Podcast: Play in new window | Download

Over the last few years…basically since the beginning of the Insurance Pro Blog going back to the summer of 2011, we've been preaching the gospel of whole life insurance.

Sure, there have been plenty of people who've come along to tell us how wrong we are and how a simple investment in an index fund could certainly outperform the return on the cash value of a whole life insurance policy.

To this, we've never disagreed. Yes, in fact, we too believe that a long term investment in stocks or equity funds of any kind should…outperform the return on cash in a whole life policy. But that's kind of like us all agreeing we'd live a much longer and healthier life if we only ate raw vegetables and less prime rib smothered in butter.

Data is one thing, human behavior is another altogether.

I should preface this introduction to episode 004 by saying that if you've not read these two posts, you should, it will give you a great frame of reference for the discussion in the episode and there are numbers discussed that you can see in the post(s):

- Historical Proof That Blended Whole Life Really Works

- Blended Whole Life Insurance vs. the Stock Market

Our point is that while average annual returns for various index funds and the indices themselves look great, most people aren't able to achieve returns anywhere close to those numbers.

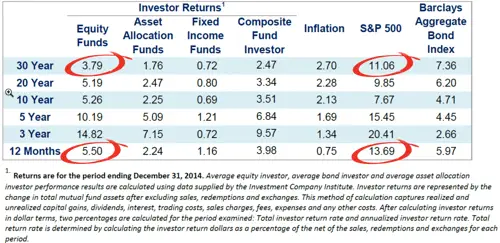

Here are some numbers from DALBAR's annual “Quantitative Analysis of Investor Behavior” based on end-of-year 2014 returns.

Here's a more detailed rundown of the DALBAR report:

- In 2014, the average equity mutual fund investor underperformed the S&P 500 by a wide margin of 8.19%. The broader market return was more than double the average equity mutual fund investor’s return. (13.69% vs. 5.50%).

- In 2014, the average fixed income mutual fund investor underperformed the Barclays Aggregate Bond Index by a margin of 4.81%. The broader bond market returned over five times that of the average fixed income mutual fund investor.(5.97% vs. 1.16%).

- Retention rates are

- slightly higher than the previous year for equity funds and

- increased by almost 6-months for fixed income funds after dropping by almost a year in 2013.

- Asset allocation fund retention rates also increased to 4.78 years, reaching their highest mark since plummeting to 3.86 years in 2008. Asset allocation funds continue to be held longer than equity funds (4.19 years) or fixed income funds (2.94 years).

- In 2014, the 20-year annualized S&P return was 9.85% while the 20-year annualized return for the average equity mutual fund investor was only 5.19%, a gap of 4.66%.

- In 8 out of 12 months, investors guessed right about the market direction the following month.Despite “guessing right” 67% of the time in 2014, the average mutual fund investor was not able to come close to beating the market based on the actual volume of buying and selling at the right times.

Just further proof that behavior rarely aligns with reality.

Psychology and emotion play a very large part in your long term financial success. It's better to build a plan to “control the control-ables”. It's not sexy, it involves more planning and probably requires you to save more money because you're accepting a plan based on lower average returns.

But in the end, if you plan conservatively, and end up with more money, you'll be happier than if you over-project higher than average returns and miss your target thereby not having enough money. I've yet to have anyone complain that they had too much money.

You can't buy groceries with average annual returns. And averages also mean that half the people get less than average returns. How do you know you'll be average or better?

If we've done our job effectively and you feel like this is a concept that you'd like to explore for yourself, feel free to reach out to us, by contacting us here.