Podcast: Play in new window | Download

“Whole life insurance/universal life insurance is a terrible investment because the rate of return is horrible.” We've heard that before. You don't have to wander the interwebs far to find someone peddling this bologna. If you don't believe me, see here, here, here, and here. None of those four authors hold a license to sell life insurance, but I digress.

Though we’ve addressed this statement a few times on the Insurance Pro Blog, I wanted to distill the point many people miss into one simple notion that should be approachable by just about anyone.

Rate of Return…Focus your Attention Over Here

When it comes to personal finance (and all the various subsections thereof) few terms are used in a more misleading fashion than the rate of return.

The mutual fund industry has enjoyed confusing arithmetic mean and geometric mean for decades. We also see financial pundits “cherry pick” their favorite periods of time to support the case for being invested in the market. They want you to believe that investing in the stock market is an imperative.

But what does rate of return even mean for you and me?

Answer this question to yourself (that way you’re less apt to lie): If I could guarantee an adjustment to your savings/investment plans that guaranteed an 8% annual rate of return over the next 10 years, would you know what to do with the money you made? Don't lie now.

Most people wouldn’t, and this is the trap that most of us step into when it comes to the rate of return on various savings/investment options. It's swell to make an awesome return for a given period time but then what?

I can't even begin to tell you how many people have told me they were thrilled with their investment portfolio because it returned X percentage points over Y number of years. They proclaim this with a certain chest inflated pride, but then sheepishly deflate and ask “that's good, right?” Sigh…(insert eye roll here).

A Retirement Income Case Study

Keeping pace with the promise that I want my point to be so simple a caveman could do it, and hammering on the notion that retirement planning is about what you can actually do with your money, I present you with the following scenario:

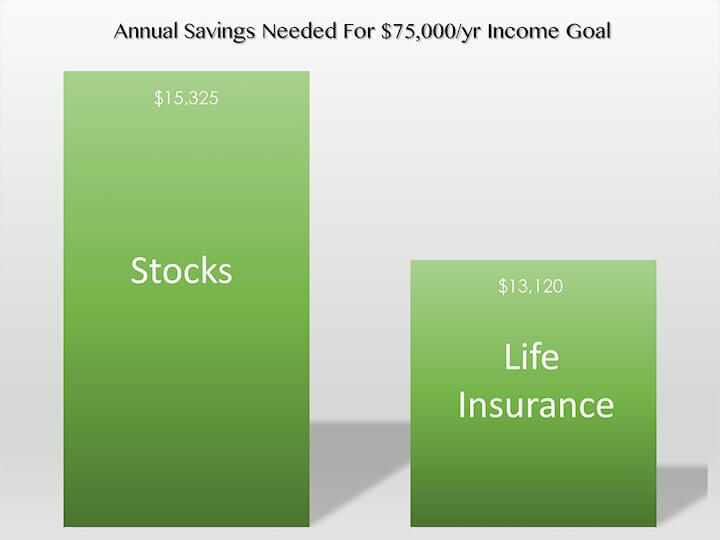

A 35-year-old male wants to target a retirement income of $75,000 commencing when he turns 66.

He’s going to earn that elusive 8% compounding annual return on the stock market we often hear about (though several sources don’t believe in it), and using the old 4% rule about safe withdrawal percentages (whatever it inflates the numbers a bit in favor of stocks) we determine the need is $1,875,000 at retirement to generate his target income.

Given these parameters, we can easily calculate the sum he needs to save each year at $15,325 (assuming he makes his investment at the beginning of the year all at once).

Now, how much do we have to save if we want to generate this same income amount using life insurance?

I’m going to use an indexed universal life insurance policy for this. We’ll assume the policy’s average index credit earned is 6% per year.

The premium amount needed to achieve an annual income in retirement of $75,000 per year is $13,120 per year (again assuming the premium payment is made at the beginning of the year). That’s $2,205 less committed each year than needed for the stock market investment.

For what it’s worth (not much) the annual rate of return given cash value by age 65 is 5.75% per year for the indexed universal life policy. 2.25% less per year vs. the stock investment for those keeping score.

Let's recap. It's possible to achieve greater buying power (i.e. do more with your money) on a savings plan that has a lower compounding annual return. Why? I hear you cry out. Because not all money you have functions the same way.

Focusing on the rate of return may cost you money

That $2,205 difference could buy a lot of things each year. Or it could be added to the life insurance policy and simply generate more than $75,000 per year.

The important take away here is that simply picking the option with the higher rate of return doesn’t always mean you end up with more.

I enjoyed your podcast on the episode 95, as well as many others, I would like to get the blog version but it’s not showing.

Thanks for letting me know Sam! Just made a major site upgrade and sometimes things just don’t work exactly as they should.