There are three main types of life insurance: whole life, universal life, and term life insurance. In each of the three broad types, there are many variations of each but we will take a look at the broad categories while pointing out a few of the finer points of each type.

And just to be clear, this website will not ever tell you that one type of life insurance is better than any other. Each category serves its own unique purpose for unique circumstances.

Remember, first and foremost that life insurance exists to pay a death benefit to your chosen beneficiary(s) when you die. Nearly all types of life insurance also offer some sort of living benefit nowadays as well.

Okay, let’s take a look at the three main types of life insurance now.

Whole Life Insurance

Within the realm of whole life insurance, you may stumble upon it being referred to under different names. The two most common other than calling it whole life are “straight life” or “permanent life”. We will spare you the history lesson and only add that whole life insurance is the original type of life insurance. It has been offered in its most modern form since the nineteenth century.

Within the realm of whole life insurance, you may stumble upon it being referred to under different names. The two most common other than calling it whole life are “straight life” or “permanent life”. We will spare you the history lesson and only add that whole life insurance is the original type of life insurance. It has been offered in its most modern form since the nineteenth century.

If you are looking for absolute guarantees, there is no product that compares to whole life. In addition to its promise to pay a death benefit if the premium has been paid, it also offers a very stable and safe savings plan. There are all sorts of opinions on the internet about whether whole life is any good, whether it is worth it, and/or is it just a total ripoff.

Try our whole life insurance calculator to see how it might work for you.

From personal experience, we can say definitively that it’s not a ripoff. That being said, it should be used appropriately for the right people. Policy design, setup, and service are extremely important for the policy owner to have a satisfactory outcome, particularly when looking at the savings component which is formally called the cash value.

Back to the guarantees for a moment as that is the crucial component for whole life. There are three basic ones:

- A guaranteed rate of return on cash

- A guaranteed cost that will not change and is locked in when you purchase

- A death benefit that is guaranteed to last for your “whole life”

There is a lot more detail to discuss but can read more about all the more detailed aspects of whole life by clicking right here.

Universal Life Insurance

One of the earliest descriptions that I ever heard regarding universal life insurance was that it was “built on a term insurance chassis”. Well, that sounds good but to most normal people (I was normal back then) that does not do quite enough to accurately define it, so let’s try to do better.

Universal life insurance is really a term insurance policy with a savings component attached to it. Just like all other types of life insurance, there is a raw cost to insure your life. In a universal life policy, this is known as the cost of insurance and it is clearly disclosed for you. At its core, you must pay enough premium to cover the cost of insurance to keep the death benefit that you purchased in force.

But you also have other options to cover the costs. If the savings component has cash value (there’s that phrase again) the policy expenses or costs can be covered in whole or in part by the cash value. Universal life insurance is very flexible in that there really is no set premium. You only have to cover the cost of insurance and perhaps a few other expenses to keep the death benefit in force.

Your cash value will have interest credited to it at least annually in most cases. How much and what the interest is based upon is an entirely different discussion and something we have other content that explains more in-depth, you can check that out by going here.

Back the basics of universal life: the term portion of the policy works very much like yearly renewable term insurance as the cost increases a bit each year. It starts out very inexpensive and moves up as you age. This could become a problem and has for some people.

However, as you will read from us or hear from us repeatedly, this only becomes an issue when the policy is incorrectly designed, implemented, and managed. Do not let this deter you from exploring universal life. There is a great deal of misinformation out there that intimidates people into ignoring it as an option.

Term Life Insurance

It will not take quite as much space to accurately explain term life insurance to you. That is because term insurance is very simple.

Remember when you were in school and your teacher told you that you couldn’t use the word itself to define the word on your vocabulary tests? Yeah well, I’m gonna break that rule because I’m not sure how else to do it in this case and this is our site so we can do what we want to.

Term life insurance actually gets the name from the fact that it is life insurance purchased to cover you for a specified period or term. At the end of the term, your level, fixed, and the affordable premium is over and so is your coverage.

Well, that really describes level term life insurance which is offered most commonly in 10, 15, 20, and 30-year terms. There are other types of term insurance but they are largely fading into the past and not entirely relevant anymore. Those other types are decreasing term and yearly (or annually) renewable term insurance.

The vast majority of term life insurance sold today is level term insurance (10, 15, 20, or 30 year level periods).

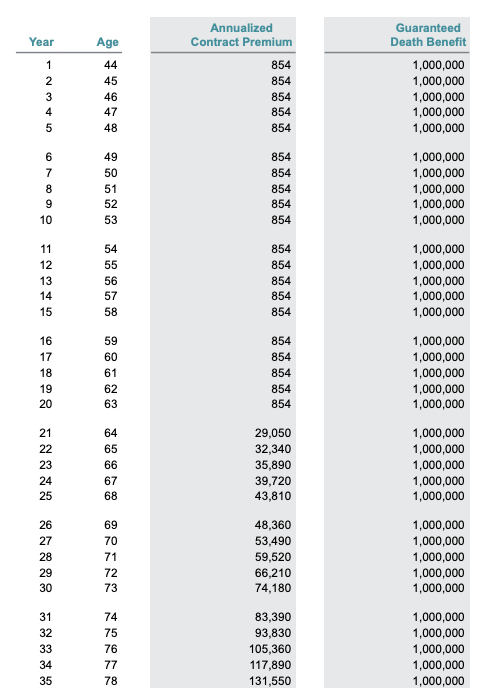

In most cases at the end of the term, the life insurance company will allow you to continue the same coverage but at a greatly increased cost. Here’s an example:

This is a 20-year term policy for a healthy 43-year-old with a $1,000,000 death benefit. You can see the annual cost is guaranteed level at $854 for 20 years. But when the insured turns 64, if he would like to keep the coverage in force, the premium jumps to $29,050 per year. That is a very substantial jump.

To add one more important detail that is not mentioned above with term insurance…the cash value. That’s because unlike whole life and universal life, term insurance has no cash value or savings component. It is pure insurance offered for a period at an affordable price which makes it a very popular option for those who need a particular amount of coverage to replace their income if they die.

Let’s Put a Bow On It

Each of the three main types of life insurance serves a unique purpose. Do not be enticed by detractors to feel that one is better or worse than another.

Whole life insurance is great for those with a greater amount of discretionary income, a long time horizon, and the desire for safety with strong guarantees.

Universal life is infinitely flexible and can offer better returns on cash value over time if designed, executed, and managed properly.

Term insurance is the utility player of the bunch. It offers inexpensive death benefit protection for those who have a finite need. It works particularly well for a primary breadwinner that needs to make sure their income is replaced for their family when they die.

All types work well and should be considered when you are looking to purchase a new life insurance policy. Choose the right one for your specific need or want. And if you would like to discuss purchasing a policy, please contact us, we're happy to discuss it with you and to help you get the policy you need. In addition to being a resource for life insurance information, we are also agents and work with clients all over the country.

After paying more than $33,000 over the last 30 years to Transamerica I was shocked to learn that I have absolutely no value in it . In fact if I don’t pay them over $1500 immediately they will cancel my policy. In addition I am expected to pay $400 a month. What did I do wrong.

Hi Charles, It’s tough to say specifically what you did “wrong” in this case. It’s probably the case that you ended up with a policy that had far more death benefit than reasonable for the premium that you paid during the past 30 years. Have you discussed any options with Transamerica to reduce the death benefit?

what is the best type of life insurance policy to purchase for the estate planning purpose above 60 years old.

What is the best company to purchase from?

What institution that I should use to shop for the best quote ?

what is the best strategy to use to optimize current estate law together with life insurance

Hi J, “Estate planning” can encompass a wide scope of insurance needs, so there is no answer to your current questions. You’ll need to refine them further.

Early 30’s couple having our first child. We currently have no life insurance other than the meager if killed while working, our respective jobs pay something to a beneficiary. Is there a one stop comparison shop for life insurance? Both of us are healthy with no previous health conditions.

Hi Lindsey,

If it’s just death benefit protection you need to replace lost income, then I’d seek out term insurance immediately to ensure that you both have coverage as soon as possible. There are a number of places online that you can check out to get a good idea of the cost and compare products such as AIG Direct, Select Quote, and Policy Genius. These companies will be term life only resources.

Looking into permanent life insurance is a much more involved matter, which might make sense for you, but I’d address your need with term insurance first for the meantime.

I’m 60 years of age. Thinking of getting life insurance. What do you believe would be the best insurance for me

Hi Chris, that information alone isn’t enough to make any recommendation to you on the best insurance for you. You should meet with an agent/broker and discuss more details to arrive at what the best option is.

I think wholelife insurance is appropriate one..u must choose this one..

Thaanku

Both types are great but whole life insurance much great with no complications,,,

Universal life insurance too complicated

Hi. I recently lost my father and had to scrabble around to pay for his funeral expenses. I quickly realized that I need to have some preparations in place to avoid leaving my children in the same position I had just faced. I need help to I select the best policy and insurance company for me. I’m lean in my towards an Universal policy.

Hi Tesha,

Sorry to hear about your father. What makes you think a universal life insurance policy is right for you?

My husband and I are 30 years old and we figured if 2020 has taught us anything, it is to be prepared (financially) for the worst. We are first-generation Americans that want to set up security for our children. At this age is there anything for us to particularly look for? After reading this, it looks like I should look into whole life and universal life insurance?

Hi Luisa,

I need a little more information on what setting up security for your children means to you, then I could probably offer up a few ideas to get you started in the right direction.

My husband and I are both in our 40’s. My husband has some health problems. We are looking for life insurance that will help the other one financially if one of us would pass away. We have 2 children and a mortgage. But a policy that we wouldn’t lose the money over time. You had spoken about how some policies were like savings accounts as well as life insurance policies. Would that be something you would suggest?

Hi Sarah,

It’s difficult to say based on what you shared if cash value life insurance policies make the most sense for you and your family. While I understand your desire to not potentially buy a policy that ends with no payout and no cash value to you, you may find that the alternative (term life insurance) ends up being your best bet with regard to getting adequate death benefit coverage. I say that to encourage you to keep an open mind as you consider your options. Cash value products can do great things, but if you need a specific amount of death benefit and the premium needed for a cash value product is beyond your budget, it’s a terrible idea.

Im Over 60 and need to purchase a life insurance policy. Am I to old to get a whole life,or universal life policy?

Hi Freda, this might make sense. We don’t enough about you to make a recommendation at this point. You can reach out to us through the contact form if you wish.

I’m a 45 years old father of 2 thinking about buying a life insurance which one would you recommend. And if you suggest just term policy,should I do it for 20 or 30 years?

Hi Fisher, this unfortunately isn’t enough information for us to make any specific recommendation to you. If you’d prefer to discuss with us in detail, please feel free to reach out to us through the contact form on the website. Thanks!

Thank you for this article. I appreciated this!

Hello, I will be 55 next month. I am permanently disabled, living in a fixed income from SSI/disability. I am a mom to 7 children and 6 grand children. I knodo know that it’s wise to purchase a life insurance at this point. I do not want to leave my family with the hardship of funeral expenses. I would like something with a little more benefit, beyond just funeral expense. Is there anything kind of plan that may meet my low income baseline. Anything that may be affordable in my situation?

-TIA

Hi Alice, the type of life insurance you are looking for is commonly referred to in the life insurance industry as Final Expense. This is not a type of insurance we can help you buy. It is my understanding that some of the tele-agencies are beginning to focus on this product line so you might be able to reach out to them and get information. Select Quote is one option that I know is selling this line of life insurance as they’ve discussed it publicly in their earnings calls. They might be worth reaching out to.

Hello. Just turned 50 and wondering about the possibility of getting a policy for around $250,000 that in the event 15 or 20 years down the road if i need money to cover costs for whatever comes up, I could get a loan from the policy. Basically I want a safety blanket in case I need one. Is this possible and if so what would you recommend. Thank you for your time.

Chris

$250,000 was a typo … meant 50,000 or anything like that.

Hi Chris,

Where are you located?

If you want add another amount to your policy that you have for ,14 years term life will you have to wait two years for it to pay.

Hi Nadine, this depends on the type of policy you are buying. Waiting two years for it to pay sounds like a graded policy, which would refund premiums for the first two years and then pay the death benefit in the event death occurs after two years. If this is type of policy that you own and you are looking to add more coverage with this type of policy then yes there would be a new two year period where the death benefit would potentially not be paid.

I am needing to know if a prepaid funeral plan would be as good or better than paying for life insurance. My intentions are not to leave a bundle ofmoney for my kids, but rather enough for burial expenses. What are your thoughts on this?

Hi Peggy, pre-paid funeral plans will generally be more expensive than life insurance, but without knowing the specific details about the pre-paid funeral offer and your personal health, it’s tough to say which option is the best bet. The type of life insurance you would compare this against is referred to as “final expense” insurance (think the type of policy you used to see Alex Trebek talking about on TV for Colonial Penn). You could always contact an agent who sells final expense insurance and get a quote to compare to the price you get from the Funeral Home for pre-paid service.

Hello I’m a 54 year old married to a 56 year old man in soso health, I’m healthy. I’m looking for life insurance that will provide me with the security that if anything happens to one of us we would be able to live financially ok. I really don’t want to worry about my premium going up thru out the years and I don’t want to worry about getting canceled for some stupid reason. Also I don’t want to wait years to see the benefits so what do you recommend?

This is a very premature recommendation based on very limited information, but you might be a candidate for guaranteed universal life insurance. This is a permanent type of insurance that cannot lapse so long as you pay the premium.

How much is its life insurance coverage?

What is the underlying link investment?

How much is the premium cost? What is the payment term? When is the due date?

What are the breakdowns of the policy charges?

Hi Ahra,

This blog post isn’t about any specific policy.