Podcast: Play in new window | Download

Whole life insurance, and other forms of cash value life insurance, enjoy numerous tax benefits that make them sought after financial products. These benefits can be found among other financial tools, but together they represent an impressive package of tax-friendly features well worth a look. These combined benefits become especially interesting to Americans in higher income tax brackets or individuals with more than just a few thousand dollars in assets (especially when those assets are appreciated in value or sit in qualified accounts).

Today we're going to walk through the many tax benefits of owning whole life insurance.

Tax Deferred Cash Value Accumulation

The cash value that grows inside an insurance policy does so tax deferred. This means that as the account balance grows each year, the policy owner will not owe taxes on the change in his/her account balance.

For example, assume you own a whole life policy currently with $100,000 in cash value. Over the next 12 months, that cash value grows to $106,000. You will not be responsible for paying taxes on this $6,000 growth in your cash value.

This feature of life insurance differs considerably from other financial tools that do create a tax liability for any increases in value achieved throughout the year.

Think about your savings account. If there is $100,000 in there at the beginning of the year, and that balance grows to $101,000 through interest earnings throughout the next 12 months, you will receive a 1099-INT early the following year reporting taxable earnings of $1,000. You will owe ordinary income taxes on this $1,000.

There is a significant compounding benefit to tax deferral over time. Because taxes aren't due on the growth unless you remove the gain from the policy (or cancel the policy) the gain will continuously compound in its entirety. Mathematically this means you'll end up with a much larger account balance because you don't have to remove money each year to pay taxes due on the growth of funds inside the policy.

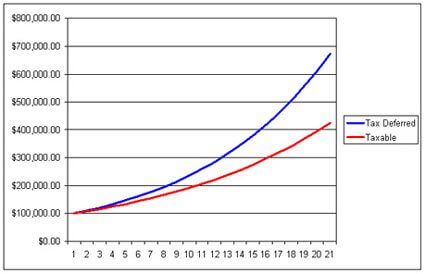

The image below shows the difference in account balance growth between a taxable and tax deferred account over 20 years.

As you can see, the tax deferred account grows to a much larger sum after 20 years. Both accounts earn the same amount in terms of rate of return each year, but the because the tax deferred account doesn't have a tax bill to pay each year, it can compound more dollars year-over-year.

As you can see, the tax deferred account grows to a much larger sum after 20 years. Both accounts earn the same amount in terms of rate of return each year, but the because the tax deferred account doesn't have a tax bill to pay each year, it can compound more dollars year-over-year.

FIFO Accounting Principle

Life insurance policies use the First In First Out (FIFO) accounting principle. This means that you can withdraw the money that you contribute to your policy first and the gain achieved by the policy second.

For example, assume that you had a whole life policy with $500,000 in cash value. You've paid a total in premiums of $300,000. You want to make a $50,000 withdrawal from the policy. This $50,000 withdrawal is non taxable because you can take it from the $300,000 you contributed to the policy.

In fact, you can take all $300,000 back out of the policy if you want and there is no taxes due on this because it was your money that you used to pay the premiums of the policy.

Non Taxable Policy Loans

All life insurance policies with cash value have a feature that allows you to access the money through an automatically approved loan issued by the insurance company.

A life insurance policy loan does not count as income to you so there is no tax due when you take a loan out against your policy's cash value. Policy loans are a way people access cash in their policies after removing the cost basis and keeping the distributions tax free.

For example, assume you have a whole life policy with $1 million in cash value where you paid a total in premiums of $400,000. You've reached retirement and now wish to use the cash in your whole life policy to generate some of your retirement income needs. You decide that you will take $60,000 per year from your policy. For the first six years you can withdraw your cost basis out of the policy to generate the $60,000 income. Beginning in year 7 you will remove your entire cost basis so to keep the retirement income you generate from the whole life policy, you begin using policy loans to create the income. Doing this for now on ensures that your $60,000 per year income from the whole life policy remains tax free.

So long as the policy remains in force until the say you die, you will not owe taxes on the income that you took from the policy.

Unique Tax Treatment of Dividends

Dividends earned on a whole life policy enjoy a special tax benefit when taken as a cash distribution. Whole life dividends come with an array of different options, and one of those options is to simply take the dividend payment in cash.

If you chose to do this, tax law recognizes whole life dividends as a refund of the premiums you paid. In other words, you can use the FIFO principle applicable to withdrawals for any dividends you take in cash from your policy. This shields some dividend distributions from being recognized as ordinary income to you.

So unlike stock company dividends that normally come to you as ordinary income and carry and income tax liability, you can receive whole life dividends tax free assuming you have not exhausted the cost basis of your policy.

Tax Free Death Benefit

In general, life insurance offers an income tax free death benefit. This means that the death benefit payable on a life insurance policy goes to the beneficiary(ies) without an income tax implication to them. This has a subtle, but very significant implication regarding how whole life insurance can create a substantial tax free savings and legacy account for a policyholders.

Remember that all cash values inside the whole life policy accumulate without immediate tax liability because cash value grows tax deferred.

If the policyholder does not remove the gains generated by the cash value from the policy, but instead withdrawals his/her cost basis from the policy and then uses loans to access the cash value comprised of gain, he/she will owe no taxes on the money “distributed” from the policy.

When the policyholder dies, the death benefit goes to his/her beneficiary(ies) without income tax liability owed by either the policyholder/insured or the beneficiaries.

So this means you can build up cash value in a whole life policy, use either the FIFO withdrawal to basis or policy loans to access the money built up in the policy without paying taxes on it, and then pass the remaining death benefit on to your heirs all with no taxes due on any of the gains every created by the policy. Whole life insurance is a substantial way to build tax free wealth.

The Whole [Life] is Greater than the Sum of its Parts

The various tax benefits afforded by whole life insurance (and other cash value forms of life insurance) are powerful on their own, but when combined into one neat package, the synergies become quite attractive. Sure you can find one or two of the many tax benefits whole life insurance has to offer among other financial vehicles, but you cannot find all of them together in any other financial product available.

I await your next article entitled. “Tax Benefits of indexed Universal Life Insurance.” written with same even-handed approach.

Thanks Brandon. Very interesting and helpful. Could I ask you to clarify one point? One of your examples describes my situation almost exactly. In that example, you state:

“Beginning in year 7 you will remove your entire cost basis so to keep the retirement income you generate from the whole life policy, you begin using policy loans to create the income. Doing this for now on ensures that your $60,000 per year income from the whole life policy remains tax free.”

Are you saying to take out loans and not pay them back (because I wouldn’t have any income to pay back loans)? I know that’s possible but it has implications. Just trying to understand the mechanics of this approach. Thanks!

Hi Ken,

That’s is exactly what I’m saying. There are a few important steps one should take to begin this process and ensure that they aren’t taking too much from the policy to risk a lapse in the future due to exceedingly high loan balance. Just like someone should do some risk testing on an investment balance when they begin taking withdrawals to ensure that over time the sum of those withdrawals won’t draw the balance to zero too early.

The process involves looking at current and projected values given the planned income amount to assess soundness of the income amount. Then it’s prudent to check on things periodically (once a year or once very couple of years) to ensure that things are still working as planned.

Thanks Brandon, super helpful response and makes sense to make sure your loan balance doesn’t get too high and to manage that appropriately. Is it safe to assume that the unpaid policy debt is paid from the death benefit prior to payment to any beneficiary?

That is correct Sue. If there is an outstanding loan at death, the insurance company will deduct that balance from the death benefit and pay the remainder to the beneficiary(ies).

Cool. I wouldn’t have considered withdrawing money as a loan at that point in my life. But I understand and I’ll look into it more closely now. Thanks!

As someone who currently has a life insurance plan in place, I never would have drawn attention to the tax benefits. It definitely sheds more light on this plan that I’ve been using and allowing to grow on its own.

Hi Brandon my whole life policy was paid by my waiver of premium since I am diabled.since I did not pay those premiums. is my cash value in my policy over the death benefit taxable when I die and she gets the proceeds.

Hi Kindred,

In general the death benefit should not be taxable in this case. But you should always consult a tax professional to render a final opinion on this.

Hi guys

I just got a chance to listen to this podcast, sorry for the late response.

Thanks for the concise summary of the tax treatment of policy cash value and death benefits.

And thanks for talking about policy dividends and how they could be used as a source of retirement income.

Brantley made a point that I haven’t heard before: policyholders should consider dividends as an alternate source of retirement income when it comes to deciding which source to use to avoid sequence of returns risk. I don’t recall reading this point before in industry literature, but it is one more powerful tool in the life insurance tool box when it comes to using life insurance as a retirement savings vehicle.

Hi Harry,

Thanks for leaving a thoughtful comment. Isn’t it funny how we forget about the basics sometimes? Of course, I talk about dividends with clients every day but it’s easy to overlook the basic value of benefits that are inherent to whole life insurance. You could even take part of a dividend in cash if you wanted to. We should all remember to view whole life insurance like a Swiss Army Knife. Not the perfect solution to every problem but a solution that gives us a variety of capabilities.