Podcast: Play in new window | Download

Some questions came up following last week's discussion about Ernst & Young's analysis on various retirement strategies. The gist of a handful or so of these questions focused on the buy term and invest the difference scenario, basically did the hypothetical couple continue to pay term insurance premiums into retirement? We don't know the answer to that question, but there were a few who posited this question while noting that keeping term insurance into retirement would be a bad idea.

I find the suggestion that keeping term life insurance into retirement is a bad idea to be a very “privileged” point of view. I don't mean this in the context of race or social class, but rather in the sense that things have simply worked out well. It's sort of like the middle-class relative we all have who got lucky and managed to never experience much financial down-turn in their life who likes to opine whenever there's a rumor about concerning a mutual acquaintance's misfortune. “Looks like they aren't good at managing their money,” these people often suggest–all the while knowing very little about the adversity-stricken individual's particular circumstances.

I want to directly address this idea today and highlight a significant weakness of the BTID philosophy because it doesn't get talked about nearly enough.

Things don't always go as planned

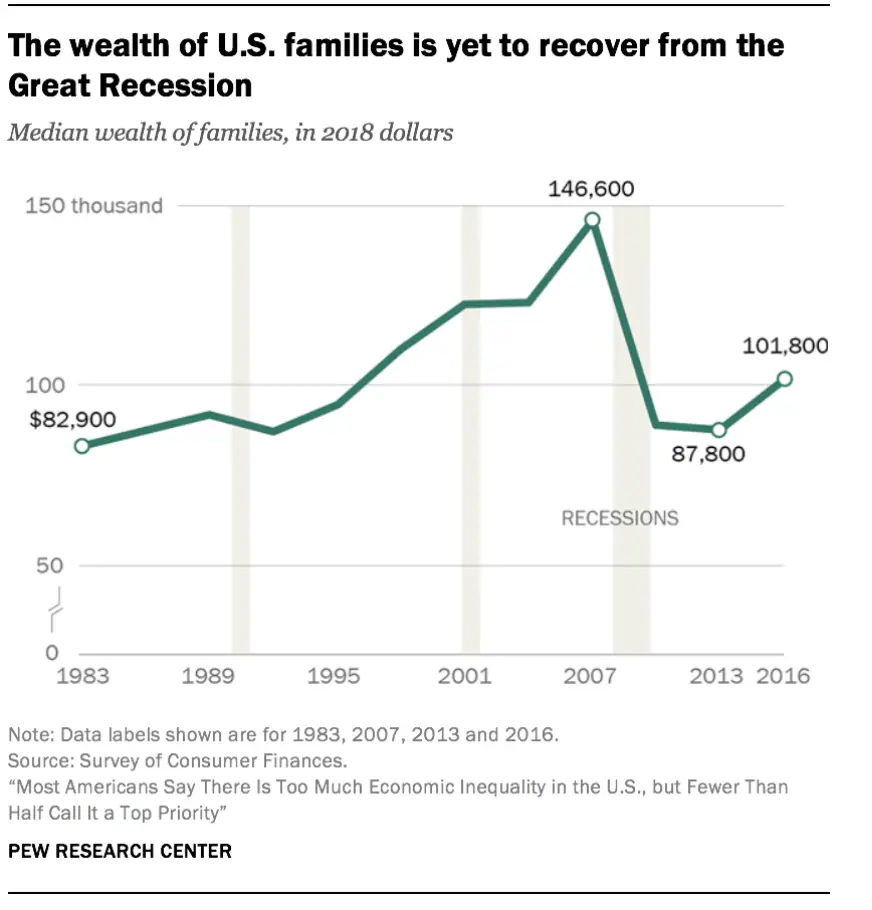

The idea that buying term life insurance instead of whole life or universal life insurance and investing the difference is certainly not novel. It's a philosophical chant that pre-dates my existence and many of the rest of you. So if it had decades to run, why do we hear that financial security among Americans is getting worse instead of better? Here's a graph from Pew that tracks the average wealth of Americans from 1983 to 2016:

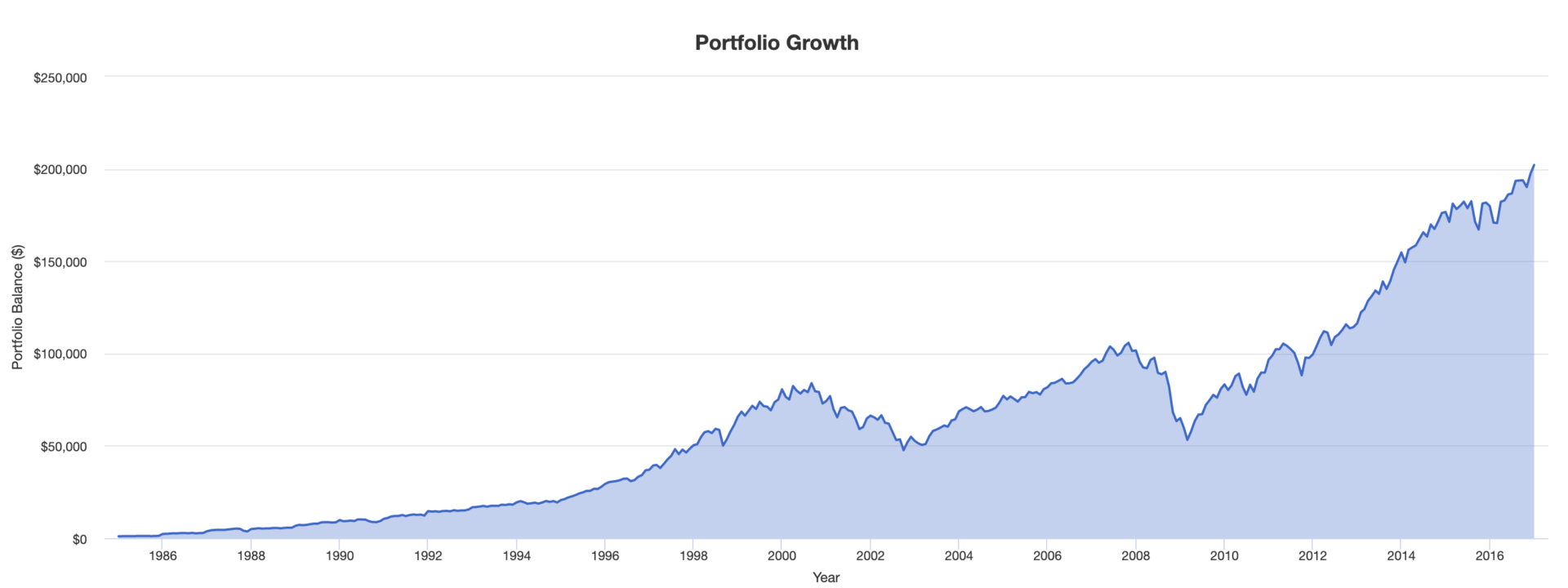

I'm not saying BTID won't work. What I am saying is that people either largely ignore it, or can't get it to work for them. If this weren't true, then the graph above should look similar to this one:

This is a graph of a $1,000 per year investment in the Vanguard S&P 500 Index Fund (VFINX) from 1985 to 2016–beginning in 1983 wasn't an option). The growth patterns is obviously different from the one we see showing average wealth among Americans according to Pew.

The problem with the idea of BTID and dropping the life insurance coverage at retirement is that it assumes “perfect world” scenarios…it makes no provision for your kid that needs to go to rehab when they’re 21 costing you $100k, the local health department official who decided your business is non-essential and shuts you down for 6 months, or the fact that most of your retirement savings are in a qualified plan leaving your heirs (non-spousal) not with the balance but with the balance minus the income taxes due.

It also doesn’t take into account that there might be some need for insurance after retirement. In my experience, even people who seemingly should have no NEED for life insurance often do need some amount of life insurance in retirement. And they’ve long since dropped their term coverage or outlived it. They’re now in their late 60s to early 70s. Now they’re faced with buying some small permanent coverage that’s quite expensive or hard to get because they now have a thick stack of medical records documenting their demise.

Reacting to the Need is Too Late

Costs associated with the life insurance if you wait and then decide you need it are substantial, particularly for those who have normal, middle-class level income. Here's an example Brantley used in a past blog post to illustrate this very point.

And do people really get to retirement age and then decide they need life insurance? Yup, they sure do. Here's a blog post from several years ago looking at third-party universal life insurance sales data. Key takeaways from that post are that people 65 and older make up a large percentage of UL buyers, and they make up an even larger percentage of premium payers–that's because it becomes increasingly more expensive as you age.

A serious weakness in the BTID strategy is that you won't know that you'll need life insurance in retirement until you actually reach retirement. The strategy leaves no contingency for planning ahead. It hopes that stocks and bonds will provide ample returns to capitalize you in such a way to “self-insure.” If this fails to happen, you'll be forced to spend a lot of money correcting this.

Alternatively, if some of your retirement planning funds go towards permanent life insurance you will theoretically lose some of that money in terms of accumulation you'd otherwise achieve by investing it. But…and here's the key…you can easily figure out exactly what the “loss” is at the outset–and it's not nearly as much as you might think.

If, on the other hand, you go the BTID route, and end up missing the mark, you have no idea what your losses will be from having to liquidate assets and buy life insurance at a time when it's significantly more expensive. The purpose of planning is to prepare yourself for unforeseen circumstances and protect your interests from their negative implications. BTID is more wing-and-a-prayer than it is a plan as it provides little to no guarantees–or even reasonably high likelihood–that it can shield you from the financial setbacks of less than perfect life unfolding.

All the numbers, spread sheets, and discussions miss one huge human behavior. How many people who go the BTID route actually invest the difference consistently? The semi- compulsory nature of permanent life insurance premiums make a great deal of difference. Think Christmas clubs. Another real world risk to BTID is the probability that an individual may become disabled as I did 26 years ago. I am now 70 years of age and the Company has waived the premiums for the past 26 years and will continue to do so until I am 90 years of age. The self completing nature of permanent life insurance can make all the difference. My portfolio at the Vanguard took a fair sized hit due to Evergrande, but my cash values went up, guaranteed.