When you retire, you have the option to continue paying for the life insurance you had while you were working or buying your own policy that is not connected to your employer at all. For most people, the type of group life insurance (offered at work) that costs almost nothing while working becomes very expensive to continue after you retire. Insurance companies have different policies to offer you that you should explore years before you punch the clock for your last day at work.

You should know about these things that can impact your life as a policyholder. It's always worth remembering that you really only get one shot at planning for your retirement. You should be able to enjoy your freedom once you stop working or managing your business. One way to do that is to maximize the benefits you can get from the life insurance you own during your retired years.

Life insurance, although not required, is one of the best and most stable assets you can use to store cash for and during your retirement. Aside from the fact that it provides security for your family when you are no longer around, you can also enjoy the benefits provided by its cash value while you are living.

Life insurance companies have become much more creative now and are creating policies that offer basic death benefit protection with the ability to provide competitive returns on your cash with unparalleled stability. You now have options more than just paying large premiums to insure your death benefit. If you are still hesitant and you want to learn more about why you might consider owning life insurance after you retire, here are a few things to consider.

How Long Should You Have Life Insurance?

Life insurance, as the name suggests, assures that you and your family are financially secure when you are not here anymore. The most popular life insurance policies sold today are term life insurance policies. You buy a term policy for a predetermined period, typically 10, 20, or 30 years. After the term period has elapsed, the policy stops. That may be a good thing for you when you are younger and have a really tight budget as most term insurance is pretty inexpensive.

But if you are retired, you are probably looking to have some sort of life insurance coverage that will be around until you die, not just for the next 10 or 20 years. So, what we have found to be the best option for most retired people is to look at permanent life insurance. There are really two main types of permanent policy–whole life insurance and universal life insurance.

If you want to read more about the three types of life insurance, read this article.

The key to buying permanent life insurance (let's talk specifically about participating whole life insurance) is to get it long before you retire. If you buy whole life insurance when you are younger, you will find that it is much more affordable and if the policy is designed correctly the death benefit will grow over time. This is why it is best to have one when you plan on retiring at the age of 65 or younger.

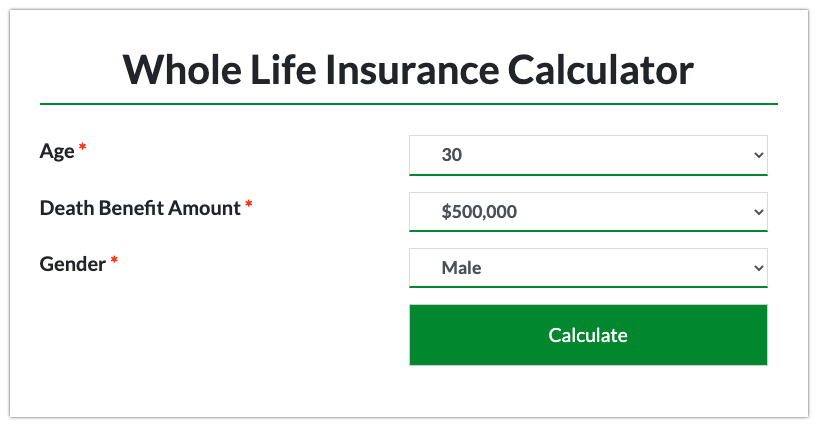

Starting a policy when you are young and starting one when you are old will change what you are able to afford. When you are young, you pay a lesser amount of premiums than when you are old for the exact same death benefit. Take a look at this example from our whole life insurance calculator…

Brad is 30 years old and he's married to Jenny. They just had their first child and that has Brad thinking about his life insurance. Right now, all he has is a death benefit that's 2x his annual salary at work which is about $160,000 in total death benefit. The policy costs him about $12/month. He thinks that he would like to add $500,000 in whole life insurance. When he gets to our calculator, this is what he enters:

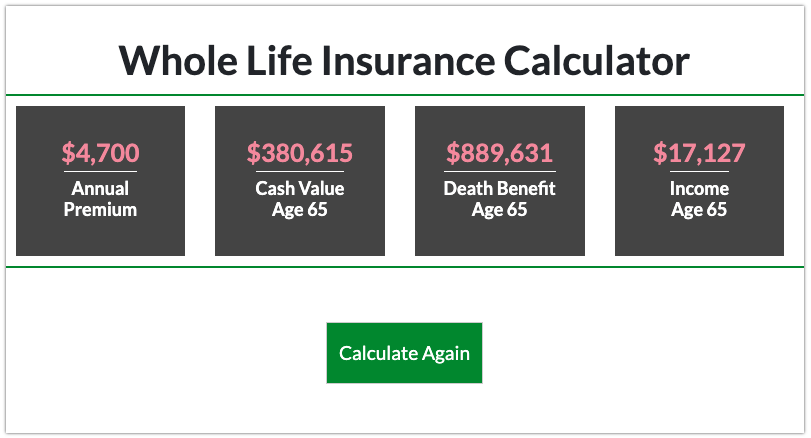

Here is an estimate of what Brad will pay he buys the policy now at 30 years old:

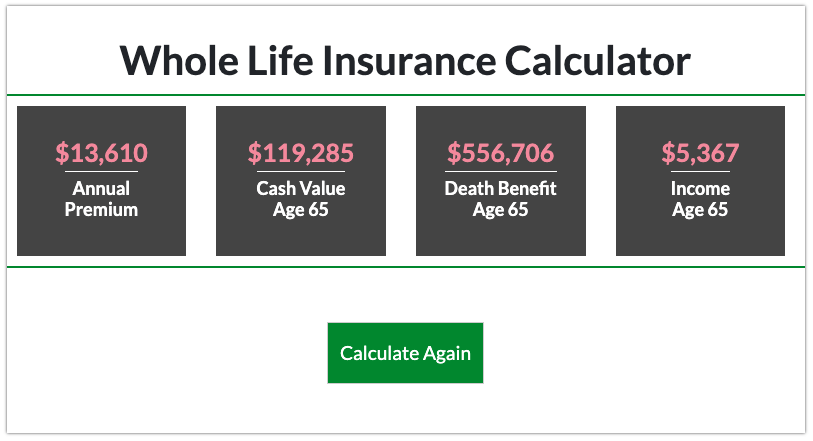

If, on the other hand, Brad decides to wait and instead looks to purchase the same whole life insurance policy when he's 55, this will be the result (approximately):

The cost of waiting here means that he will pay nearly 3x as much in annual premium for the same death benefit, he will have much less in cash value to add extra liquidity to his retirement, and his death benefit at 65 (retirement age) will be about $300k less than if he started his policy now at 30. Waiting is expensive and could be detrimental to your ability to afford life insurance in retirement.

Do I Need Coverage If I Have a Pension?

Another thing to consider is having insurance when you already have a pension. Some people consider their pension as their most important retirement benefit. While this is not a bad thing, pensions may not be enough to support you throughout your retirement.

What if you retire at 65 and live to be 95 years old? You still have to support yourself for 30 years if that's the case. Your pension may certainly provide a nice, stable income but it's probably not enough to afford everything you would like to have to enjoy your retired years. You still need an additional resource (more income) to help you create a solid retirement plan. Cash value life insurance can add that extra retirement income that allows you to enjoy yourself.

The good thing about having life insurance is that it serves as an additional source of money when you retire. You may have plans to travel, build a retirement house, or start a small business. The cash value accumulation in your whole life insurance or indexed universal life insurance is a ready source of available capital when you are ready to make your move. More often than not, pensions are only as good as a monthly allowance. You won't get enough from it if you still want to do other things once you retire.

Is Life Insurance Worth Getting If You're 65 Or Older?

It's better late than never. Whether you are 65 or older, it's still worth it to get your life insurance. As long as you can pay the premiums, life insurance is worth it. The best advice we can offer her to is to adjust your expectations a bit. You are not going to purchase a $500,000 whole life policy when you're 65 for $100/month.

But you may be able to buy a $20,000 whole life policy for $100/month when you're 65. Sure, it will not provide any additional benefits to you but it will ensure that there is money to take care of your funeral expenses and perhaps to settle some small debts that could help your spouse. Just make that you understand the terms and conditions of the policy you are buying and that you can comfortably afford the premiums going forward.

The Wrap Up

The best time to get life insurance is now, whether you are younger or older. As you age, underwriting challenges and policy costs make it tougher to find a policy that suits your budget. If you have the opportunity to buy a policy now that can provide a nice death benefit, decent cash value accumulation, and an affordable premium when you retire, do not wait. As long as you are around, you will continue to enjoy the benefits your policy provides during your years in retirement.