The paid up additions feature of a whole life insurance policy is one of the most powerful components with respect to cash value accumulation. Most whole life products have a paid up additions (PUA) feature, but they can all work a little differently so it's important to note that one company's approach could vary substantially from others.

But before we explain how they work…

What Are Paid Up Additions?

Paid up additions are available through a rider that is added to a whole life insurance policy. The PUA rider allows the policy owner to purchase additional paid-up insurance on their policy. That all sounds very technical, so let's explore what that actually means for you if you're looking at cash value life insurance (whole life in particular) and trying to decide if it's the right fit.

The PUA rider is the mechanism used to place additional money into a participating whole life insurance policy to increase policy cash value performance. Every dollar of premium that is allocated to the paid up additions rider creates a small paid up insurance policy that has its very own cash value that is created immediately. In general, whole life insurance policies that have a substantial portion of the total premium allocated to paid up additions will outperform those that do not take advantage of PUAs.

There are also various paid-up additions options available from each insurance company. It may all seem complicated but hang in there, we're gonna explain it in multiple ways and provide examples to illustrate how it works. We want to help everyone understand paid-up additions and their application to life insurance policies.

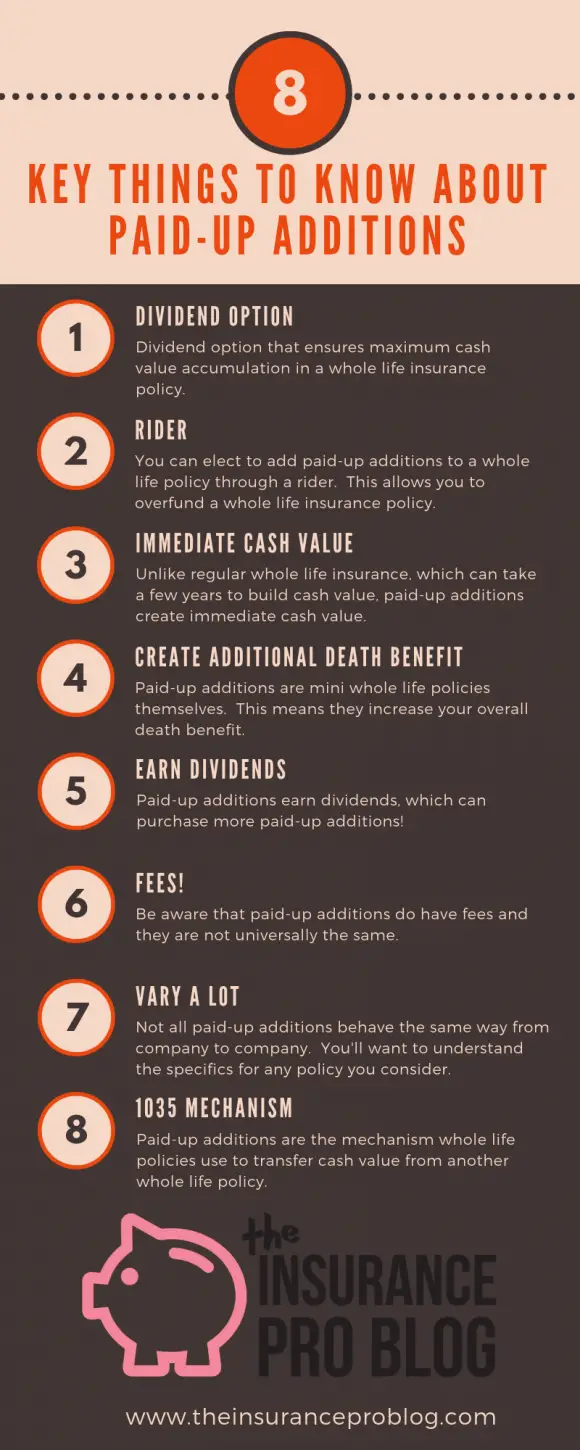

8 Things to Understand About Paid Up Additions

It makes perfect sense to dedicate some time to the discussion of paid-up additions and their role in cash value life insurance. You’ll find them under a few different names (additional insurance rider, enricher rider, enhanced paid-up additions, etc.), but it all means the same thing.

The important thing to understand is PUAs and the PUA rider are critical for creating a cash-rich policy. Today we'll help you understand how they function inside a well-designed policy that helps you achieve your goal of focusing on maximum cash value build-up.

With nearly two decades of working in the life insurance industry and having sold hundreds of whole life insurance policies over the time frame, we have actual, real-world experience with all of this. In fact, the Insurance Pro Blog itself is the longest continuously running financial blog committed to information on life insurance.

So when we sat down to figure out how best to explain PUAs, we came up with 8 key aspects you must understand to squeeze the most value from them

The 8 key things are:

- It's a Dividend Option

- It's also a Rider

- PUAs have Immediate Cash Value

- They have their own Death Benefit

- They Earn Dividends

- Have their own Load Fees

- Can Vary a lot from Company to Company

- PUAs are the Mechanism used for 1035 Exchanges for Whole Life Insurance

Using the Dividend Option to Purchase PUAs

A lot of whole life insurance policyholders have experience with paid-up additions but most may not realize this. One of the most common dividend options used for whole life policies is the option to purchase paid-up additions. This means the insurance company takes the dividend earned on a whole life policy and uses these funds to purchase the additions for the policyholders.

For those seeking the fastest accumulation of whole life insurance cash values, there is no better option than purchasing paid up additions. I'll explain later in this blog post why that is.

For most insurers, the dividend option to purchase paid up additions is the default option. So if the policyholder or agent do not elect a different option, the life insurer will automatically assume this option

The PUA Rider

In addition to being a dividend option, paid up additions can also be a rider. This means the policyholder can choose to add the PUA feature to his/her policy and elect to make a payment to the policy solely for the purpose of buying PUAs.

This differs from the dividend option to purchase PUA's because now the policyholder is choosing to take external funds and use them t0 purchase the additions. This money does not represent a dividend earned on the whole life policy.

To be clear, many whole life insurance policies afford the ability to both use the PUA dividend option and elect the rider thus allowing the policyholder to both purchase PUAs with their dividends and buy paid up additions directly with additional funds they decide to contribute to the policy.

Have Immediate Cash Value

When someone who owns whole life insurance chooses to buy paid up additions in addition to paying their base whole life insurance premium, they gain an immediate advantage–the paid up additions produce immediate cash value. This cash value functions similarly to the rest of the cash value in the policy. The policyholder can pledge this cash value for a policy loan. Additionally, the policyholder can surrender the paid-up addition and receive its cash value–we sometimes refer to this is “withdrawing” money from a whole life policy.

A dollar used to purchase a paid-up addition, creates a dollar of cash value (minus any fees associated with the paid-up additions, see the fees section below). This creates much faster cash value in the whole life policy versus standard base whole life insurance premium, which can take years to create cash value for the policyholder.

Creates Immediate Death Benefit

Paid-up additions also create an immediate death benefit, and this death benefit is a multiple of the dollars used to purchase the paid-up addition. For example, a dollar used to purchase a paid-up addition might create five dollars in death benefit.

This death benefit is immediately “paid up” (hence the name) and requires no further payments to remain in force. Paid up additions can be thought of as miniature paid-up whole life policies attached to a larger whole life insurance policy. This means the PUA feature (whether it be through the dividend option or an elective rider) augments the total overall death benefit of a whole life insurance policy. Over several years, the PUA feature could create a larger death benefit than originally purchased on the whole life policy.

The amount of death benefit acquired through each paid-up additions purchase depends on the age of the insured. As the insured under the policy ages, the multiple of death benefit created per dollar used to purchase the PUAs declines.

For example, a 30-year-old might receive $8 in death benefit for every $1 used to purchase a paid-up addition whereas a 50-year-old might receive $3 in death benefit for every $1 used to purchase a paid-up addition.

Earns Dividends

I mentioned earlier that paid up additions can be thought of as miniature paid-up whole life policies. These miniature policies are participating policies, which simply means that they too earn dividends.

The significance of this fact is subtle but substantial. Because PUAs earn dividends, there is a compounding effect that's created by the continual purchase of PUAs. More purchased, means more dividends earned. When dividends themselves go towards the purchase of more PUAs, this creates more PUAs which in turn purchase more paid-up additions, which earn more dividends, which purchase more paid-up additions, and etc.

There really is no better way to grow cash value quickly in with a whole life insurance policy than through the use of paid up additions. It almost seems like magic.

Load Fees

PUAs usually have a one time fee assessed at purchase. Insurance companies express these fees as a percentage of the purchase amount just like a load fee assessed against a mutual fund.

For example, if the paid-up additions load fee is 10% and a policyholder uses $1,000 to purchase paid-up additions, then the fee is $100. The $100 goes to the insurance company and the policyholder has $900 in immediate cash value created by the paid-up additions. There are no additional ongoing fees for paid-up additions.

Fees can (and usually do) differ depending on the way policyholders purchase paid-up additions. The example above most closely depicts how fees work for paid-up additions purchased through a rider.

The fee charged by insurance companies varies a lot among insurers. It's tempting to compare paid-up additions by load fees and suggest that lower is better. However because most whole life products are issued by insurers with a direct interest in returning profits to policyholders, a higher paid-up additions fee doesn't always mean a lower-performing policy.

Variation Across Insurers is almost Limitless

The exact functionality of the paid-up additions rider varies considerably from one insurer to the next. While most behave pretty straightforwardly concerning the dividend option to purchase paid-up additions, the paid-up additions rider differs greatly among life insurance companies.

Insurers also have a practice of calling the paid-up additions rider different things. Some common names are: additional premium rider, additional paid-up insurance rider, optional permanent protection, enricher rider, and supplemental insurance rider. They all mean and, for the most part, do the same thing.

Some insurers differentiate between a lump sum and scheduled paid-up additions rider. The difference being the former allows a single payment around the outset of the policy while the latter permits ongoing payments several years into the future.

Certain insurers permit a large degree of flexibility in the exact payment of the paid-up additions rider while others require a specific amount be paid each year.

Most insurers impose yearly and/or lifetime limits on the amount of money a policyholder can place into the paid-up additions rider. This limit might be a fixed amount or a multiple of some basis such as the amount of base whole life premium on the policy. Insurers place these limits because they worry about the liability created by the ever-increasing death benefit brought about by paid-up additions.

The Mechanism for a 1035 Exchange

For those seeking to make use of the tax-free 1035 transfer of cash values from one life insurance to a whole life insurance policy, paid-up additions are a required feature of the new whole life product. The paid-up additions rider is the mechanism through which the cash transfer can flow into the new whole life policy. Without a paid-up additions rider, the new whole life policy cannot accept the funds.

The good news is, almost all whole life policies issued in the United States have at least a paid-up additions feature in place to accept 1035 exchange money.

The “Supercharger” Rider

There have been books written about whole life insurance and using your whole life policy as a personal banking system. Those books often make reference to a rider that supercharges the accumulation of cash values in a whole life insurance policy. All of those references are referring to the paid-up additions rider.

The paid-up additions rider is most often used purely as a strategic way to increase the cash value of a whole life insurance policy. While paid-up additions do create additional death benefit, it's rare to come across a circumstance where one uses them purely to increase the death benefit.

Whether a life insurance policy design simply adds a PUA rider on top of a whole life premium or uses term life blending to open up additional funding capacity, the paid-up additions rider is a must for those seeking cash-rich whole life policies.

This has to be one of the best life insurance blogs I have read.

The style is extremely readable and understandable.

Each blog post gives just enough to understand one of many cogs of life insurance.

I look forward to reading the rest of the posts!

(non-affiliated)

Hey thanks!

Hi Brandon, I have a Whole Life policy, that I have a loan against, which has doubled. I am so lost, and need direction. Can you please assist? The agent that I had when I took out this policy has past away. The agent that has taken over the agency I am not comfortable with. He never returns my calls or takes a very long time to get back to me. I have a sinking feeling. Thank you for your help. Jean

Hi J,

Why not call the insurance company? They all have customer service departments that can assist with questions about policy functionality and they are staffed with regular hours to assist during the day.

You can contact us through this link. Please be as detailed as possible in terms of the information that you send us so we can see what sort of help we can offer up.

Thank you very much for this information! I have spoken with various life insurance agents about this PUA as a vehicle for increased cash value, and most look at me like I don’t know what I’m talking about…and granted, for the most part, I agree with them. However, I look to them for the knowledge, but I just haven’t been that lucky I guess.

You’re welcome Ruben. If you think we can be of any further assistance to you, feel free to contact us directly through the contact page.

Which whole life companies are best for PUA policies?

Traditionally, you’ll find the best value from companies like Penn Mutual, MassMutual, Guardian, and American United Life.

Or maybe Northwestern Mutual!?

So I’ve read many, many different articles on PUA and they all say the same thing in terms of the death benefit–it should increase. So on a participating whole life policy with a supplemental life rider that has its own premium, and a base benefit with its on premium, why are the PUAs that have accumulated for 2 decades now not increased the death benefit? There is a loan on the policy for the premiums, but when you add the numbers up–premium, loan, and dividends purchasing PUAs, the value of the supplemental life rider is just being reduced by the amount of PUAs and the overall policy value isn’t increasing like it should with all these little paid up policies. What gives? I’d love to hear your thoughts.

Hi Samir, the supplemental life rider (term “blend” rider) is your answer. The company most likely reduces the supplemental life rider amount by outstanding PUA death benefit. As soon as the outstanding PUA’s bring the supplemental life rider amount to zero, then you’ll see an increase in total outstanding death benefit. Until then, the PUA’s are reducing the supplemental term.

Thank you for the quick reply! I just got off the phone with the insurance company and while the rider is purchasing its own term insurance and PUAs for its value and death benefit, the cash dividends from the overall policy also are purchasing their own PUAs, and these PUAs aren’t showing up anywhere–that’s what’s puzzling. Because if we would have elected to have these dividends as cash, then the rider death benefit would still be the same, except we would have had a bunch of cash too. What’s your thoughts on this?

Was the insurance company not able to answer this question? It seems odd that they wouldn’t have been able to explain what is going on if you just spoke with them. Without seeing the actual policy, there’s not much else I can offer in terms of places to look. There may be a problem, but the insurance company should be more than capable of fixing it. Or, there could be a misunderstanding of how things are working. If that’s the case, the insurance company should be capable of clarifying it.

Well, they never got back to me. At this point I’m wondering what type of attorneys work on cases like this. It almost looks that this major insurance company just doesn’t want to acknowledge the issue since they would be facing a much large payout for the death benefit. How would you handle this situation if one of your clients was facing it?

I’d send a letter certified mail to the CEO’s office detailing the situation. Have done it before. Generally gets results.

Thank you for all the help and suggestions. After getting the detailed illustration, it does explain how the rider is a blend rider as you mentioned, and it is crystal clear now. 🙂 Thank you for the guidance and the fantastic site with lots of great reading! I’ve learned more about insurance policies here than anywhere else on the web. 🙂

They haven’t, and that’s odd to me as well. I’ve been trying to figure this out for over a month now. I’m supposed to be hearing back from them today.

I concur with the previous comment – great blog with a clear, concise writing style.

Question: My wife and I have had policies since 1987 with PUA riders. You’d think we would have a large amount of available cash value, but we borrowed against them when we were younger and didn’t start paying against those loans until relatively recently (last 7-8 years), so not that much.

1. Is the paid-up insurance cash value typically lumped together with the policy cash value? For example, where it says I could borrow $x, does that include the PUA cash?

2. Do you recommend prioritizing paying back the loans? I know the CV disappears if the death benefit is paid, but the death benefit increases as the loan balances reduce.

3. Just to reiterate: if the policies are surrendered, the paid-up insurance death benefit remains, correct?

Thank you.

Hi Walter,

1. Yes PUA cash value would normally be included guaranteed base cash value so maximum loan value is inclusive of PUA cash value.

2. This very much depends on what you are seeking to accomplish big picture.

3. No if you surrender the entire policy you’ll also surrender the PUA’s. You can stop premium requirements on the base policy and keep its current paid-up death benefit as well as your PUA death benefit by triggering the Reduce Paid-up feature. But be aware that the insurance company will most likely force you to repay the outstanding loan with a cash value surrender from the policy. This may or may not create a taxable event.

I hope you can help me out.

I have New York Life Insurance whole life insurance since 2010. I paid all my premium $3200 fo seven years. Death pay out is 200,000. I got a letter offering “the conversion provision on the term rider. This important provision allows you to quickly and easily change your rider’s term coverage to whole life insurance without having to answer health questions or take a physical examination. ”

what do they mean by “your rider’s term coverage to whole life insurance”? I was under the impression that I purchased Dividend option Term rider to increase death benefit and it is permanent. but now they are saying that it is term coverage?

I called them but they never pick up. Please help me understanding.

Hi Rick,

This is most likely a term rider that is attached to your whole life policy. You most likely own a blended whole life policy, and the term rider that makes the blend is convertible to whole life insurance. Alternatively, you can allow paid-up additions purchased by dividends to replace this term insurance over time. You’ll have to check on the exact functionally of how PUA’s replace term insurance with New York Life for your specific policy.

Is your agent still around? You could also look up the nearest NYL agency and call them. They’ll put you in touch with an agent if your original one is no longer available.

Hi,

My father has a policy with PUA’s and the cash value has increased nicely as described in your blog. My question is about the total death benefit, It has increased significantly from the base death benefit but I noticed that in the last 4-5 years the total death benefit is dropping by about $5k each year. Why?

Hi Cassie, is he still paying a premium on this policy?

Amazing write-up Brandon

I’ve recently constructed a whole life policy with PUA. I won’t break even on my cash value until the 12th year. I’ve heard of policies having break even periods of as low as 5 years if constructed properly. How do I best minimize my break even period and does the MEC affect the break even period?

Hi Jim, yes the MEC does affect the break-even period. The design reason for the long break-even period might be a function of the company, or it could very likely be that you’re not maximizing the design. You are correct to assume that you should achieve break-even status sooner than 12 years. We do have a policy review service to help get you pointed in the right direction, click here for more information on it.

Can you take value of PUAs on a whole life insurance policy and cash them in and apply to a loan against the policy?

Yes you can do this.

Hello Brandon,

Please make me understand. There is a $20k PUA face amount and A $10k PUA cash value. Can i borrow money from either of those? There is also a $8k maximum dividend available. Which one of those I can borrow. I need to buy a car as i cannot work without a car.

Thank you

Jese

Hi Jese,

You can borrow against the cash value of the PUA. The insurance company can provide you with the maximum loan amount you can take against the policy. You can simply call their customer service department or look this up if you have an online account for your policy.

Interesting blog. I have a whole life policy put in place 50 years ago when I needed life insurance. I no longer need life insurance, but do need long term care insurance. I am borrowing against the cash values on the life policies to cover the LTC premiums.

My agent has given me the option of surrendering paid up additions vs. borrowing as a way to finance the LTC premiums. Am I correct that by taking the surrender route I will forego future cash value increases arising from the paid up additions? That suggests to me that borrowing against the policies may make better sense, assuming I can cover the annual interest costs, so as to keep the loans from compounding to much higher levels.

What am I missing in this analysis?

Mike M.

That may very well be the correct approach if you seek to optimize cash value over your lifetime. You are correct that loans will allow you to continue to earn guaranteed interest and dividend (to some degree) on the paid-up additions that you do not surrender. Whether this results in a net positive benefit to you depends on the loan provision of the policy.

I am the beneficiary of a whole life insurance policy which I have just put in a claim for. The policy has a face value of 1 million and over 25 years there have been pua’s which total roughly 850,000.00 I received a statement which lists the basic face amount of 1.4 million and pua’s as 0.00. Can this be right? The customer service phone line is atrocious and I don’t understand where there math is coming from.

Assuming the initial information ($1mm death benefit and $850k PUA’s) this does not sound correct. Death benefit should be $1,850,000. Again, assuming that information is correct.