Whole life insurance dividend options are one of the ways a whole life policy provides the policyholder robust versatility. Understanding these different options is crucial for the proper use of a dividend-paying whole life policy.

The evolution of dividend options brought about by insurance company creativity creates even more flexibility and versatility of whole life insurance. Today I'll detail the four options found with just about every dividend-paying whole life policy available. I'll also spend some time detailing some more unique dividend options available at just a few insurers.

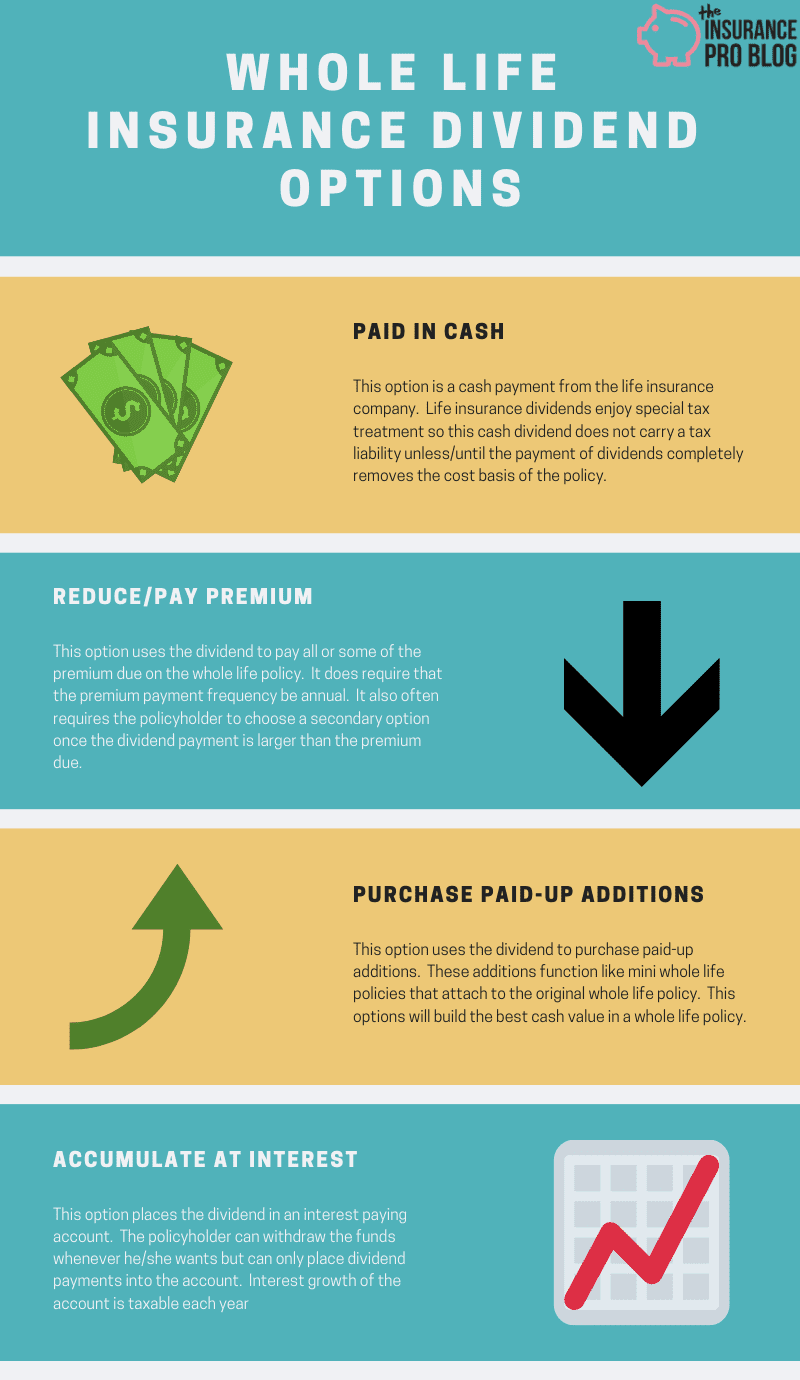

The Four Original Whole Life Insurance Dividend Options

The original four options policyholders have for a whole life dividend are:

These four whole life insurance dividend options did not originate at the exact same time, but their existence as options spans an extremely long time. Practically ever life insurer issuing dividend-paying whole life insurance today includes these four options.

Dividend Option: Paid in Cash

The option to receive the dividend in cash is pretty self-explanatory. Each year the life insurer pays the policyholder the dividend in the form of a check. The payment comes directly to the policyholder who can then use the cash for whatever purpose he or she sees fit.

U.S. Tax Code classifies the dividend payment on participating life insurance policies as a refund of premiums paid, so taking the dividend in cash does not usually cause an immediate taxable consequence to the policyholder. This is the case because the dividend paid in cash is simply reducing the tax basis established by the policyholder's payment of premiums.

Eventually, however, opting for dividends paid as cash could remove the cost basis of the whole life policy. If this takes place, all dividends paid moving forward will carry income tax consequences to the policyholder.

An example will help clarify this concept.

Sarah owns a 10 Pay whole life policy with a cost basis of $50,000 after 10 years. She opted for the paid in cash whole life insurance dividend option. Once the insurer pays Sarah an aggregate $50,000 in dividends, Sarah will need to report all future dividends as taxable income.

Also, note that if dividend payments do remove the cost basis any withdrawals from the policy will cause a tax liability as well. Policy loans continue to enjoy tax-free status so long as the policy does not violate the Modified Endowment Contract rules.

Dividend Option: Reduce/Pay Premium

Choosing to reduce or pay the premium with the dividend means the policyholder chooses to pay a part or all of the premium due with the dividend. If the dividend payment is less than the total premium due, the policyholder will need to pay the rest of the premium either with money out of pocket or with cash values from the whole life policy. It's much more common for the policyholder to pay with out-of-pocket money.

Once the dividend payment equals or exceeds the premium due amount, the dividend can pay the entire premium due and the policyholder does not need to make any payment to the policy with any out-of-pocket money. It's fairly common to see older whole life policies using this option as the policyholder can keep his/her death benefit in force without having to pay the premium on the life insurance policy.

Choosing this option does come with some consequences all policyholders should understand.

First, the insurance company will require the policyholder to change the payment frequency to annual if it's not paid annually already. This is important for policyholders who pay premiums under some other frequency as it could cause a cash flow problem. An example will help highlight this point.

Imagine that Claire owns a whole life policy with a $1,000 per month premium she pays. She decides that she wants to use the dividend option to reduce premium. In the year she makes this decision the annual dividend on her whole life policy is $3,000. The annual premium for her policy is $11,765. Choosing the reduce premium option means Claire must change her payment frequency to annual. Her dividend will reduce the premium due to $8,765, which is due in one lump sum. If Claire does not have the $8,765 to pay the premium all at once, the reduce premium dividend option is not a good idea for her.

Though the dividend payment is a refund of premium, using the dividend to pay ongoing premiums due creates an offset that leaves the tax basis static in all years a policyholder uses this option. This means the cost basis will neither go up nor go down while using the dividend option to pay premiums.

If the dividend is smaller than the annual premium, any payment made with out-of-pocket money will increase the cost basis of the policy.

It's also worth noting that dividend payments can and do fluctuate. So if the dividend payment covers your entire premium this year, it might not next year. I bring this up because life insurance ledgers assume a constantly increasing dividend due to the assumption that the dividend scale remains static. This is not how most whole life policies work in real life. Dividends do tend to grow substantially over time, but that growth is not always absolutely linear.

Lastly, know that this dividend option is somewhat unique given that there is a limit to the amount of dividend applied to this option. Once the dividend is larger than the premium due on the policy, the excess amount must go somewhere. For example, if you have a $10,000 annual premium and the dividend for the year is $12,000, you have a remaining $2,000 that cannot go towards paying the premium. In this case, the policyholder must choose a secondary dividend option. Simply, he or she will choose one of the other remaining dividend options and the $2,000 will go towards that option.

Dividend Option: Purchase Paid-up Additions

The dividend option to purchase paid-up additions instructs the insurance company to take the annual dividend and purchase paid-up additions with it. Paid-up additions are mini whole life insurance policies that attach to a main whole life policy. They earn dividends themselves and have immediate cash value.

This dividend option will ensure the most bang for the buck in terms of premiums generating cash surrender value. Put another way, if you seek to maximize return on premiums (i.e. the internal rate of return of a whole life policy) then the option to purchase paid-up additions is the dividend option you seek.

This dividend option is also how whole life policies accumulate non-guaranteed cash value. The non-guaranteed cash value of a whole life policy is simply the cash value created through paid-up additions.

Some life insurers refer to this as building “dividend additions” and will even make reference to surrendering dividend additions if the policyholder chooses to withdraw money from the policy at some point. If this is the case, understand that the terminology means the same thing.

Dividend Option: Accumulate at Interest

The dividend option to accumulate at interest means the insurance company places the dividend payment in an interesting bearing account and adds interest to the account each year. The insurer sets the interest rate on these accounts annually and usually, announces it with other information regarding interest rates such as loan rates, universal life interest rates, and annuity rates. If you have trouble locating these announcements, a quick call to the insurance company can answer what the current rate is.

The rate can change annually, but most insurers establish a minimum guaranteed rate on these accounts.

The policyholder cannot choose to place additional funds into the interest account. So for example, if a policyholder noticed that the interest rate paid on the account for the accumulate at interest option was far higher than his/her savings account, he/she would not have the option to move money from the savings account to the interest account at the insurance company. Only dividend payments can go to the account.

The policyholder is free to withdraw funds from the interest account whenever he/she sees fit. But will not have the option to put the money back into the account at a later date. Once removed, the only way to build the account back up is through future dividend payments on the whole life policy.

You should understand that the interest account is not part of the life insurance policy and does not benefit from the tax-friendly treatment associated with cash value life insurance.

Interest earned under this dividend option incurs an income tax liability just like interest earned on any other cash equivalent account held at a bank or thrift institution. The policyholder will receive a 1099-INT at the end of the year reporting all interest paid and must file this with his/her taxes.

The life insurer will not issue a policy loan against the interest account. The values accumulated can only be withdrawn.

At one point in the 1980's the interest rate on these accounts grew faster than dividend interest rates and some people began using this option more to maximize interest earnings in specific years. While it's always possible we could return to a similar situation, this option usually lags the option to purchase paid-up additions in terms of overall return on premiums paid to a whole life policy.

The Fifth Dividend Option

As insurers evolve and become more creative with product design a “fifth” dividend option appeared that is quite common–though not as universal as the four options mentioned above.

This life insurance dividend option allows the policyholder to use the dividend to purchase term insurance. This can produce the most efficient way to acquire death benefit relative to the premium paid for whole life insurance (i.e. buying regular term insurance will still be the most efficient use of premium dollars to maximize death benefit).

The significance of this option can be substantial when it comes to manipulating whole life policies with a goal to optimize cash value. In some cases, this dividend option is the mechanism for blending–but this is not always the case.

This option can also come in different forms regarding the type of term insurance purchased or the way the term insurance works.

In most cases, the term insurance is either One-Year Term insurance or Annually Renewable Term Insurance–not the same thing, though they might appear quite similar. For some insurers, the term insurance death benefit could be flat, reducing, or increasing.

Also unique to this option, much like the option to pay whole life premiums, there's usually a limit to the amount of the dividend this option will use. Once the dividend purchases the term insurance, there could be left over dividend that must go to a different dividend option. Similar to the pay premium situation, the policyholder must choose a secondary dividend option to direct the remaining dividend.

Less Common Life Insurance Dividend Options: The New Frontier

Though the life insurance industry has a reputation for being stodgy and slow to evolve, it does work quite tirelessly to innovate and bring new features and benefits to policyholders. In recent years, life insurers developed additional features for whole life dividends in an attempt to enhance policyholder value. These options are by no means universal and often exclusive or unique to just one or a few life insurers.

Long Term Care Benefits

Perhaps one of the most needed benefit option, dividend options to pay for a long term care insurance benefit attached to a whole life insurance policy greatly enhance life insurers' earlier attempt to solve this problem through accelerated death benefit options.

Essentially, this option uses all or a portion of the dividend to pay for a long term care insurance policy that is attached to the whole life insurance policy. This reduces some of the high cost of long term care insurance premiums found on standard stand-alone policies but does usually sacrifice some of the benefit richness found on more traditional long term care insurance products.

Index Credit Option

This option works somewhat like the option to accumulate at interest with a new twist. The dividend payment goes into an index account that earns interest tied to a stock index in much the same way indexed annuities or indexed universal life insurance earns interest.

The policyholder cannot add additional funds to the indexed account but can direct all of his/her dividends to the account. The policyholder is free to withdraw money from this account at any time.

GREAT ARTICLES PLEASE KEEP UP THE GOOD WORK !

Can you please confirm that my whole life insurance policy that was issued in 1990 with a guaranteed interest rate of 5% (paid annually) has qualified now to suspend annual premium payments? The accumulation account is now at $148,732.58 which will produce interest this year of $7, 436.63. My annual premium is and has been $3226. The COI is at $4,026.87 now. There is a statement on the Policy Data Page stating that the Maximum Premium excluding Special Class Premium (which is $934 of the $3226) so that would be the Maximum of $5,847.19 + $934 equalling $6,801.19. The interest earned currently covers this Maximum – which the premium cost is far from reaching that point. I have been told that year 34 (2024) is the point where I can suspend premium payments…………..last letter said (never mentioned in previous responses) that this will “Allow the cash value to continue to sustain the death benefit ($300,000) to the insured’s age of 100! I am now 74 and doubt that I will live to even close to 100! Oh, I continue to be offered a reduced Death Benefit if I stop premium payments – currently a little over $250,000. No – I have paid too long to settle for that. Please advise. Do I need an attorney? Lincoln National Life Insurance is my company – my policy was written by Sovereign in 1990, then acquired by Jefferson Pilot, then acquired by Lincoln in 2006 through a merger – bet they hated being handed a Guaranteed 5% Interest Policy!

Hi Randy,

I can’t tell you if you can stop paying premiums, but Lincoln can provide you with an in force ledger that can tell you what the policy is likely to do if you stop paying premiums at any point (e.g. now, at 2024, or any other point). This ledger should be able to provide a detailed look at how policy values unfold using both the current expenses as well as the guaranteed expenses of the contract.

What I can say is this. Given the premium and the death benefit you mentioned, you’ve managed to buy $300,000 of life insurance for 40% less than it would have cost you in annual premiums for a comparable whole life policy. You’ve saved quite a bit of money over the past 30 years in terms of life insurance premiums and the policy appears in pretty good shape given the cash accumulation and the interest earnings each year relative to insurance expenses.

Thanks, Brandon, for your reply. I have received “illustrations” over the past years which I am guessing is the in force ledger that you referred to. A recent source of frustration related to my request to Lincoln when I asked for this projection showing the numbers if I were to stop paying annual premiums. The reply was “If the premium payments are discontinued the policy will lapse without value.” Obviously, the legal advisor with whom I (and my wife) have been communicating knows that my reference to stopping premium payments would be accompanied by the proper form indicating an initiation of their offer to stop payments with a reduced death benefit, which I would obviously have followed through on! So, the communication stream with Lincoln is quite frustrating and, I might add, insulting. Wonder why they just wouldn’t run a numbers sheet, starting currently, showing how long my policy would stay in force if the 5% interest earned annually was, simply, applied to the COI each year? This policy was originally written by a very skilled and experienced insurance agent (he passed away in 1992) as a “vanishing” premium policy, Of course, the interest at time of issue (1990) was 8.25% – but, the 5% Guaranteed Rate is what has made this policy carry on with such a strong Cash Accumulation characteristic over the years as the federal interest rate dropped………well below 5%!

Is there a possibility that Lincoln may be adding extra years of premium payments to lessen their loss of paying the Guaranteed 5% rate? I was informed by an agent at Jefferson Pilot in 2006, that this policy would qualify for a suspended premium status in 2010. In late 2006 Lincoln acquired Jefferson Pilot. I was told in 2010, by Lincoln, that this policy would be able to suspend premiums in year 28 (2018) – then, when I spoke to Lincoln in September of 2018 to validate reaching this point, the reply was this policy would be able to suspend premium payments in year 34, adding another 7 years to premium payments! Is it reasonable to think that Lincoln may “move the end point” again, in year 34? Very troubling!

Hi Randy,

I suspect a lot of communication from Lincoln is hedged because the legal department controls what specifically they can and cannot say. Life insurance companies rarely offer guidance on policies as they feel that is up to insurance agents who take on the responsibility of advising their clients on life insurance policies. Life insurers do not want, nor are they honestly set up to take on, the responsibility of advising you.

Lincoln is most likely hedging their statements because the costs of insurance on the policy could increase. This doesn’t mean they will, but they could beyond the current amount (to the guaranteed maximum that I believe you referenced in your last message).

So to be clear, Lincoln is going to ensure that every communication cannot later be construed to mean something they didn’t intend, and their way of accomplishing this is to be vague and to disclosure every possibility no matter how remote.

Brandon,

Thanks for this reply. It may be time to acquire a legal source to communicate with Lincoln. If, as you suggested, the company is continuing a vague posture, simply to avoid recognizing the limits (specifically, the Maximum Premium amount of $6801.19) then, as a policy holder, I am, in my opinion, being yanked around! I appreciate your responses – will have to decide if another 5 years of premium payments will be cheaper than the fees I will need to pay an attorney to help argue my point!

Hi Randy,

I’m going to chime in here for a second with a few additional thoughts. If you have a Universal Life policy with Lincoln, there’s really no way for them to tell you how much more premium will be required to have your policy “paid up”. Unlike whole life insurance, there is no such thing as a “paid up” universal life insurance policy. Even with Lincoln honoring a 5% guarantee on your policy, they can raise the cost of insurance. Not saying they will do that but they can and a handful of universal life policies have done so in the last few years. Either way, Lincoln is not likely to ever issue a statement to you that guarantees anything if you discontinue premium payments.

That doesn’t mean that the contract will fall apart if you stop paying the premium but just that they won’t/can’t guarantee that. It’s just not how these policies were constructed from the beginning. Now, the policy may be able to sustain itself if you stop paying the premium, impossible to know with 100% certainty. Keep in mind, if you stop paying the premium, the policy will remain in force until all the cash value has been consumed by the cost of insurance. You should ask them for an in-force illustration assuming that you pay what you’ve been paying for the next five years (if that’s what you’d like to see) and see how that works. You can ask for as many of those type of scenarios as you desire, however, I would highly doubt that you’ll ever get Lincoln to guarantee anything to you in writing other than what was stated in your original policy.

If you need to have an absolutely 100% guaranteed death benefit, you might consider using the cash from this policy via a 1035 exchange to a new policy with another company. Not saying you should do that, just that you might consider all of your options.

Hey Brandon,

Thanks for your article it was helpful in understanding whole life policies like I have.

Question: I have been using my dividend to purchase paid up additions for the past twenty years and was thinking of surrendering the dividend cash value to help with down payment on a home. I would use dividends moving forward to purchase paid up insurance. Would this be a good move?

Hi Michael,

This is certainly an option that you could use for the downpayment. Alternatively you could take the money from the policy as a loan. Here’s a brief look at why you might choose one option over the other:

If you surrender the PUA cash value from dividends you’ll remove the cash from the policy and have no worry about putting the money back in there. You also won’t have the ability to electively put the money back in there, which may or may not be a major concern. With the cash, you can obviously make the downpayment and then being servicing the mortgage with whatever source of income you have. You will forfeit earnings (guaranteed interest and dividends) on the cash value that you surrendered and you will also forfeit the death benefit created by those PUA’s that are being cashed out.

If you use a loan you may or may not want/need to make repayments towards the loan. This depends on the size of the loan relative to the total outstanding cash value in the policy. In either event, you’ll be free to make repayments (if you choose to make them) to the loan at your discretion as there is no fixed repayment schedule on a life insurance policy loan. You will not forfeit earnings on the cash value that acts as collateral for the loan. So whatever the planned downpayment amount is that you would have surrendered will instead remain in the policy and continue to accumulate guaranteed interest and earn dividends (whether the dividend is the normal dividend or an adjusted dividend depends on the dividend recognition policy of your life insurance contract). You will have an adjustment in net payable death benefit by the sum of the loan; this will most likely be a value less than the death benefit lost if you surrender paid-up additions since PUA death benefit is normally a multiple of PUA value. The net result to the death benefit may be rather close in either scenario.

The right decision comes down to your comfort level between the two options. If loan has the ability to net you more overall wealth building through continual cash value compounding, but this most likely only materializes if you repay the loan. If you’d rather not commit additional resources to repaying the loan, you’re likely better off just taking the money out for the downpayment. But do pay attention to the death benefit lost in either case and make sure that you don’t need the death benefit coverage that such a reduction will create. The life insurer will warn you about the death benefit reduction as well, just to make sure you understand that the reduction will take place.

I am trying to understand a Dividend statement from John Hancock that I found in my dad’s files. he bought a $2500 in the 50s. Yes, 70 years ago. 🙂 The original policy was valued at $2500. 🙂 The statement has a line “Total Paid up Insurance – which is about $4K)” Is this the value?

Hi Laura,

Traditionally, paid-up insurance reported on a life insurance policy refers to paid-up additions. These exist most likely because John Hancock paid a dividend on this policy and your father used the dividend to purchase paid-up additions. This results in both a higher than original death benefit as well as higher than guaranteed cash value accumulation in the policy.