Podcast: Play in new window | Download

Back in 2015 we published this blog post detailing a scenario looking at whole life insurance as an alternative option to buying bonds. The details for the individual who approached us included a desire to invest a sum of $500,000 into bonds, so we looked at how we could best deploy that cash into a whole life policy.

With that approach to whole life, we'd then compare the internal rate of return projections to evaluate how it performs compared to prevailing bond yield. The whole life policy projected a 10-year internal rate of return of 4.66% and a 20 year IRR of 5.72%. This compared very favorably against bonds.

Not only was the projected IRR considerably better than bond yield, but whole life can also compound return where bonds cannot.

What I mean by this statement is that bond yields go to the investor a payment per the interest obligation of the borrower. The investor/lender receives the payment on whatever periodic schedule established at bond issuance. The bond investor does not have the automatic option to reinvest the bond income.

He/she can choose to reinvest bond income but must find additional investments to do this with the income received from the bond. Whole life insurance, on the other hand, will take any earnings for the year and keep them in the policy (if desired) and this allows the whole life policy owner to compound returns inside the policy.

Here's a video we created some time ago to explain how this works with whole life dividends and paid-up additions:

By the way, if you're curious about Predictable Profits, you can find more information about it here.

Revisiting Whole Life and Bonds in 2021

It's almost always appropriate to revisit analyses we did several years ago to see how things changed over time. We have a number of these we need to do, and we're working through several of them. Several things have changed since 2015 chiefly:

- Economy-wide interest rates are lower

- Bond yields are lower

- Dividend rates on all whole life products available in 2015 are lower today

- Whole life products changed

Creating a new whole life policy today given the same set of circumstances from 2015, things are certainly different. The one data point that probably everyone is most interested to see is the change in the internal rate of return. The 10-year IRR is 3.47% and 20 year IRR of 4.57%.

This is considerably less than it was roughly five years ago. Is this due to lower interest rates and lower dividend rates? In part, yes, but that's not the only factor at play.

While lower and sustained interest rates have definitely impacted dividend rates on whole life policies resulting in lower projected returns, we cannot overlook the impact product changes have on policy performance. The product we used in 2015 no longer exists as an option for new whole life buyers.

The company retired it at the end of 2019. In fact, all insurance companies rolled out new whole life policies at this time due to an adoption of an updated mortality table used as a basis for life insurance pricing. This new table forced death benefits slightly higher for cash-focused life insurance purchases and this results in a higher overall expense to cash value life insurance moving forward.

If we look at the in-force data on the policy used in 2015, we see a reduction in IRR due to the lower dividend rate, but it's not as substantial. The in-force data shows us that the old policy projects a year 10 internal rate of return of 4.35% and 20 year IRR of 5.41%. Why such a difference?

Again, the older product was simply a better product regarding cash value accumulation, but there are yet more factors at play. The new product assumes that the policy will only ever earn the current (lower) dividend. The old policy from 2015 actually earned dividends at a higher rate for a few years and now basis future projections of the current (lower) dividend.

The cash value accumulated during the years that the old policy actually earned those higher dividends are now permanently part of the policy's cash value, and no one can take that away. This boosts not only the non-guaranteed cash value but also the guaranteed cash value.

There is a real risk to waiting to buy a life insurance policy and it's far more complex than just the time lost and advancement in age. Keep in mind I'm not assuming an older insured in this above example, the new policy for 2021 assumes the same age insured from 2015. If we advanced the age of the insured five years, the results compare even less favorably.

How Have Bonds Changed

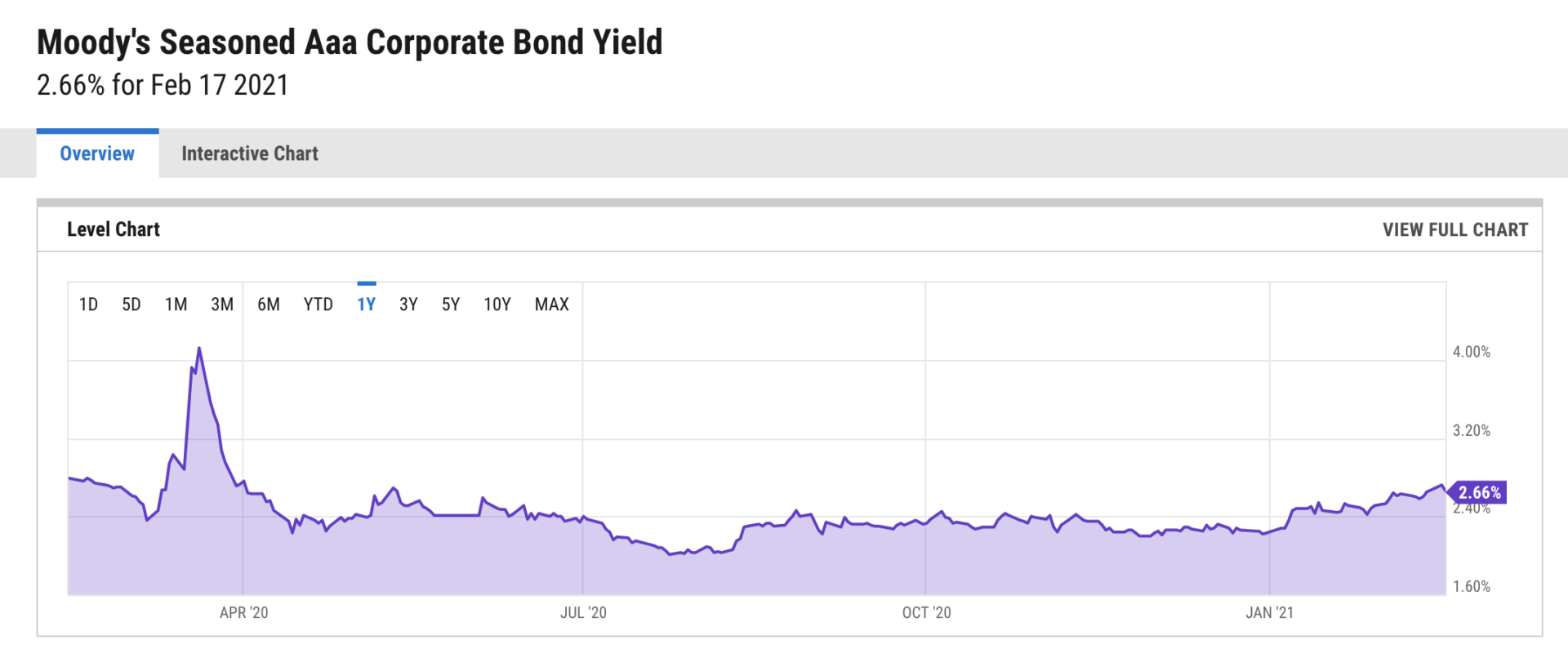

The spirit of the original comparison was looking at whole life as a bond alternative. Returning to that original question, we see it still compares very favorably. Back in 2015, the average yield for a Aaa-rated corporate bond was 3.54%. Now in 2021, it's 2.66%:

This means the yield on Aaa-rated bonds fell 25% during this time period. For whole life, the drop is slightly less at 22.5%.

We've noted for years that whole life doesn't operate in a vacuum, and here we see direct evidence of that. We also shouldn't forget that whole life continues to boast a higher overall return versus Aaa-rated bonds. Additionally, whole life insurance offers far more liquidity and ease of access.

So whole life remains ahead of a solid bond investment with a similar risk profile. And whole life will compound returns whereas bonds require significantly more legwork to create compounding returns.

One could opt for bond funds to introduce better liquidity and easier compounding, but this also introduced additional risk as bond convexity becomes a more serious concern–especially in ultra-low interest rate environments.

While I’m a huge fan of Whole Life and paid-up-additions, and if comparing it to a bond portfolio with bonds purchased at par value and held to maturity, your comparison is on target, for an investor investing in bonds and taking advantage of CAPITAL GAINS on the bonds as interest rates drop, you might have not made a complete comparison.

Hi Oren,

Thanks, please expand more on what you mean.