing this task is a rather involved process that can have significant 7 Pay Test consequences on the policy, so it's not something to approach lightly.

When can you Withdraw Money from a Life Insurance Policy?

You have the option to make a partial surrender of a life insurance policy whenever you have cash surrender value in the policy. For some life insurance policy designs, this could mean as early as the first policy year.

Unlike policy loans, which can have a waiting period, partial surrenders normally have no waiting period. But, you should understand that universal life insurance policies may apply pro-rated surrender charges to partial surrenders if they are in access of 10% of the net cash value of the policy.

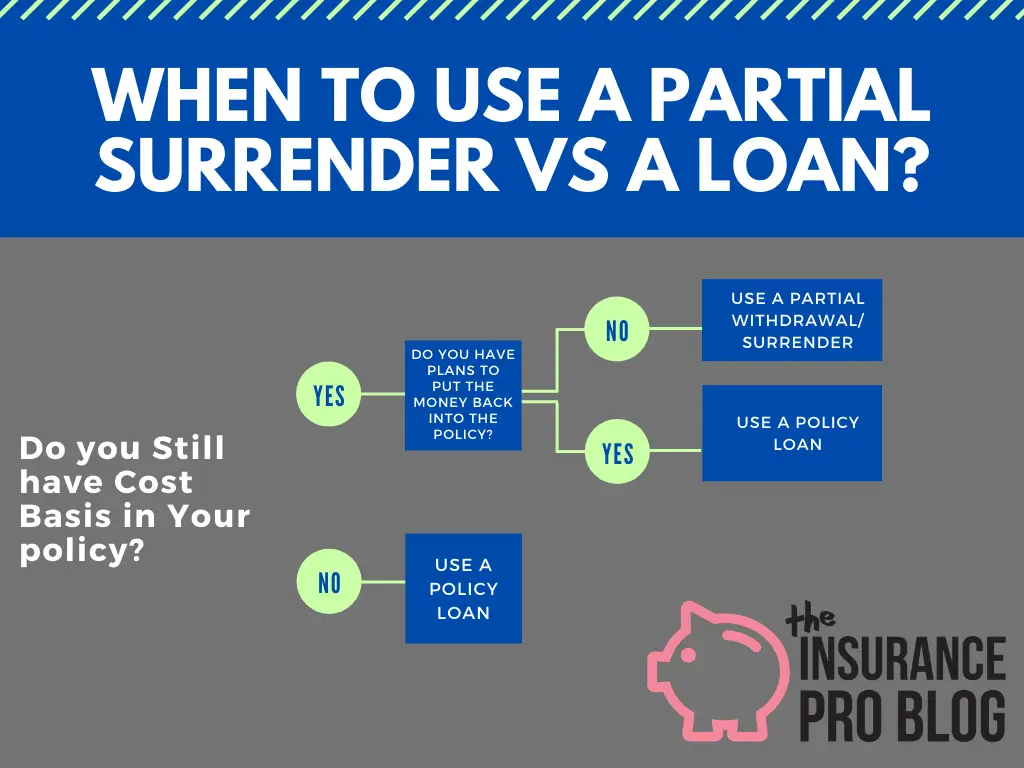

Difference Between a Partial Surrender and a Loan

Partial surrenders involve permanent removal of cash value from a life insurance policy. The policy owner generally does not have the option to put the money back into the policy in a future year (there are some circumstances were a non-over-funded policy may have the capacity to accept additional funds, but if the policy is max funded to the 7702/TAMRA limits, the policy owner cannot put the withdrawn money back into the policy).

Life insurance policy loans, on the other hand, provide the opportunity to effectively put the money back into the policy. Because policy loans simply encumber portions of cash value as collateral for the loan amount, the policy owner has the option to payoff the loan and return the cash value to unencumbered status.

Given their differences, the general rule-of-thumb to follow is:

If the need to take money from the policy is permanent with no plans of ever putting it back into the policy, a withdrawal makes sense.

But if the need for money is temporary or there is a plan to put the money back into the policy, then a loan is the preferred mechanism to access the cash value.

Tax Consequences

Partial surrenders release the cost basis first. This is one of the many tax benefits of life insurance. So long as the partial surrender amount released from the policy does not exceed the sum of premiums paid by the policy owner, there is no tax liability on the distribution of monies from the policy.

But once the policy owner recovers all of his/her cost basis in the policy (i.e. the sum of premiums paid into the policy), any future partial surrender will have a tax consequence to it. At this time, the policy owner must recognize any future distributions as ordinary income and will owe ordinary income taxes on the distributions.

There is a way around tax consequences for distributions once the policy owner removes his/her cost basis in the policy. Using policy loans instead of partial surrenders will prevent any tax liability because policy loans do not have count as taxable distributions from the policy. So the policy owner can use partial surrenders up to the amount of premiums he/she paid into the policy and then take money from the policy thereafter by using policy loans.

Do you have an expert I could contact regarding a partial withdrawal from my insurance? They are saying I cannot (BNZ). I have appox $58k & need to withdraw $10k – $18k urgently. Would appreciate a direction to whom I can talk to.

Thank you,

Margaret Jones

Hi Maraget,

We, unfortunately, cannot get involved in matters like this. The answer could be that you have a plain whole life product and the $58k is guaranteed cash value. You cannot withdraw guaranteed cash value from one of these whole life products, you must take a loan against it. The other possible scenario is that you own a Universal Life Insurance product that is still within the surrender period. so you may not have enough net cash value to make such a withdrawal.