Decreasing term life insurance is a special form of term life insurance designed to cover a borrowing obligation. It's rare for life insurance agents/brokers to sell this type of life insurance. Instead, loan officers such as mortgage brokers and F&I managers at car dealerships are the people who traditionally sell this type of life insurance.

What Decreases in Decreasing Term Insurance?

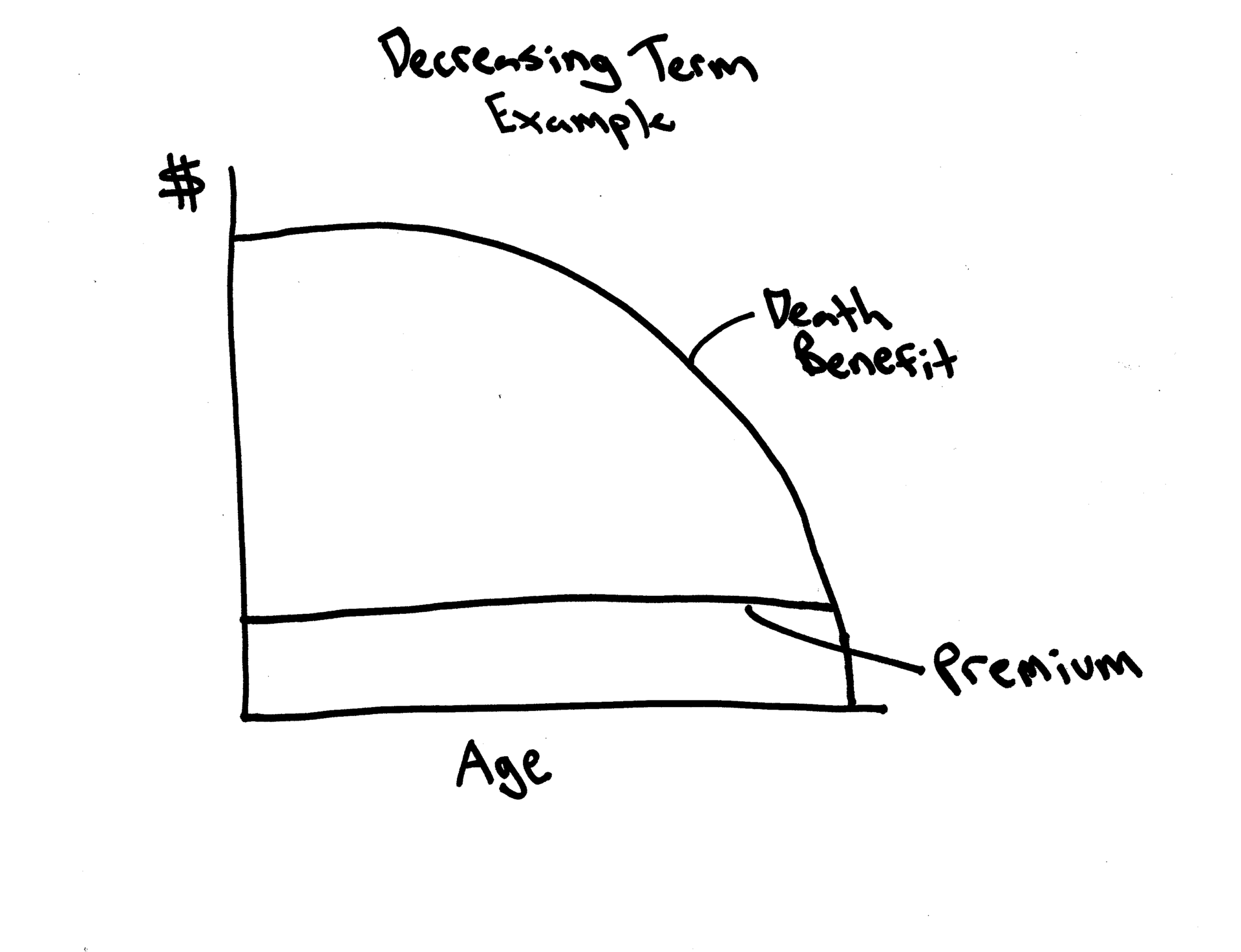

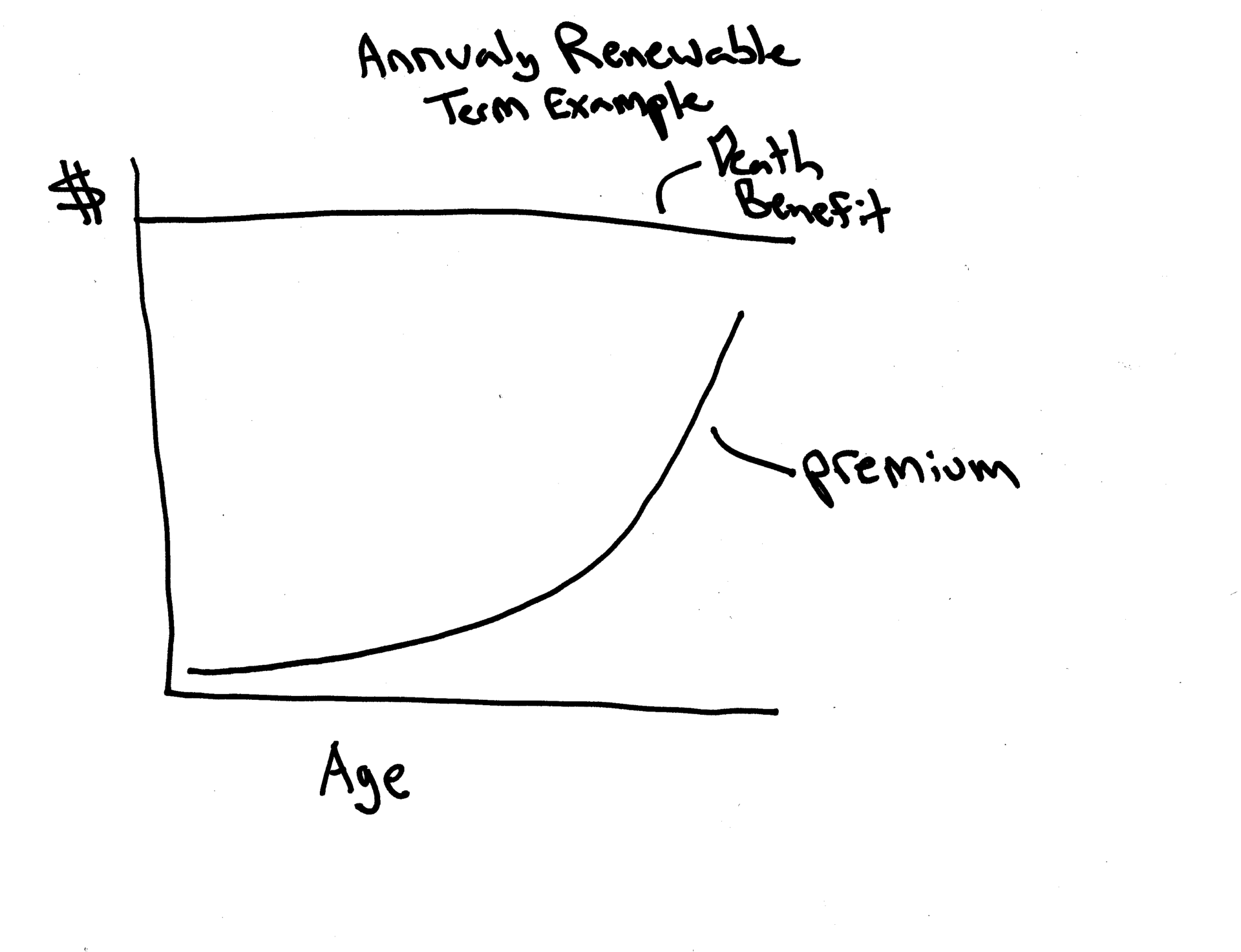

The death benefit amount decreases in a decreasing term policy. The death benefit matches the loan payoff, so with every loan balance payment, the death benefit amount will decrease. The cost of a decreasing term policy, however, remains the same. So instead of having a periodically increasing premium for the same death benefit like annually renewable term insurance, decreasing term life insurance has the same premium, but an ever decreasing death benefit.

Here's a graphical comparison of decreasing term life insurance and annually renewable term life:

Personal/Specific Asset Protection

The spirit of decreasing term life insurance is specific protection in a financial interest. For example, assume that you need to borrow money to purchase a new car. You will borrow $30,000 to make the new car purchase. If you die before you repay the loan, your spouse will be responsible for loan repayments.

One way to protect your spouse's financial interests is to purchase decreasing term life when you take out the loan. Should you die before you repay the auto loan, the decreasing term policy will automatically repay the loan for you. Your spouse will then own the car free and clear of any debt obligation.

It's also common to find decreasing term offered on mortgages. If you opt for a decreasing term life insurance option on a mortgage, you know that should you die before paying off the mortgage, your spouse and/or loved ones will not need to continue to make mortgage payments. Instead, the decreasing term life policy will pay off the mortgage upon your death.

Example of a Decreasing Term Life Insurance Policy

Assume that you are buying a house and will need to borrow $300,000 as part of the purchase. During the mortgage application process, the broker asks if you would like a decreasing term policy on the mortgage. Note, the mortgage broker will rarely refer to this as a decreasing term policy. Instead, he/she will likely refer to it as a feature or protection to pay off the mortgage if you die.

You will pay an additional $65 per month as part of your mortgage payment to have this benefit. This $65 monthly payment will not change for the remainder of your mortgage, but each month when you make a mortgage payment and reduce the principal balance of your mortgage, the amount of death benefit you have for this $65 will go down. The death benefit will go down by the amount of the pay off balance declines on your mortgage.

Should you die before you pay off the mortgage, the decreasing term life policy will pay off the mortgage for you. This will leave your spouse, or whomever you wish to have the real-estate upon your passing with the house without the need to pay the mortgage.

Advantages of Decreasing Term Life

The major benefit of decreasing term life insurance is its ability to prevent loss of assets due to debt default when a borrower dies. This will protect the financial interests of a spouse or other loved one because they will not shoulder the responsibility of repaying the debt.

Another upside to decreasing term insurance is the automation it uses. You can often receive approval for the coverage when you close on the purchase and there is no lengthy underwriting process. Decreasing term also retires the debt obligation almost instantly and avoids the need for a beneficiary to handle the pay off process.

Lastly decreasing term life insurance provides peace of mind as you know that death will not risk the loss of a house or other major financial purchases due to an inability to pay the loan off.

Disadvantages of Decreasing Term Life

Decreasing term insurance is rather expensive life insurance. Most individuals will find they can acquire the same or more death benefit protection for a substantially lower premium with a traditional term life policy.

The decreasing term policy is permanently tied to the debt obligation and cannot cover a different death benefit need. If you repay the loan early, the decreasing term policy terminates. If you borrow again, you must opt for another decreasing term policy; you cannot bring an existing decreasing term policy to a new loan. This is especially important in the case of a refinance. Refinancing debt will terminate an existing reducing term policy and require you to opt in to a new one with the newly issued debt.

While the underwriting process of a decreasing term policy is streamlined, it does require you to be able to satisfactorily answer some questions. If you cannot do this, you may be ineligible for a decreasing term policy and will not have the protection it provides.

decreasing term to pay off 6 year truck loan

Hi Bill, unfortunately, I can’t help you with a decreasing term policy, as those are only sold through lenders. You should reach out to the bank that issued the truck loan.