Podcast: Play in new window | Download

Whole life guaranteed cash value is an often overlooked and very powerful aspect of the use of whole life insurance as a wealth-building tool. The fact that a financial intermediary is willing to guarantee a value you can walk away from them with all the while promising to pay a substantially larger sum to your beneficiary should you die is both a difficult task to accomplish and an unheard-of benefit achieved with other financial tools.

When we talk about whole life insurance, we're mostly interested in the dividend. We care so much about dividends because they are a major driver behind the overall wealth-building potential afforded by whole life insurance. But, insurance is certainly an option often entertained when we contemplate what might go wrong as we wade through life. Truthfully, I can't name any other financial tools that offer guarantees anywhere close to what whole life has to offer especially given its non-guaranteed potential.

Attacking Whole Life Insurance Guaranteed Cash Value

Despite the strengths of whole life guaranteed cash value, many people attack the guaranteed ledger of a whole life insurance illustration because apparently, they know of somewhat you can supposedly do better. Do better is a highly subjective and relative notion, but one of the major arguments presented notes that with whole life insurance, you are guaranteed to lose money if you buy it.

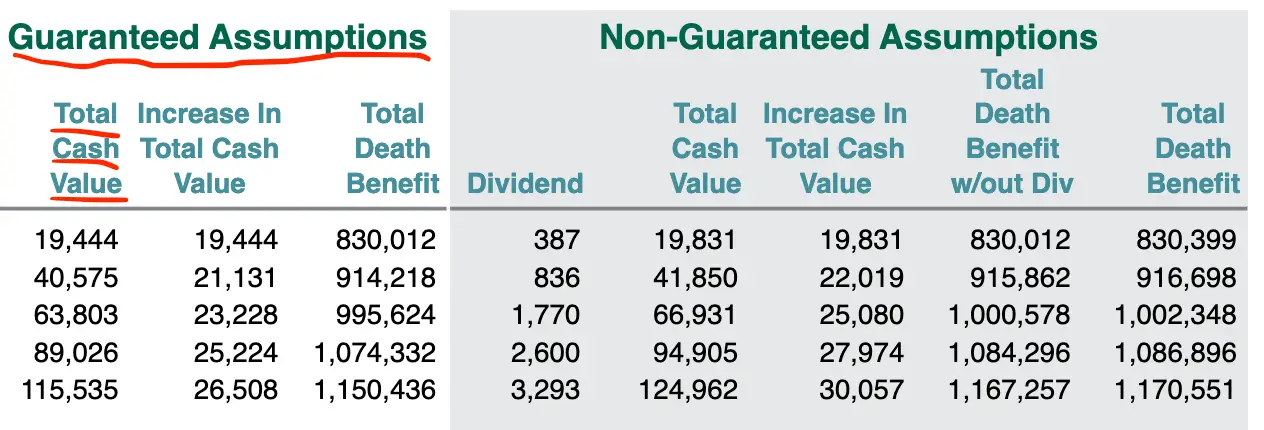

Seems like a reasonable claim. I mean the ledger does generally reflect some figure that is less than the premium you pay in the first year. It might look something like this:

In this case, the premium paid annually is $25,000. So you can plainly see that for this 40-year-old male, he is guaranteed to lose $5,556 (we simply subtract the guaranteed cash value from the annual premium). That's one way of looking at things.

But what if we thought about alternatives in the same context we present whole life insurance values?

The Guaranteed Ledger on your Other Investments

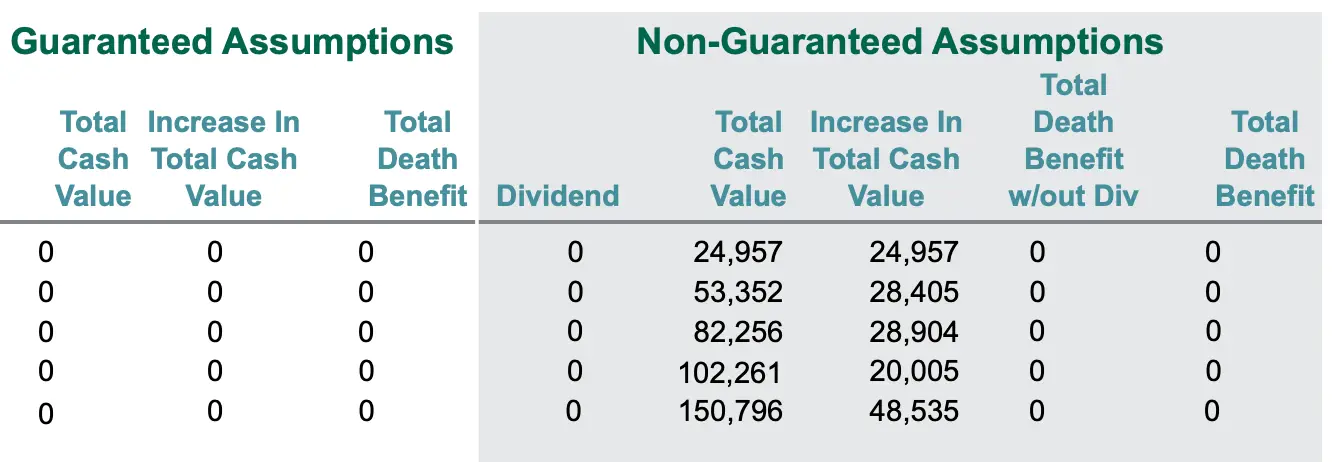

We express our displeasure for whole life's guaranteed loss from the outset, so what if we treated traditional investment options like we do whole life insurance? I took historical data from the iShares Corporate Bond ETF (LQD) and ran the last five years through a pro forma matching a whole life insurance illustration. Here's how that unfolds:

That's a lot of zeros. Turns out investing also guarantees a loss from the outset as well. And the guaranteed loss is significantly larger than the guaranteed loss on a whole life contract. There's also no death benefit provided to the investor, despite the significantly larger guaranteed loss.

Now some might object to the above scenario by noting just how unlikely it is for such an investment to go to zero. I agree. I note, however, that the likelihood of a whole life contract achieving only its guaranteed results are similar in likelihood.

The non-guaranteed accumulation values appear to pull ahead of the non-guaranteed projections from the whole life illustration. But notice that the increase in cash value year-over-year is certainly not linear. Now in truth, the growth of cash value in a real whole life policy that earns dividends will also sometimes fail to increase by an ever-growing number year-over-year.

If the dividend rate drops significantly, it's possible that the growth in cash value could drop below the prior year. Take special note here, I'm not saying the cash value will be less, I'm merely saying that the growth in cash value may be less than the year prior.

But, go back to the whole life illustration above and notice that the guaranteed accumulation of cash values also produces an ever-growing result year-over-year. This means that a very large reduction in the dividend could result in an absolute growth in cash value that is less than the prior year, but the guaranteed accumulation of cash value in a whole life policy will most likely make this difference extremely small. Let's also not forget that the guaranteed accumulation of cash value in a whole life policy does improve as non-guaranteed features unfold.

This makes the ever-increasing guaranteed amount of cash value increase each year improve vastly beyond what we see when we look at an illustration. It also means that guaranteed values will vastly improve as actual non-guaranteed elements unfold.

Had I truly followed the rules for whole life insurance, I would have instead used an average of the returns achieved by the ETF in the past five years and used that value to project values. Doing that would have resulted in projected cash values at year five of between $140,000 and $145,000. Still, though, I get no death benefit.

And these results change depending on what day or month I actually bought into the ETF. Whole life insurance, on the other hand, will deliver the same return regardless of the day or month of the year I buy it. I don't have to worry about fluctuating markets because of a bad earnings call, an international pandemic, or whatever major story rattles the bond or equities market.

Why Does he Keep Talking about the Death Benefit

I know there are some of you who will happen upon this blog post and say “who cares?” every time I mention the death benefit. Perhaps you belong to that group of people who thinks you'll achieve some sort of platinum saver status once you've “self-insured” against the risk of dying early–whatever that means exactly.

I bring up the death benefit part because it means something. A lot of people (me included at one time) discount the value of a death benefit. A lot of us think death is way off in the future and there's no way that sort of thing will happen to us. But death benefit does have serious value to it. It creates an immediate estate for those who have it.

I'm pretty happy to know that ignoring all future decisions I make about new life insurance purchases, I'll have at the very least a seven-figure death benefit in force solely because I choose to buy some whole life insurance in my 20's. For me, the focus was way more on the cash accumulation, and it's still the aspect that gets me more excited at the moment.

But if someone someday shows up and offers Brantley and me several million dollars for The Insurance Pro Blog and I find myself with a new pot-o-money that wasn't part of my original retirement plan, I'm certainly not going to cancel my life insurance.

The fact that I have that death benefit in force, the fact that I am guaranteed a certain level of cash value and cash accumulation forever and always and I get this death benefit with the option to keep it for as long as I want it makes for a good deal in my eyes.

Whole Life Insurance is Far More Comprehensive in its Reporting

Whole life insurance (or really any life insurance with cash value) is stunningly more comprehensive in its reporting of assumed and guaranteed components than any other financial vehicle of which I am aware of. This is both a blessing and a curse.

It's nice to see just how far life insurers go (sometimes it's voluntary and sometimes it's a regulatory requirement) to try and explain the many aspects of what could and what will happen if you buy life insurance.

At the same time, this comprehension can cause a lot of confusion and intentional misinterpretation by those who wish to sell you on an alternative idea. Some people assume that because other savings or investment options don't come with near as much detailed explanation, those options must not contend with the same number of obstacles as whole life insurance. That seems like a logical thought process, but it's sadly ill-conceived.

Truth is most if not all of those alternatives have just as many, if not more, stumbling points and asterisks to check. However, the norm for most investment plans is to ignore a lot of those obstacles and instead sum it up by mentioning that investments involve risk and results are not guaranteed. That statement is similar to the ledger I produced above, but I'll bet the zeros in the above ledger catch far more attention than a fine-print statement that says something to the effect of “results not guaranteed, investments involve risk of loss.”