Podcast: Play in new window | Download

If you have extra cash, time, and an open mind, whole life insurance is worth it. Over the long term, you can expect to earn returns similar to bonds and secure lifetime death benefit coverage that your beneficiaries will receive tax-free.

On the other hand, if you're young, just getting started in your career, and only have a couple of thousand bucks a year to make premium payments, you should buy term insurance for now while you still have excellent health.

The best life insurance companies will allow you to convert your term insurance policy to whole life later when you have a larger budget without a medical exam. Locking in the premiums for an affordable term life insurance policy is a good move. When you do that, you are also locking in a guarantee that you have some life insurance coverage that can later be converted to permanent coverage.

If you've been doing a lot of research about the different types of life insurance products (universal life insurance policy, term insurance, variable universal life) and whole life insurance policies, in particular, you're wrestling with a lot of conflicting information.

Whether or not whole life is worth it for you, will depend on your circumstances and where it may fit into your portfolio as part of your future financial plans. It depends on what you want to accomplish.

But if you choose to purchase a whole life policy or any type of permanent life insurance, remember that there is a “right way” to set up your policy if your primary goal is to buy a policy that builds cash value.

We help our clients maximize the policy's cash value accumulation with whole life insurance and occasionally an indexed universal life policy as well. We help hundreds of people do this every year and coach life insurance agents, financial advisors, and other financial professionals to do the same.

But at least a few times a week we're faced with questions like, “does it really work?”, “is it worth it?”, or our all-time favorite “can you send m

Whole Life is a Good Decision

As a matter of fact, we've met a lot of people who own whole life insurance and most of them didn't buy policies from us. Most of these discussions have started without us initiating any sort of sales presentation. We never had any intention of selling life insurance to them and they had no intention of buying a policy from us.

When people ask me what I do for a living I tell them “I sell life insurance“. As you can imagine, nobody wants to get into a discussion about life insurance premiums or riders at a social function. Or they tell me about the term life policy they bought to cover their spouse and pay off the mortgage.

While the majority of people hear me say life insurance and look for an exit from the conversation, some stick around and are eager to share their stories. It's often a tale of how they purchased permanent insurance and held onto it for a while. Fascinating stories to say the least.

Eyes light up a bit and they say something like “I have this whole life policy I bought from XYZ company back in 1970 something, and let me tell you that was one of the best decisions I ever made!”

Why would someone suffer the early expenses with a significant portion of their discretionary income just to leave a juicy payout to their heirs?

Because that boring whole life policy now has a boatload of cash value that they'd never have if they'd tried to save it some other way–their words, not mine. I'm not coaxing that response from people.

Just how much cash value you might ask? Let me give you an example.

Real Numbers from Whole Life Insurance Policies

Almost three years ago, we published this piece on the subject of “badly designed” whole life insurance and how it could work out quite well. I want to recap the numbers from this example.

That article was special for two reasons.

- It had substantial historical data–36 years to be exact–on a whole life policy

- It reported numbers from a whole life policy issued by State Farm–a company that has completely changed focus away from dividend-paying whole life insurance

Using the data provided in the comment, we calculated the effective internal rate of return on this whole life insurance policy; it turns out it achieved a 6% return over those 36 years.

Could Jim (the contributor who shared the information on his whole life policy) have done better if he had invested that money in the stock market, rental property, etc?

Maybe. But who knows and would he have been willing to take on the risk?

Would he have had the intestinal fortitude to stay fully invested in 2000, 2001, and 2002 when the market fell by double-digit percentages for two straight years?

Who knows if he would have stayed fully invested in 2008 when losses would have been well over $100,000 as the market “corrected.”

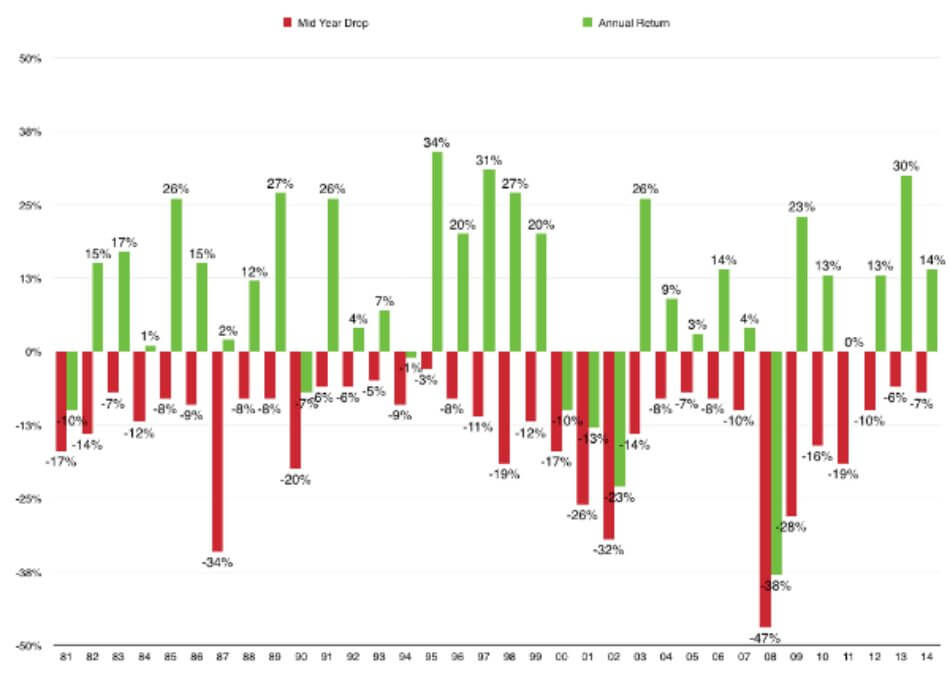

Take a look at this chart, it gives you a great idea of what happened in the S&P 500 during that time period on an annualized basis. It also shows you the drawdowns that happened within each year. That last data point is so important and almost nobody talks about it, we're always focused on annual returns.

However, we all have to overcome our own emotions and markets don't fluctuate in perfect synchronization with the calendar. Take a look:

The one thing Jim likely never worried about during any market decline that came after he bought his whole life policy was where his whole life insurance cash value was. He probably also never worried about it when CNBC, Bloomberg, or any other financial media outlet speculated that this or that major news headline “spelled trouble for the stock market.”

Your Policy Should Maximize Cash Withdrawals

If plain whole life policies from yesteryear have worked out pretty well, what about the ones that were customized to produce boatloads of cash surrender value?

We took a look at policies we've put in force to compare against the original illustrations (projected values based on the current dividend rates at that time). Most policies have been in force for five years or more and a few of them were issued by companies that have since reduced the dividend paid to whole life policyholders versus the dividend assumed when the policy was bought.

No denying that there has certainly been a reduction in the policy's cash value vs. the original illustration. But everyone knew this could happen when the policies were purchased and the premiums were being paid. Permanent life insurance policies, including whole life, provide a great deal of financial protection against all manner of economic calamity.

But they are not immune from reality either–like the prolonged period of low-interest rates from 2008-present.

The difference, however, is not all that substantial. In raw dollars, no policy is down vs. the original projection by any more than a few thousand dollars, which on average comes out to less than 1.5% off its original projection. If we look at the internal rate of return, this is less than a 0.5% difference vs. what was originally projected in the illustration (on average)

For major one mutual life insurance company, kept their dividend unchanged for over a decade so none of those policies have cash values that were any different than what was originally assumed as long as the client paid the premium as originally planned.

Oh and here are the historical numbers from a maximized policy issued in the early '90s. It achieved a return of over 7% for the years shared.

Wrapping it Up

Despite some small reductions in dividends and lower cash value balances, we don't hear much in the way of complaints or concerns about whole life insurance. In fact, we've seen several policyholders take advantage of the built-in flexibility to increase the premiums they pay by dumping additional money into their policies.

These people all think that whole life insurance is worth it. They continue to pay their premiums each year. Life insurance protection to last your entire life, a decent rate of return, the ability to access cash tax-free, and stability for your financial plans are all very appealing.

Does it make you curious to see how a whole life policy might work out for you? If so, feel free to reach out (click here to contact us) and have a discussion with us. A short conversation can determine if it's a strategy worth pursuing.