We don't often talk about the endowment life insurance policy. This is largely due to the fact that they are no longer a thing in the United States. But just because you won't find them for sale doesn't mean there aren't still endowment policies in existence. So let's take the day to explain these special life insurance contracts as we weep softly over the fact that you can no longer buy them.

Oh a really quick note, I do not mean Modified Endowment Contract, which is an entirely different thing that is certainly available “for sale” in the United States today.

What is an Endowment Policy?

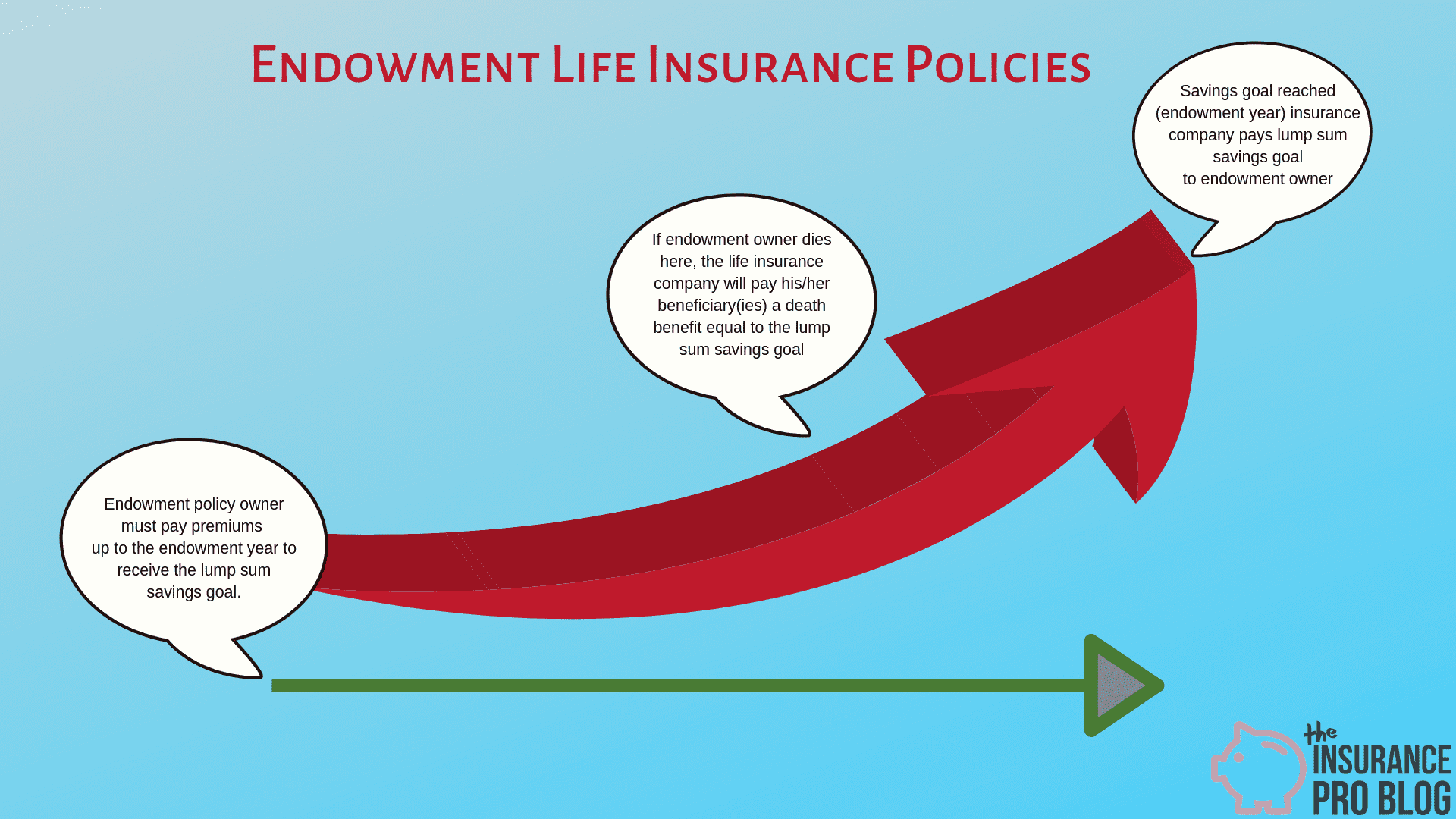

The endowment policy was a form of life insurance that worked as a savings plan for the purchaser. At the outset, the buyer (usually also the insured) selected an amount of money and the life insurance company computed a premium required to achieve that savings goal at some future date (often the buyer's age 65).

Endowment Policy Example

Mortimer wishes to save $250,000 by the time he turns 65. He decides to do this through an Endowment Policy. The premium he needs to pay is $4,000 per year. If Mortimer pays this premium every year, the life insurer guarantees that he will have $250,000 at age 65, which he will receive as a lump sum payment.

Once the buyer reaches the age selected under the contract to achieve the savings goal and receives the guaranteed lump sum amount he/she selected at policy inception, the contract “endows.” Endowment is simply an insurance term for finalizes or matures. It's the point when the premiums paid satisfy the buyer's obligation to receive the cash benefit he/she chose.

But wait, there's more…

Endowment contracts also have a life insurance component. If at any point prior to the endowment year the buyer dies, the life insurance company issuing the endowment policy will pay a death benefit equal to the savings goal amount to the named beneficiary(ies) of the endowment policy.

Death with an Endowment Example

Sadly, Mortimer doesn't make it to age 65. He passes away 10 years early. The life insurance company that issued his endowment policy will pay his beneficiary $250,000 immediately.

Dividends Paid to an Endowment Policy

Endowment policies were often participating contract meaning they earned dividends paid very similarly to the way life insurance companies pay dividends to whole life insurance owners. This often created endowments with much more cash value, death benefit, and ending value than originally purchased.

Endowment Dividend Example

Mortimer purchased a participating endowment and earned several dividends while paying premiums. He was on schedule to receive a lump sum payment of $350,000 instead of his original $250,000 benefit. When he passed away, his beneficiary received $300,000 due to increases created by dividend payments.

Dividends paid on endowment contracts functioned with the same tax friendly features whole life dividends enjoy today. They acted as a tax-free refund of premiums paid to the policy owners.

Borrowing Against Endowment Policies

Just like whole life insurance, endowments permitted loans against cash values. If the policyholder needed cash and wanted to take a loan against his/her endowment contract, he/she had this option. Loans functioned identically to the way loans work with other life insurance policies.

Loans had no tax consequence while the endowment remained in its premium paying period and the policyholder was free to repay the loan however he/she saw fit.

There was one special consideration for those who borrowed against endowment contracts. If the endowment reached the endowment year and paid the lump sum cash benefit to the owner, the contract ceased to exist. This would make any gain distributed through a loan against the endowment taxable ordinary income to the policyholder.

Tax Consequences of Endowments

Just like ordinary life insurance, the cash value of endowment policies accumulated tax-deferred. Distributions from endowments through loans took place tax-free.

But…once an endowment reached maturity and the life insurance company paid the policyholder the lump sum cash benefit, the cash received came to the endowment owner as taxable ordinary income. This had the potential to cause some problems for individuals with additional tax problems due to high income.

There were, however, a few options to avoid such problems. First, the policyholder could transfer the endowment via 1035 exchange to a new endowment policy with a longer endowment period (if one existed). Alternatively, the policyholder could choose to transfer the cash in an endowment to an annuity contract to continue to defer tax liability on the accumulation of cash values. Old tax law on annuities favored this strategy since annuities at one time enjoyed first-in-first-out accounting for distributions–this is not the case today. This made it possible to transfer the endowment cash value to an annuity, withdraw the basis from the annuity tax-free, and then let the gain continue to grow tax-deferred.

What Happened to Them?

Endowments were an unfortunate casualty of the laws that put speed limits on excessive universal life insurance contributions. Once Congress established life insurance qualifications tests that sought to limit the amount of cash value and/or premium that could exist inside an insurance contract relative to its death benefit, endowment contracts no longer fit the definition of life insurance.

The accumulation of cash value inside endowment contracts was quite high by life insurance standards and this led to contracts that deferred a lot of taxes for a while. This coveted feature was also the endowment's undoing.

Once tax laws changed in the 1980s and endowments no longer qualified as life insurance, they no longer benefit from the many tax favorable features life insurance enjoys. As a result, the life insurance industry stopped offering them with one small exception.

The Gerber Life Grow-Up Plan® is an endowment contract, and this is why the Grow up Plan doesn't tout tax benefits in the same way many life insurance contracts bring them up.

While the endowment policy no longer exists for sale, people who bought them prior to tax law changes still benefit from them. They can still receive their lump sum benefit at the endowment. They can still borrow against them with no tax liability while the contract is still in the premium paying period. They can also choose to transfer the cash via 1035 exchange to an annuity (not to a life insurance policy) if they want to–but they can't use the old FIFO trick to withdraw basis tax-free.

Or they can simply take their lump sum cash benefit all the while knowing that if they die before the day the life insurance company owes them the benefit, their beneficiary will receive the lump sum instead, earlier than originally planned, and tax-free because it's a death benefit.