Podcast: Play in new window | Download

Some say that whole life insurance only makes sense for the ultra-wealthy. Believe it or not, one of the top-ranked websites for personal finance makes this claim about whole life insurance, “…such policies usually only make sense for individuals with a net worth of at least $11.4 million” (estate tax exemption threshold).

Uhhh…not sure how they reached this conclusion and of course reading horrible misinformation about whole life insurance is not uncommon.

We’re using that quote as an example of what the internet views as being authoritative information about whole life insurance. By the way, the article where it was pulled from promises to discuss the same topic I’m writing about here.

However, I’m pretty sure if you read their article next to this one, you’d swear we’re not even talking about the same thing.

Why Would Anyone Want to Use Whole Life Insurance for Retirement?

If you’re asking this question, you’re one of those curious people that we welcome with open arms to this website. A major reason that we’ve kept after producing content here for over eight years (you read that right) is that we both tend to have contrary viewpoints.

It’s not that we’re disagreeable for the sake of it. Not at all in fact.

But we have a unique perspective to offer you having been trained by large mutual companies that specialize in selling participating whole life insurance. We’ve both been licensed to sell securities (stocks, bonds, mutual funds, etc.), had some experience in the wholesale distribution side of the financial services industry as well and one of us owned an RIA at one point as well.

Having done all of those things and experienced the sausage-making process of financial planning and retirement planning, we reached the semi-educated conclusion that whole life insurance can, in fact, be used for more than paying estate taxes. It also serves a purpose for people who aren’t “ultra-wealthy”. In fact, most of the people we help are far from ultra-wealthy. Most earn above-average incomes and are definitely way above average with their level of financial discipline.

With that experience, we’ve narrowed down three distinct ways that whole life insurance can be used in retirement. These are not the only uses for whole life in retirement.

But these are the three that can have a direct impact on retirement income which we have found to be the most popular discussions from our clients and potential clients.

We’re going to look at the following three ways that you can use whole life insurance for retirement:

- As an alternative to loading up qualified plans

- Income source rotation

- To Build an Income Stream That Lasts Forever (with guarantees)

But first, let’s explore how the whole life policy would even have the cash to provide for you in retirement.

How Would Whole Life Insurance Deliver For You in Retirement?

When you own a whole life insurance policy, the premiums you pay accumulate cash value. Not all of the premiums you pay go directly to the cash value, but a portion of the premium does.

The cash value of your whole life insurance policy can be taken out at any time and for any reason. You don't have to die in order to use the cash value in his or her life insurance policy. But in this context, we’re looking at how it can benefit you in retirement.

You can take cash values out of a life insurance policy in two different ways.

1. Withdraw cash from the policy

2. Take a loan against the policy

When you take a withdrawal from a whole life insurance policy it means that you are removing the cash from the policy. The option to take withdrawals is available for every whole life insurance policy I’ve ever seen. That being said, taking withdrawals is something that you need to explore first and make sure that you understand the implications of it as it is irreversible.

Why would that matter? Well, if you withdraw cash from your policy, typically you are surrendering paid-up additions. That means those paid-up additions will no longer earn dividends. It’s not a bad thing, just need to be sure you know that and understand how it will impact your policy going forward.

A loan does not mean you removed cash from the policy. Instead, the insurance company lends you money. You then pledge cash in your life insurance policy as collateral for the loan.

The method you choose to access cash in a policy depends on specific circumstances. These circumstances include personal matters about the policyholder as well as the specific life insurance contract.

You can check out our whole life insurance calculator to get a rough idea of how it could work for you.

Qualified Plan Alternative That Shields You From the Taxman

It seems like everywhere you turn in personal finance websites, publications and books, you’ll find advice that recommends you take full advantage of your 401k, IRA or whatever flavor of qualified plan you have the ability to fund. The rules of each are slightly different but the tax treatment for each is the same.

Defer current income, pay no income tax on the deferred amount, your money grows without tax and when you are around 60 you can take the money from your qualified plan without a penalty. Obviously, you’d pay taxes at that point. How much you pay will depend upon your other sources of income.

I’m not going to exaggerate and suggest that you’ll be paying a 62% effective tax rate when you retire. Though we have certainly seen some outrageous claims about tax rates.

We take a contrary position here. Not that we like paying taxes nor do we suggest that your patriotism is tied to paying taxes.

But today, we’re suggesting there could be another consideration than just the tax argument, though we will touch on that one below as well.

Lemme share a short story with you…

A couple of years back, I was at a meeting with other financial professionals. Before the start of the main event, I was walking around meeting people that I hadn’t met before.

During that time, I had the privilege of meeting a guy who claimed he’d been listening to our podcast for years and reading our blog. I’m always flattered and forever stunned. Weird to think that people you’ve never met spend the time to listen to what you have to say. It’ humbling.

But I digress…

As we were talking, we were lamenting how tough it can be at times to get people to pay attention to the message we’re trying to convey. Long story short, he began telling me about his father.

A guy who’d been around the life insurance industry for decades and is now semi-retired as I understood it. What the younger son was conveying to me is the conviction he had in funding life insurance as opposed to loading up his own qualified plan (though he had a 401k available).

[Quick sidebar here from me…I’m not suggesting that all qualified plans are bad and that no one should ever use them. People have different reasons and different circumstances. The details do matter.]

His Dad created a six-figure retirement income exclusively using the cash value from various policies that he had. I’m not sure of the companies, products, etc. It doesn’t really matter.

The point of the story that the young man shared with me was that he had recently looked at his father’s tax return and verified that “on paper” he had no reportable income from investments, pensions, etc. His only source of reportable income for income tax purposes was social security.

He paid no taxes at all because the rest of his income is derived from life insurance policies that he funded over his working years. Income from a life insurance policy (particularly if it’s all in the form of policy loans) does not apply toward provisional income calculations either, so none of his social security is taxed either.

Is this the right solution for everyone? Probably not but it is interesting to look at those cases out on the edge to see what’s possible.

Use Whole Life to Diversify Your Retirement Income Sources

You may have heard someone mention or read somewhere else online that you should plan to withdraw no more than 4% of your assets in retirement? This is what’s commonly referred to as the 4% rule.

There’s a lot of common financial wisdom floating around out there and one of the favorites relates to the 4% rule. People will suggest that if you just follow the 4% rule everything will work out fine.

After all, average market index returns have far exceeded that and despite the up and down, if you keep withdrawals to no more than 4% you’ll be fine.

The idea is that it will ensure you against running out of money over time as you take the money that you need to live from your total pool of liquidity in retirement. It was conceived by William Bengen back in 1994 and further analyzed by three professors at Trinity University in what has become known as the “Trinity Study”.

This has led a lot of financial professionals to recommend a plan where individuals liquidate no more than 4% of total assets in any given year to cover retirement expenses. And there’s a lot of hypothetical data to support it, just google it, you’ll not run out of reading any time soon.

Maybe it will work out for some people but our suspicion is that it’s way oversimplified and really doesn’t account for at least two separate risks (though there are others):

1. That there could be a significant drawdown in your investment account(s) during the early years of your retirement income phase of life.

2. That you will ignore all external information and blindly follow a rule of thumb come hell or high water.

Why not be a bit more selective in how you choose to take income and perhaps consider using whole life insurance as a core component of your retirement income plan?

Here’s an idea, just like most people aren’t going to put all their eggs in the whole life insurance basket, maybe consider not putting all your eggs in the “I’m gonna withdraw 4% of my investment account value” basket.

What if you treated your whole life insurance policy as another asset pool that you could use as a source of income?

And instead of taking 4% every year from your investment accounts no matter how poorly the market performs, you alternate what source of money is used to withdraw the money you need to live.

What I’m sharing is also an oversimplification but the idea is valid. The particulars are dependent on each person’s unique situation.

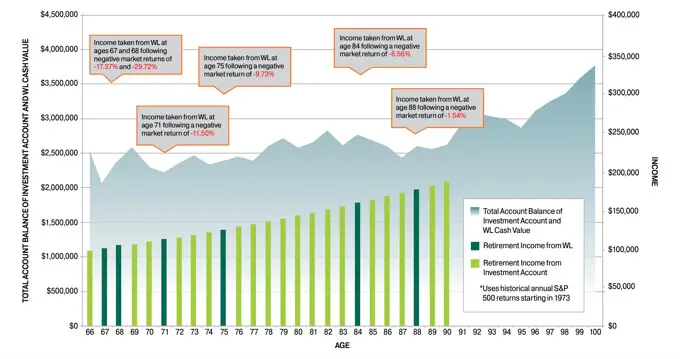

Consider this…what if you alternated. You save and invest in your retirement plans, investment accounts, stock purchase plan and you also fund a whole life policy.

When you retire, you take your income from investment accounts following the year when they are up and you take your income from the whole life policy the year following a market drawdown. Obviously, you could mix and match here, I’m just floating an idea.

Here’s an example that overlays historical market returns starting in 1973:

Remember, life insurance companies tend to invest their reserves conservatively. Part of that is just the nature of the life insurance business and the other part is the regulations that govern how they’re allowed to do invest their reserves.

Yes, dividend rates can and have decreased in the last decade. But I was just looking at a big mutual company’s complete dividend history yesterday and current dividend rates are not an anomaly. They’ve been low before and the policies thrived in spite of it.

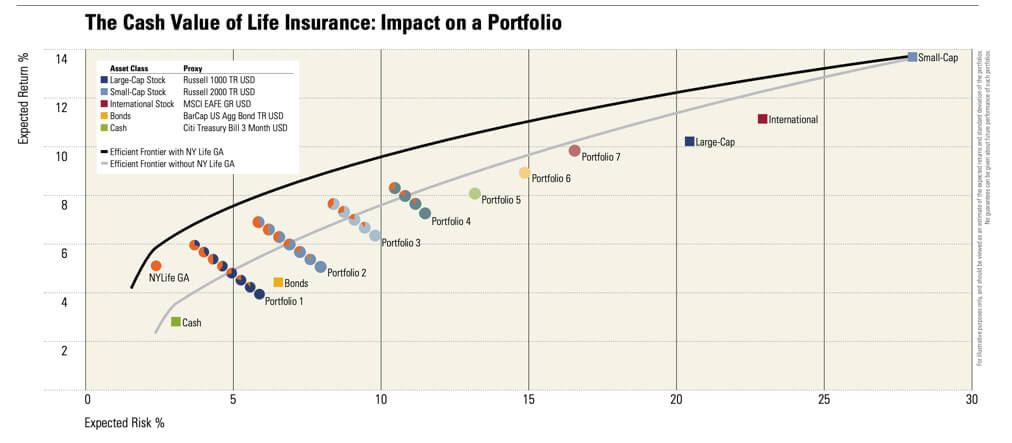

Life insurance is an inherently profitable business and your policy dividends benefit from that in addition to the insurance company’s ability to create decent investment returns in their general account over time. Whole life insurance is truly non-correlated and creates a more efficient portfolio mix when viewed in the context of being another asset, rather than a “have to” expense.

I wish I had a more up-to-date graphic to share but this is still relevant. Look at how whole life insurance adds to overall portfolio efficiency:

Buy an Annuity That Provides Income Security

Using your whole life insurance policy to purchase an income annuity is an old idea that no one really talks about anymore. Well, no one really talks much about income annuities at all, they’re not sexy and the returns are not that great in our current environment of super-low interest rates.

That’s a shame really. Income annuities are among a small handful of ways that a person can absolutely guarantee a stream of income that will last until you die.

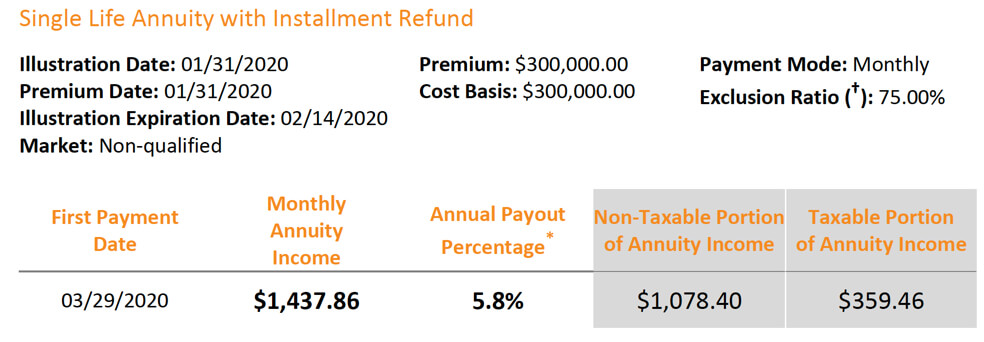

I ran a quote assuming that a 65-year-old male uses a 1035 exchange to move 300k from his whole life insurance policy to a single premium immediate annuity. Based on a single-life payout with an installment refund (if he hasn't received all of his principal when he dies, his beneficiary will continue to receive the annuity payments until all the money has come back).

Here's the outcome:

Now, many people will look at that and think that they can do better than that. They don't wanna give up control of their money in exchange for a guaranteed income stream.

Others will claim that the monthly annuity income is too low, they need more income. We get it, but maybe you could shift your perspective a bit and realize that these numbers are realistic. If you need more income, you need to grow the total size of your income-generating asset pool.

Whole life insurance works in retirement and for more reasons than the three I've listed and described here. If you'd like to see how it can work for you, reach out and let's talk about it.

I see a lot of NW Mutual policies with an 8% loan charge rate. So I would not use loans on these policies unless they will be paid back quickly. For the long term, you typically would be better off using withdrawals even if you get to the point of paying taxes on gains, rather than pay the high loan charge rate. what rules of thumb would you use to look at loan charge rate, dividend credit rate and base cash value credit rate?

There is so much variability that we don’t general use rules of thumb regarding this. You are correct that Northwestern’s loan rate can be punitively high. Though they do adjust the dividend upward to partially offset this.

Hello Brandon and Brantley

Thanks for putting in a good word on behalf of immediate annuities. You guys are the source of truth in a financial world full of lies and misunderstandings.

I commend you for including the illustration that shows the total benefit and the taxable portion of the benefit. Very few discussions of annuities make the point that if the consideration consists of after tax money, then the IRS recognizes that the annuitant has the right to recover his basis during his expected lifetime. This is done thru the calculation of the exclusion ratio which determine what portion of the total benefit is subject to federal income tax (until the entire basis has been recovered). This exclusion of basis from income taxation is a strong selling point for annuities, I don’t know why it is not mentioned more frequently. Also the exclusion of basis from income taxation refutes a criticism of annuities from uninformed ‘experts’ who claim that annuities are a bad deal because you end up paying income taxes on the consideration you paid. Wrong ! I heard this charge just recently from a financial ‘expert’ on the radio..

Whole life insurance is the worst product that anyone can buy. It literally says insurance at the end and that’s what it should be used as. It’s not an investment strategy. Annuities are horrible. You guys need to learn that selling whole life insurance is pathetic. You’re taking people’s money and slowing down their wealth building process by taking their money and putting it in your pockets.

Hi Chris,

Thanks for setting us straight. You forgot to teach us what magical “wealth building process” recommendation suits your fancy.

?????? Chris Fox, you’re SO RIGHT. You should write for Investopedia! Luckily you’re here to protect me from insurance and annuity commissions and these salesmen. Clearly this blog is run by greedy salesmen only interested in base premium commissions. Commissions are bad. Salesmen are bad. Commerce is bad. Efficient choices are bad. I prefer to pay for fees every year for limited investment strategies based on good old fashioned investing advice. Investing always works – just google it. After all, I don’t care what something does, what it provides, how much it reduces my taxes, or how efficient something is – I won’t do it if it involves a commission and has the bad words insurance and annuity. So I’m with you Chris – tell these fools how to do it the right way!

Know it alls are people that stopped learning.

Said like a true multi level term plus American Funds Salesman. ???

Can you demonstrate the science behind your claim as Theinsuranceproblog.com does?

A strategy to make the annuities far more viable and effective is to wait to do the exchange. Use your whole life for as long as you can until you see the need for the additional income – the annuity will consume itself while sticking with whole life for as long as you can will allow it to keep growing, all else equal

A very long time ago, I would also have been one of these trolls. I have, since reading your blogs and multiple educative articles, come to realise that it is not fair to characterise Whole Life Insurance as a pure Insurance product. After seeing many of your illustrations, and conferring with my advisor, I have seen ways to actually make this an investment strategy, with insurance as a mere nomenclature. I thank you for constantly endeavoring to educate sheeple – and hope that the industry is able to clarify the investment capabilities so that it is not vilified by all and sundry.

Not saying the following to brag, just to show that I have some experience and education when it comes to life insurance and annuities. I am a licensed life insurance agent, I just passed the CFP® examination, and I also have a master’s in finance. With regards to the hearsay you mentioned about some guy’s dad that funded his retirement with policy loans, I have a few things to add:

1) I’m guessing this gentleman’s father started these policies in the 70’s, 80’s, or 90’s, at the very latest? You mentioned you do not know the details, but I think this is a safe assumption. This was a time when interest rates were much higher than they are today. Thus, they would have accumulated a lot more cash value tax-deferred. Investors and policyholders today do not have this luxury. Additionally, the dividend payouts are not quite as high as they used to be because insurance companies are not able to earn as much interest on their general accounts. Like you said, they are limited to investing in conservative investments, mostly because the money needs to be ready at a moment’s notice to pay off claims. Mind you, he could have established variable or indexed policies or a combination, but those are going to come with market risk in exchange for higher potential returns. This also does not count all the other fees that the company charges for investment management, mortality expenses, and sales & administrative expenses.

2) The policy loans he took out certainly would not count as taxable income, as you said. This is not a bad option if the policyholder does not care about paying the loan interest each year and does not intend to leave much of a death benefit (if any) for his loved ones. Most insurance companies give policyholders a window every year (usually 45 to 60 days) to pay off the interest all at once so that it doesn’t compound. If you do not pay off the interest each year, then it gets added to your loan balance. This new figure is then multiplied by the loan interest rate when the interest bill is due the following year. When the insured dies, the loan balance is subtracted from the death benefit payout. The net amount is passed on to the beneficiaries designated by the policyholder.

Even if he does not care about leaving a death benefit, having to pay all that interest each year detracts from its viability as a good retirement investment, no? If he doesn’t pay the interest, then the loan balance increases. Most insurance companies have a limit on how high your loan balance can be (usually 90% of cash surrender value). Once your loan balance exceeds that, the policy either is cancelled or the owner has to make payments on the loan. In essence, his retirement fund disappears if the loan balance exceeds that level if he’s still living. If he has multiple policies, he might not care if one or two run out of cash reserves each year.

———

As for me, I sell term life insurance, simplified whole life insurance, and basic universal life (not indexed or tied to the market in any way) options A and B. I run across very few cases where universal life insurance, let alone whole life insurance, is a good option. The only times I push whole life insurance are the following:

1) The individual wants to make sure they still have coverage active after their term policy is up for renewal (i.e. at the end of its term). By setting up whole life insurance at the same time as your term policy (ideally when you are relatively young and healthy), you’ll pay lower fixed costs. A bonus is that you have more time for the cash value to build up. Once the term is up, you do not have to sign up for new coverage at potentially higher rates because of your health and/or age.

Note here that the cash value component is a bonus. It is not the primary selling point I make. If you want to invest and you are young, there are better options out there.

2) The client wants to provide income tax-free funds to pay for funeral expenses. Whole life is great for this objective because you cannot outlive the policy so long as you keep making payments.

3) The client is a partner in a business and wants to make sure his/her partners can buy out his/her share at a favorable rate pursuant to a buy-sell agreement if the client passes away. (Talk to your tax advisor and estate attorney for further guidance.)

4) To pay estate taxes if the client anticipates leaving an estate greater than $11.58MM (2020). Neither term life nor even universal life does the job because the client might outlive those policies. Plus, the pay-out is income tax-free, though there might be estate taxes involved.

Hi Paul,

The timing of the purchase is mostly irrelevant. If this individual did buy a policy during any of these decades you mentioned, he would have missed out on the dividend payment you suggest because he would have had a policy with far too little cash in it to benefit much from the higher dividend rate. Best case scenario would be a policy purchase in the early 70’s, which would have benefitted the most from the run-up in interest rates throughout the late 70’s through 80’s timeframe. But he’d still have a declining dividend rate such as the ones seen today affecting cash value now.

In addition, the logical conclusion of your statement is that because interest rates are different now, whole life is no longer a good deal. We don’t know what interest will be throughout our lifetimes. If something forces interest rates up five years from now, I’ll be much happier than if interest rates were to spike right now and then fall because I’ll have more cash value accumulated in my whole life policy five years from no and will therefore be in line for a much higher dividend then.

Balancing assets against liabilities through debt accumulation is a finance trick far older than modern-day whole life insurance (or any of the other forms of life insurance). The indebtedness that accumulates against whole life insurance is not a problem if that’s the plan someone has for the policy. I suppose you intended your comment to mean that it’s not a good after-thought. In other words, one probably shouldn’t just think “I can do that,” because he/she owns an old whole life policy. There are circumstances where I’d be inclined to agree.

Most companies will allow much more than 90% loan to cash value before a problem occurs, but even with that in mind, we have to be honest about how easy it is to accumulate such a loan balance. Sure there are anecdotes about someone who used premium loans, for example, then after several decades discovered the loan balance was nearly equal to the cash value. Operator error is operator error.

Your lack of being in/finding situations where whole life insurance or universal life insurance is a good option says more about the people you work with than it does about whole life or universal life insurance. I mean no negative sentiment with that statement. There are lots of people who shouldn’t buy whole life or universal life insurance.

Universal life insurance can be a perfectly fine option to address estate taxes.

“There are lots of people who shouldn’t buy whole life or universal life insurance.” Can you demonstrate the science to back up your claim? Shouldn’t be hard. ?

I’m retired receiving a set amount each month .from my pension plan do union have the have plan that retirees use during retirement years …

Hi, I don’t understand your question.

Thank you for sharing useful information about whole life insurance for retirement. You have provided such a wonderful article with all the important information.