Paid-up life insurance is a term that confuses a lot of people. The idea seems straight forward, but what makes a life insurance policy paid-up? Also, how does paid-up life insurance differ from other types of life insurance? We hope to help you understand all of this today

Paid-up Life Insurance is Whole Life Insurance

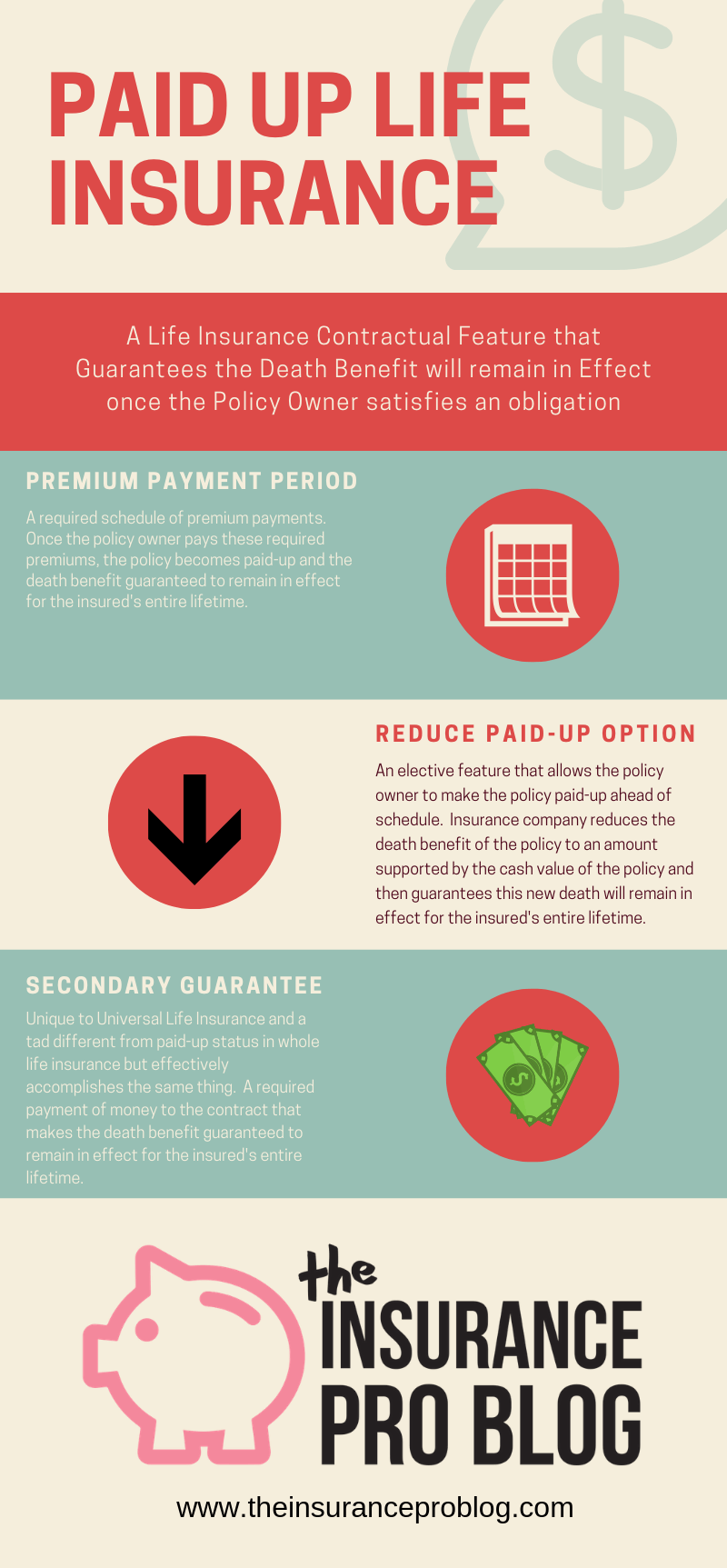

Admittedly, paid-up life insurance isn't really a type of life insurance but rather a condition of whole life insurance. All whole life insurance policies have a paid-up provision that works in one of two ways.

First, the policy becomes paid-up once the policy owner satisfies the premium payments necessary for paid-up status.

Alternatively, the policy becomes paid-up when the policy owner elects to trigger the reduce paid-up feature of his/her whole life policy.

Regardless of the method, once paid-up the policy is guaranteed to remain in effect for the rest of the insured's life. More importantly, the death benefit of the policy is guaranteed to be valid for the insured's entire life.

I want to take some time to explain the two paid-up conditions in a little more detail.

Satisfying the Paid-up Requirements

All whole life insurance policies come with a schedule of required premiums. The insurance term for this schedule of premiums is the “premium payment period” (how creative), and it's often a defining feature of a whole life contract.

If you look at various whole life products available for sale, you might notice that they make references to a “paid-up at” age or a specified number of years before being paid-up. For example, you might find a Whole Life Paid-up at age 100 policy or a 10 Pay Whole Life policy. These examples give a pretty good explanation of the premium payment period right in the name of the product.

Not all whole life policies put the premium payment period in the policy name. Some companies choose to give their products fancier names and make you dig a little deeper to discover how many premium payments you need to make to make the policy paid-up.

Regardless of the name, the premium payment period clearly identifies the number of premiums the policy owner must make to satisfy the paid-up feature of the policy. Once this occurs, the policy requires no future premiums and will remain in force accumulating cash value and earning dividends (if participating in dividends) on top of providing a death benefit.

[thrive_text_block color=”blue” headline=”Paid-up Life Insurance Premium Payment Period Example”]Kim owns a whole life policy paid-up at age 65. Kim purchases the whole life policy at age 40. This means Kim must pay premiums for 25 years. After Kim pays the premium on the life insurance policy for 25 years, the policy becomes paid-up. Kim stops paying premiums but gets to keep the policy in force. The death benefit still exists, and the cash value continues to accumulate. [/thrive_text_block]

Triggering the Reduce Paid-up Option

If the policy owner wishes to cease premium payments before reaching the end of the premium paying period on a whole life policy, he/she can elect to make the policy paid-up with a lower death benefit. The industry calls this a reduced paid-up option.

The life insurer will evaluate the policy's current cash value and calculate the death benefit amount supported by that current cash value amount. This newly calculated death benefit will be less than the current death benefit on the policy and becomes the effective death benefit after electing the reduced paid-up option.

The policy owner no longer pays premiums on the policy–it is paid-up–but also must understand that some of the death benefit he/she had prior is now gone. For some people, this is more than a reasonable trade-off. Others, however, might need to reconsider this option is death benefit needs are high.

While there is a reduction in death benefit when using the reduce paid-up option, the accumulation of dividends, could potentially create a death benefit that is larger than the original death benefit even after triggering the reduce paid-up option. This happens when the policy owner chooses the dividend option to purchase paid-up additions.

Paid-up Life Insurance and Dividends

A common concern voiced about paid-up life insurance focuses on the continued payment of dividends. Some people worry that they will lose their dividends if they have a paid policy. This is not the case. Paid-up policies continue to earn dividends if they are participating policies that received dividends before the paid-up status.

The amount of dividend could vary, however. Some life insurers do have different dividend scales applicable to older paid-up whole life policies. This isn't necessarily a common practice and generally not worth worrying about when it comes to making a whole life policy paid-up.

Non-Whole Life Paid-up Life Insurance?

I mentioned earlier that paid-up life insurance was actually a function of whole life insurance, which  suggests that only whole life insurance can be paid-up life insurance. This is technically correct, but functionally not 100% true.

suggests that only whole life insurance can be paid-up life insurance. This is technically correct, but functionally not 100% true.

It is true for all term life insurance policies. You cannot have paid-up term life insurance because term life insurance exists for only a time (i.e., a term). No matter what premiums you pay towards a term life policy, the life insurer will never guarantee the death benefit remains in effect for your lifetime.

You also cannot make most types of universal life insurance paid-up. While it's possible to manipulate a universal life insurance policy in such a way that it becomes effectively paid-up, the guarantee that it will always remain in effect does not exist. And that guarantee, remember, is a critical component to the technical definition of paid-up.

However, some universal life insurance policies do come with a paid-up feature, it's just not called paid-up. Some universal life insurance policies have a feature known as a secondary guarantee (these policies often go by the name Guaranteed Universal Life Insurance).

This feature provides a guaranteed death benefit be in effect for the insured's entire life provided he/she meets a specific contractual obligation. This obligation often looks like a premium payment period similar to whole life insurance, but functionally it's a sum of money paid to the policy to meet the guarantee's requirement. I know to the layperson this seems like a silly game of semantics, but I assure you there are technical elements here that are critically different and important.

So while technically we don't really refer to these types of universal life insurance as paid-up life insurance, they are in effect the same thing, because they also guarantee that a death benefit remains in effect for the insured's entire lifetime.

How can you borrow cash from a Whole Life “Paid-Up” Policy; and not, effect the value of your policy and not have to start making payments again if possible.

I’m afraid this question is too broad and I can’t figure out what it references.

But in general, any loan taken from a whole life policy does not affect the cash value insofar as cash value remains in place. It might affect the dividend payable on the policy. No making payments depends on the amount of money in the policy and how long the insured of the policy reasonably expects to live

What happens in the reduce paid-up WL surrender option if the onsurednlives past 100?

*insured lives past 100?

Hi Allison, this depends on the product. If the product is set to mature at age 100, it will still do this. If the product is set to mature later than this, then nothing happens.

My wife and I are both 77 years old, in reasonably good health and still living in our home. I (husband) have a Long-Term Care Insurance policy pitchased a number of years ago. My wife did not qualify medically for a policy at that time and she has no Long-Term Care coverage.

We are considering purchasing a paid-up whole life insurance policy so we can draw on that if, or when, she needs it to pay for long-term care expenses and our children will have to pay less tax on their inherintance if there is anything left in the policy.

Does this sound like a reasonable thing to do ?

Hi Jim, it could be. There are certainly products out there that address exactly what you are talking about. Be aware that some products will cover temporary loss of activities of daily living and some will require the loss be deemed permanent by a medical professional.

What you’ve described doing is one of the primary ways people are addressing this need these days. The purchase of traditional Long-term care insurance is rather uncommon now.