Podcast: Play in new window | Download

Somewhere along the way, retirement planning and particularly retirement income planning came completely off the tracks. However, there is a way that you can fix it for yourself and that's by learning a simple methodology to create your own pension. A retirement income stream that deposits a certain amount of money into your bank account every month like clockwork.

But first, a disclaimer: the information below opposes conventional wisdom with regards to planning for your retirement. I’ve been directly involved in all sides of the retirement planning industry (stocks, qualified plans, all types of annuities, insurance, discounted cash flows, bonds, mutual funds, separately managed accounts, limited partnerships, etc.). Not looking to impress you but just to let you know that I’ve peeked behind the curtain, seen the Wizard and I’m not impressed.

Now that we got that out of the way, I can spend less time talking about what’s wrong with the retirement planning advice business and more time talking about what we can all do better. What we can do better for our clients, for ourselves, and for everyone we know.

When exactly did this train wreck happen?

I’ve done my homework, and it’s really tough to put a finger on the exact date when things went awry; however, the problem really began to rear its head sometime in the early 1980s. This is when corporate boards and executives decided it would really be in the best interest of their employees (nudging each other with elbows) to adopt defined-contribution plans (enter the 401k) in lieu of the defined benefit plans (or more commonly known as pensions) that had been the norm for the previous 60 years or so.

So, this immediately put the responsibility of providing a retirement income squarely on the shoulders of the employee.

Please don’t misunderstand me. I’m very much in favor of personal responsibility and seizing the opportunity to control your own destiny.

You Are Responsible For Your Retirement Income

In other words, I would never suggest that my retirement or yours is the responsibility of an employer or of the government for that matter.

However…

The problem with almost all of the advice that people have been given over the last couple of decades is that it heavily relies on a “pie in the sky” rate of return assumption. Most financial “gurus” will suggest that if you save at least 10% of your gross earnings and earn a 10% average rate of return, then you’ll be all set.

I disagree with that assumption.

Within that flawed logic, you are too heavily relying on the rate that you earn over your working life. I hate to break the news to you, but you have absolutely no control over that rate. Furthermore, to average 10%, you’d have to do something akin to a very successful streak of winning at the blackjack tables in Vegas.

And whoever came up with some static percentage as a “rule of thumb” for how much of your income should be dedicated to retirement savings? This figure can vary wildly depending upon how much money you make, how much income you need later on, and what your goals are.

That’s perhaps the weakest link in the strategy.

Honestly, this is just the wrong way to solve the retirement income problem.

So, what’s the right way to figure this out?

I’m glad you asked.

Actually, it’s pretty easy and it is a throwback to a bygone era when people actually used absolutes to plan for the future. Who’da thunk?

Okay I’m done being sarcastic…I promise (scout’s honor)

What’s old is new again.

I’m suggesting the way you should really plan for your future retirement is to figure out how much money you’ll need to live comfortably in the future. How do you do that? Well, the best methodology is to be realistic.

Determine what expenses you’ll have–to the best of your ability, how much you’d like to have for leisure etc. Then you’ll just back into how much you need to save to create that income.

You don’t have to be a math wizard like our resident mathemagician, Brandon Roberts. In fact, you can use a few different online calculators to help you and have your answer in a matter of minutes.

Simple Strategy to find your “number”

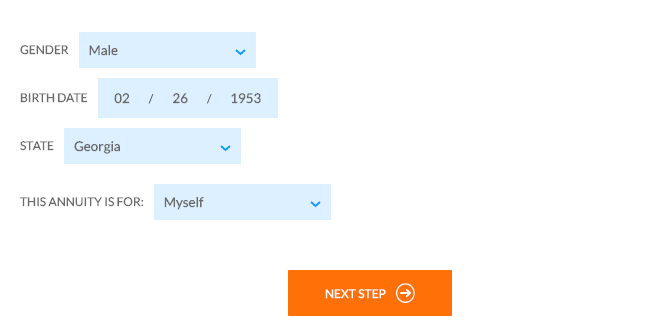

1. Go to https://annuityfyi.com –Fill in your resident state, choose a birthday that reflects the age you'd be today if you were to retire. That's probably a little confusing but for example, I am using 2-26-1953 as my date of birth because I plan to retire when I'm 67 and I'd like for the calculator to show me a number based on that age (the calculations are based on your life expectancy) and the amount of monthly income I would like to to have when I get there.

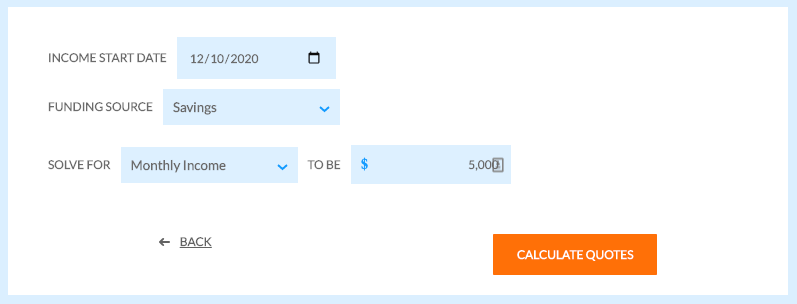

2. Press “Next Step” and a new page will appear with a few more boxes to fill. Scroll down to the option that says “Solve For”. Then use the down arrow to toggle the option to solve for “Monthly Income”. For the example here, I chose $5,000 per month and my income start date is 12-20-2020.

Your screen will look like this after making all the above selections:

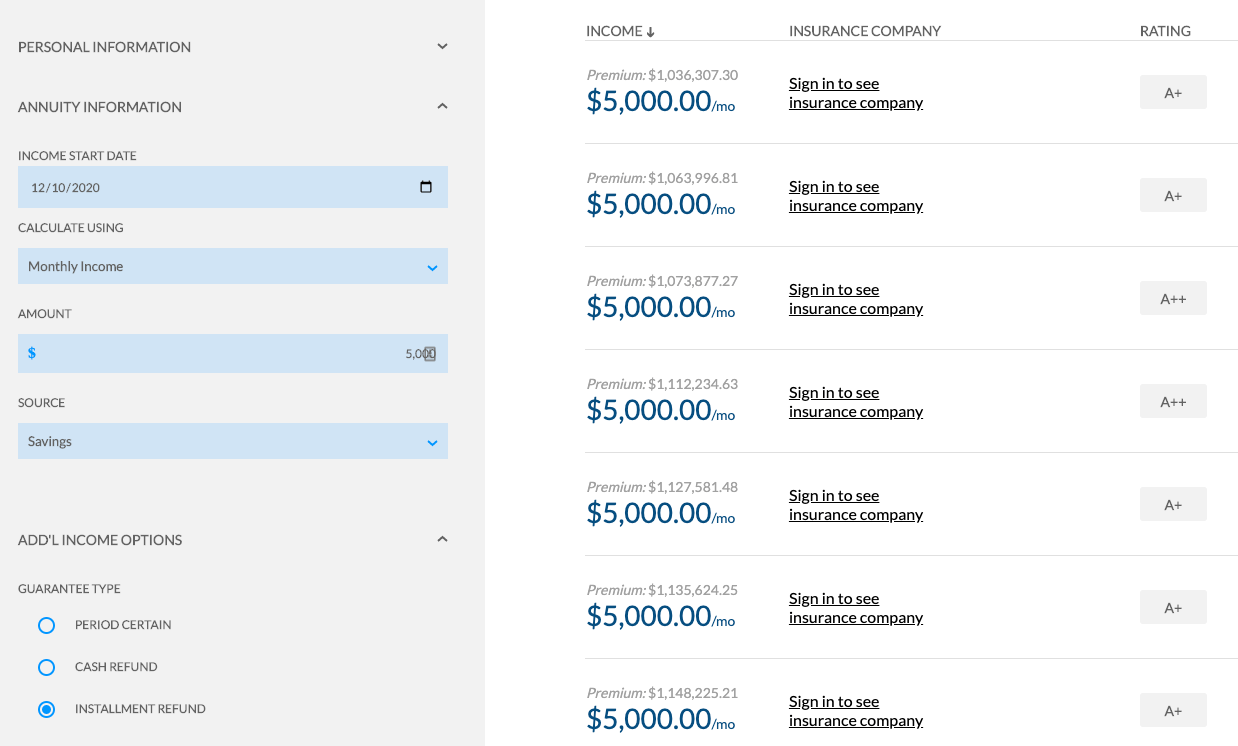

3. After pressing the Calculate Quotes button, you'll have the “number” that you’ll need to have in your bucket to generate the income you desire. If you look in the top row, you'll see that you would need to deposit (pay a premium of) $1,036,307 today to guarantee that you would receive a $5,000 monthly income for your life beginning in December 2020 and that your beneficiary will receive a refund (installments) of any unpaid premium that you deposited when you die.

The other numbers on the rows beneath are for other insurance companies. We don't know what companies are quoted here because you'd have to go further in their process to be privy to that information. But it's worth pointing out that there is a difference. For example, the third option down would cost nearly 40k more to guarantee the same income stream for life.

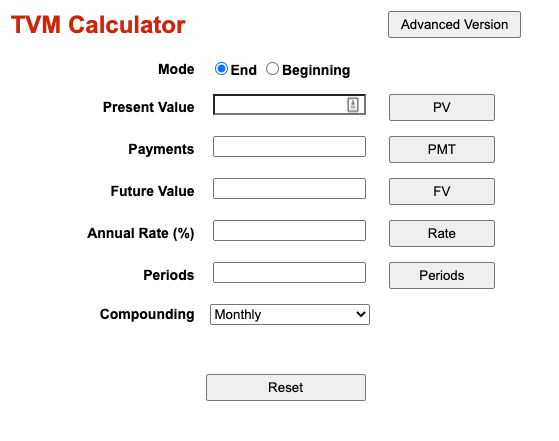

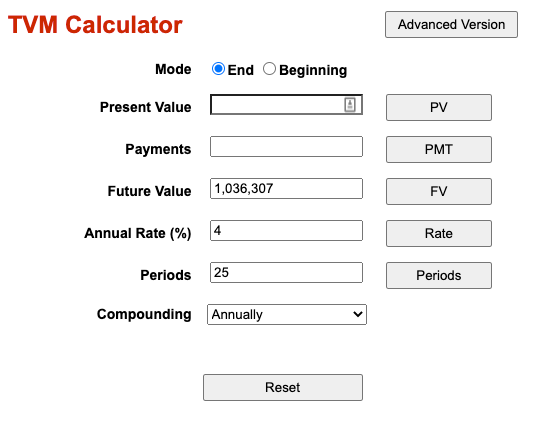

4. HOWEVER, this is only if you retired today. So, in other words, you’re not quite done. Click the link to head over to a rather generic site, Financial Calculators and you should see the TVM calculator in front of you.

5. Don’t be intimidated. We have to do a little math here but all we're doing is plugging numbers into the Time Value of Money calculator to tell us how much we need to put away each year assuming a very conservative 4% inflation rate over the next 25 years. Conservative in that we're probably going to end up with a higher annual required savings number than we really need.

You should see this when you first load the page:

6. Now we're going to take the amount was from the annuity quote that we dug up on AnnuityFYI.com and plug it into the FV (future value) field.

7. In the rate field type in 4. This is the rate we’re using as our rate of return to get us to the “number” over the next 25 years. We use 4% because that’s a super conservative number that most insurance actuarial tables rely on to make safer assumptions and we’re comfortable with that. Here is exactly what I typed into the calculator to get the results.

8. Then we put in the number of periods. In my example, I used 25 periods because I was performing the calculation on myself. I’m 42 and planning to retire at 67, thus 25 years away.

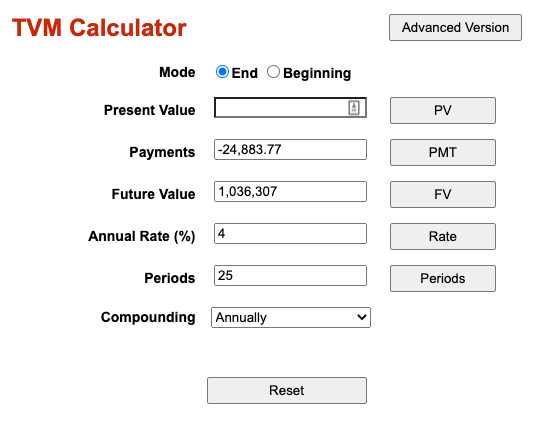

9. Finally we click the button labeled “PMT” and the number we need to save on an annual basis to get us to our number, $1,036,307 will appear in the PMT field. In my example, it’s $24,883.

So, what does all this tell us…

It tells us that we better get serious about stashing away some cash to take care of ourselves down the road. To drive home that point, I first performed this calculation back when I was 35, and using the annual savings needed to achieve the same result was only $14,501. The cost of waiting is expensive and becomes exponentially more so each year.

Many traditional financial planning types will propose that my methodology is arcane, crude, and far too simplistic.

They’ll say that using a 4% rate assumption is far too conservative a number and that the market has averaged closer to 8% throughout history. (If you believe that then you should check out my post on compound annual growth rates.) I mean you could end up saving too much money.

As a financial professional for the last 20+ years, I've never had anyone tell me they saved too much.

But what if you assume an 8% return and only average 6%?

I’ll tell you what…you’re either not retiring when you wanted to, or you’re accepting a lower standard of living in retirement. Those are your only two options at that point.

I don’t know about you, but I’d rather plan on earning a lower rate on my savings over my lifetime and be pleasantly surprised when I do better. See, if I plan on 4% then I’ll save more money than a guy who plans on 8%. The engine of my plan is driven by the amount of my savings and is not dependent upon an unpredictable rate of return.

In that scenario, who has more control?

I do.

I can control how much I save; he can’t control what his rate of return will be.

So, next time you hear some talking heads blabbering on about how to plan for your retirement, keep in mind that the way it was done years ago, is still the right way. Plan on what you know you’ll need to generate the income you want and then save enough money based on a conservative rate of return to get you to your destination with ease.

That’s it.

Then you don’t need a company pension, you’ve saved enough money to make your own pension that works every time. This sort of planning doesn't rely on some overly complicated models based on probability and statistics.

There will come a day when we all have to generate an income from our retirement savings, that’s not probable–that is a certainty. And you’ll be much better off having a certain strategy to get you there.

If you’d like to learn more about how we help people plan this way, contact us—we’re happy to help.

Whoa! 10 ads for Clover Health. I’m sold. JK!

Good blog and podcast IPB Bro’s. Love SPIAs! The other side of life insurance – living too long. Personal Pension options are directly related to whole life insurance. It’s a strategy we were taught at Guardian… Ideally, for every dollar owned of whole life insurance coverage, that’s a dollar that can be annuitized, and eventually replaced by the death benefit proceeds. Also, annuitization often guarantees a higher payout than the 4% withdrawal rule of thumb. As we know, a major drawback with a maximum life SPIA payment is giving up principal and losing it at death. The insurance effectively solves the return of principal problem. Good show!

BTW – Why is annuitization always considered misspelled? Wall street removed it from Webster’s … 401konspiracy!

Perhaps you may want to calculate the amount needed at retirement to produce an income for life for you and your spouse (unless you are not married)…a joint SPIA, which produces less income in your scenario. Also the SPIA rates that are used today are much lower than historical averages….which range between 6.28% to 13.28% from January1986 through January2020 for a 65 year old. I for one do not think these current rates will remain at their current lows, but may start going back to their historic norms over the next decade or two…which of course decreases the amount of monthly savings to produce the income you indicated. Having said that, using todays rates makes sense, and if the SPIA rates do increase so much for the better. Thanks for the information