This weeks edition of senseless arguments levied against whole life insurance and universal life insurance is one my very favorites.

Even though I’ve addressed this topic before, I couldn’t pass it up knowing I’d be writing a series on the most common “complaints” used to dissuade the buying public from these products.

I do have to admit right out of the gate, though, that this one has a shred of truth behind it.

You can’t take it with you

The old argument goes something like this:

“When you buy permanent life insurance, the cash that accumulates inside your policy is not paid to your beneficiaries when you die. Instead the life insurer keeps the cash and pays you the death benefit.”

Oh the horror…

I’m here to confirm this statement. It’s true. Functionally speaking, no life insurer pays the cash value out of a life insurance policy to a named beneficiary. The cash stays with the insurer; the beneficiary gets the death benefit.

But if this disheartening news makes you want to take up arms against the insurance industry, slow your role just a smidge because I have some additional information that could potentially change your views entirely on this.

It doesn’t Work Quite the way You are Thinking

This argument takes a technically true but functionally speaking obsolete piece of information a bit too far. Really far in fact.

Just because the life insurer is keeping your money doesn't mean they're robbing you or your beneficiaries of untold millions. An example will help explain.

Let’s go back to last week’s ledger we used to point out that positive returns really don’t take all that long to materialize. Here it is again.

For what it’s worth this is a whole life insurance ledger.

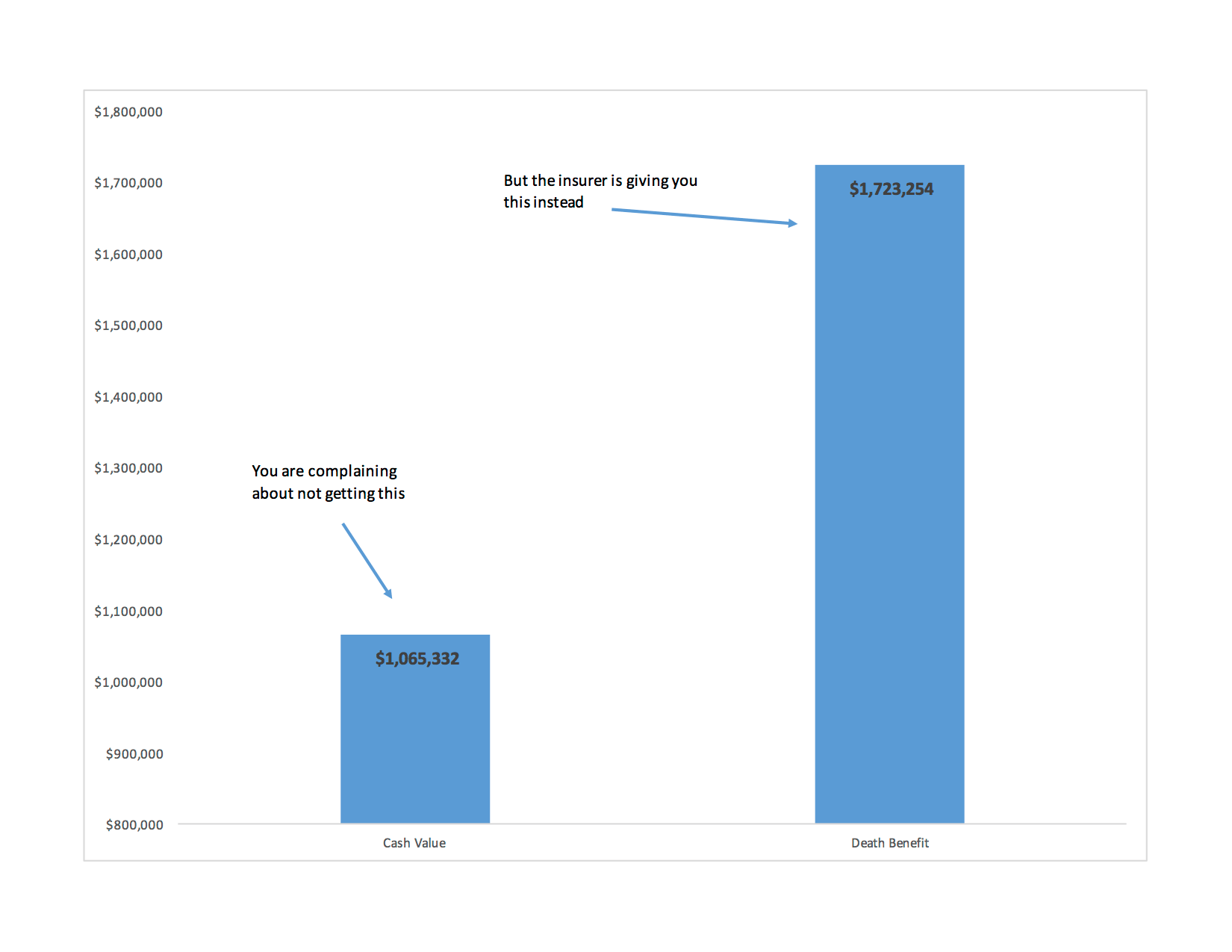

Notice that the initial death benefit in year one is $1,149,725 and the cash value is $40,424. Notice also that in year two the death benefit is $1,270,374 and the cash value $86,384. That means the death benefit increased in just one year by $120,649 and the cash value increased by $45,960.

I don’t know about you, but I’ll gladly give up ~$46,000 if I receive $121,000 in exchange.

Now let’s skip to year 15 where the death benefit is now $1,723,254 higher than it was at the start while the cash value is $1,065,332 higher than it was at the start. Allow me to put that in graphical form for you:

So wait a minute. Why is this happening?

Permanent Life Insurance Policies can have Increasing Death Benefits

I need to be clear in pointing out that not all permanent life insurance policies do have increasing death benefits, but most can be set up this way.

This applies to both whole life insurance and universal life insurance.

The so-called “taking of your cash value” keeps the death benefit completely tax free—assuming there isn’t an estate taxable circumstance, Goodman Triangle issue, or employee benefit rule violation that creates a taxable death benefit.

The life insurance industry is not trying to extract every last dollar out of you and keep it as their own. In fact, from this example, the annualized rate of return in year fifteen given the planned premium and the death benefit is 15.54%. I personally find that offering quite generous especially given the risk involved (or lack thereof).

Yes, life insurers keep your cash and pay your beneficiary the death benefit. But so what? You end up with way more benefit as a result.

This is all true but another piece of this is that even for level DB policies, the ins company isn’t really “keeping your cash” and paying the DB. While you are still alive, the “charge” for each year’s mortality coverage is based on the net amount at risk which is the DB less the CV. So, although the details of it all are very technical, you are really only paying for the amount the ins company will need to pay your from their own pockets (i.e. not your CV).

Another way of looking at it is that you could theoretically treat your CV as your own bank account and then pay for a one year term each year for the coverage amount that would equal the desired total DB when summing this term face amount and your bank account for that year, resetting this every year. In this example, when you die, your beneficiary is then left with your bank account amount and the ins coverage purchased, which would be the same as the ins company would pay in the full perm example.

Hi Dave,

Technically correct regarding pricing functionality, but this argument against whole life insurance cares more about what’s viewed as lost rather than what is gained. My point is simply that the suggestion of loss is largely fiction/misunderstanding.

You are absolutely correct that there is a pricing offset for the reduction in true death benefit (the net amount at risk) in the case of a level death benefit. And it’s certainly not the case that one should shun a level death benefit design in all cases.

Net Death Benefit = Net Amount At Risk + Cash Values – Any Outstanding Loans.

The cash values ARE paid out in the event of death.

Effectively yes, but technically no. There’s specific reason for this. Similar to dividends being a “refund” of premium.