There’s no doubt a number of people have made arguments against the ownership of cash value life insurance. You don't have to spend a lot much time surfing ye olde' interwebs to find such evidence.

There’s no doubt a number of people have made arguments against the ownership of cash value life insurance. You don't have to spend a lot much time surfing ye olde' interwebs to find such evidence.

Too many of these arguments are propped up on misinterpretations of the various products that exist–heck even the agents themselves can’t come to a consensus on how things work.

But one of my favorite literal interpretations about cash value life insurance that's used to substantiate the opposition is the fact that life insurance companies keep the cash in your life insurance policy when you die. “You don’t get the cash when you die, the insurance company keeps it!”

They exclaim with sharp disapproval. And most of you who don’t know any better fall for it.

Actually, they are Correct

Huh?

You mean the insurance company really is screwing me on the cash value thingy?

Yup, well maybe. Remember that analogy I made some months ago about cardboard boxes and creativity? If you’re new here check this out.

It’s completely true that when you die, the cash in your life insurance policy stays put with the insurer and they pay the benefit. Get over it.

This Hardly seems like a GOOD way to argue in FAVOR of Cash Value Life Insurance

Whining about the fact that life insurers keep your cash value is kind of like the complaining I did a few weeks ago when I said I wasn’t going to buy an engine air filter from E-europarts (a great resource for European car parts by the way) because the filter they had on serious discount for only $5 was still going include an $8 shipping charge.

My next cheapest option was Amazon, where it sold for $25 with free shipping! I’ll wait while you all do the math to figure out just how silly I was being…

Believe it or not, people make really dumb decisions and opt for the Amazon method everyday because they get tripped up in semantics. To be clear, I have nothing against Amazon, I spend lots of money there, too.

My point is simple. Like a lot of things, life insurance—and specifically cash value life insurance—is greater than the sum of its parts. It’s foolish to focus in on one part and declare something good or bad based solely on that one part.

It’s like saying I’d buy that engine air filter from that one place and save $12 vs. Amazon if only they didn’t charge me to ship it. When you really stop to think about it the answer is obvious, but we could spin it other ways to make the truth more obscure.

That’s Nice, but we like Proof

Alright, so I'm sure that you'd like to see evidence to back up this whole notion that “the product is worth more than the sum of its parts”…right?

Let’s do that.

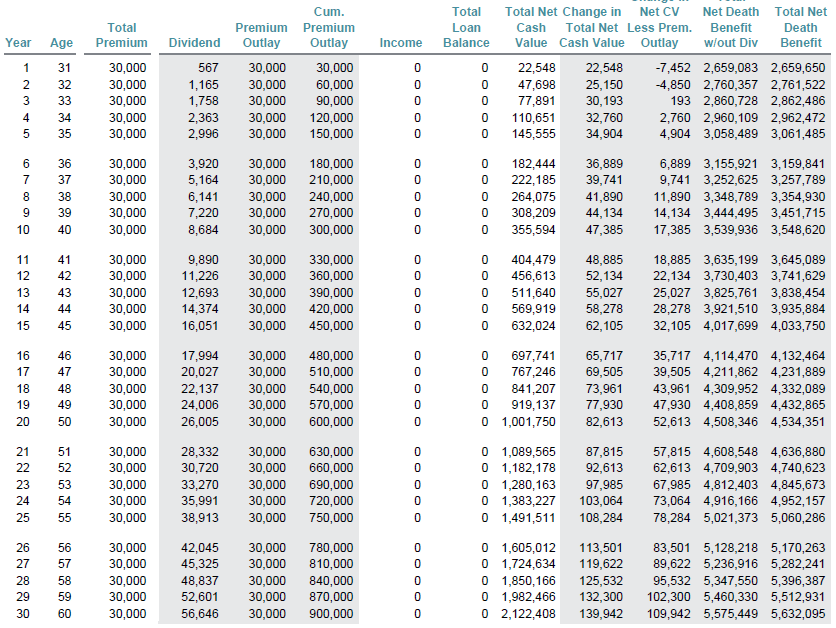

Here’s a blended policy designed to optimize cash and remain compliant with modified endowment contract restrictions. We have a hypothetical 30 year old who is placing $30,000 into the policy each year. This individual will then take income from the policy from age 66 to age 80.

[title color=”navy-vibrant” align=”scmgccenter” font=”arial” style=”normal” size=”scmgc-1em”]Click Image to Enlarge[/title]

So we start with a $2.7 million death benefit and come age 60 that death benefit has increased to $5.6 million. To get there, our premium hasn’t changed at all. For those interested in the math, that’s an 8.04% return on death benefit.

But much more noteworthy (at least to our topic at hand) is the fact that the difference between the cash value and the death benefit is $3.5 million. So even after the insurance company “steals” our cash value we’ll have increased the death benefit by $800,000.

But why stop there? Let’s take a look at our income scenario.

[title color=”navy-vibrant” align=”scmgccenter” font=”arial” style=”normal” size=”scmgc-1em”]Click Image to Enlarge[/title]

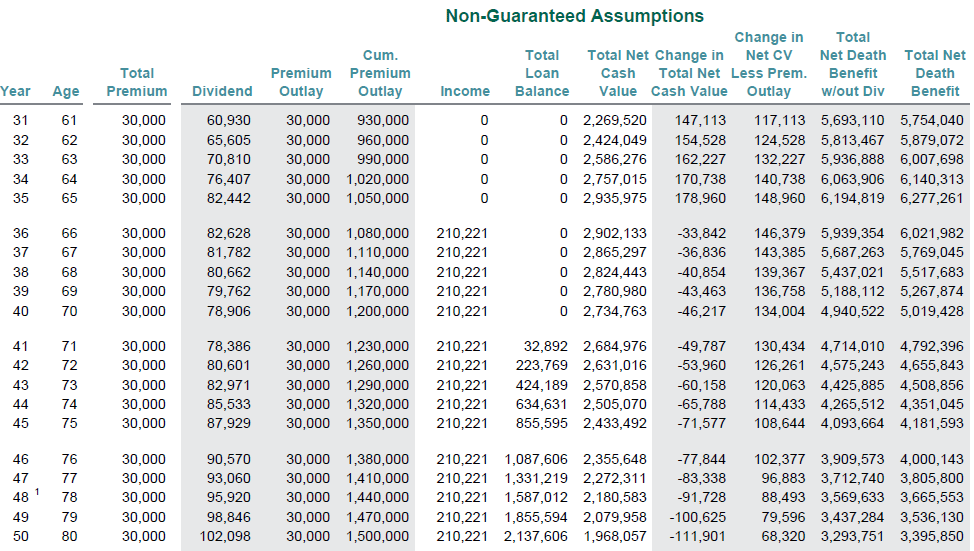

The policy projects income of some $210,000 per year.

That’s almost $3.2 million over the 15 year period. And at age 80 we have a death benefit of just a hair under $3.4 million. Let’s do the math on that, we’d need an equivalent investment account that yields a consistent 6.03% each and every single year in order to rival this plan.

That’s one hell of a yield in today’s market for a low risk asset.

But I’m not done just yet. The above example used whole life insurance, and we believe in equal opportunity at the Insurance Pro Blog. What happens if we run this same scenario with indexed universal life insurance?

Take 2 Indexed Universal Life Insurance’s Turn

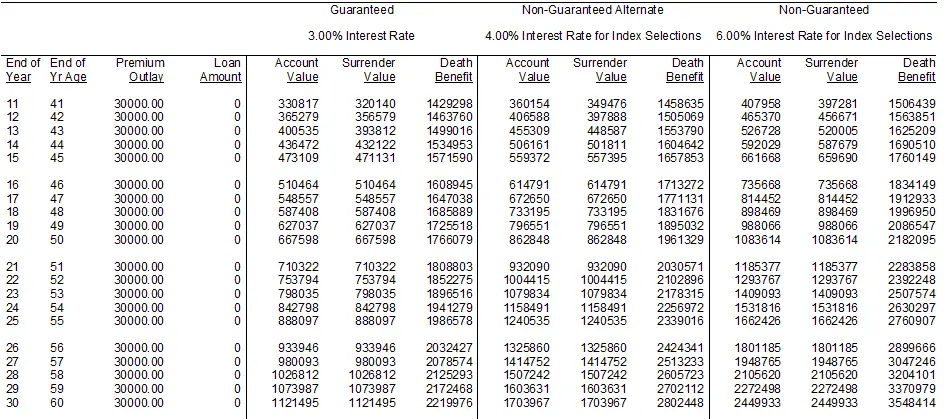

Same scenario, 30 year old male, $30,000 per year stops at age 65 income from 66 to 80. There’s no blending with universal life insurance, but we design the policy to use the guideline premium test, and we drop the death benefit to minimum allowed death benefit under the DEFRA guidelines.

As per our usual illustration guidelines, the assumed crediting interest rate is 6% in all years.

Here’s what we get:

[title color=”navy-vibrant” align=”scmgccenter” font=”arial” style=”normal” size=”scmgc-1em”]Click Image to Enlarge[/title]

We start with a death benefit of $1.5 million, for those of you who send me emails asking what I mean about universal life insurance being leaner with respect to premium to death benefit, this should paint the picture pretty well.

Come age 60 our death benefit has risen to $3.5 million. The difference between death benefit and cash surrender value is about $1 million. So here our gap hasn’t necessarily grown at a rate that outpaces our original death benefit.

Maybe this is what the opposition was referring to? Should we then forsake universal life insurance in favor of whole life insurance?

Nope, and here’s why.

The guideline premium was designed to do this. We want a lower death benefit because it squeezes out expenses. What do we get for this lower death benefit?

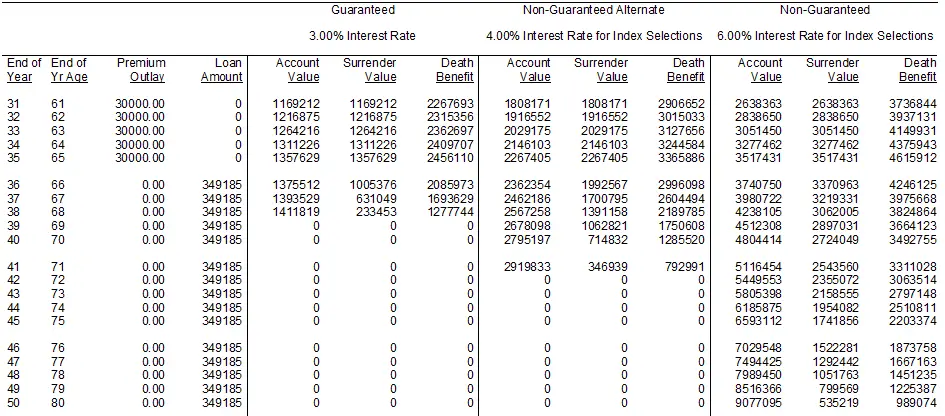

About $139,000 more in annual income; check this out:

[title color=”navy-vibrant” align=”scmgccenter” font=”arial” style=”normal” size=”scmgc-1em”]Click Image to Enlarge[/title]

That leaner universal life design yields considerably more income (we’ve noted this several times in the past). Some $5.2 million or $2 million more than whole life gave us. I think I can deal with the lower death benefit, now.

Death benefit is lower come age 80 in this scenario, but the internal rate of return is a good bit better. We’d need an alternative investment that yields a consistent 6.4% annually to rival this plan. Given the fact that this product really holds no more risk than whole life insurance, the math shows us that using indexed universal life further augments an already super low risk asset play to generate income.

Let’s be Clear about a few more things

To the amateurs out there who are yelling “I can get 8% on the stock market!” at their computer screens, I have two comments:

- Prove it

- Tell me who leaves their money in stocks when they retire

Then go back and calculate the Sharpe Ratio on your stock portfolio and let me know if you really think the risk is worth it.

Then do me one last favor, consider the taxable equivalent yield on this whole scenario. And let’s not get ridiculous about it. Let’s assume just a 15% effective tax rate.

For whole life insurance we’d need an equivalent yield of 6.5%. This number is actually woefully low-balled since the $3.4 million death benefit would max out tax rates, but I’m going to only assume 15% there as well.

And on the universal life side it gets even better. We’d need an equivalent yield of 7% to rival the results. Again, the nearly $1 million death benefit at death would also max out tax rates, but I’ll assume fictitiously low here as well.

Knowledge is Power

I’m full of corny clichés today. But there’s some truth to this. Cash value life insurance as a low risk asset and income tool works. If it didn’t there is no way any insurance company would let me design policies the way I do and place the amount of money we do into these policies (the liability is astronomical).

That doesn’t mean that every cash value product works for this purpose, and it also doesn’t mean that every insurance agent or broker out there has your best interest at heart. In every industry from medicine to law to car sales to insurance there are both good people and bad people.

There is no doubt that insurance agents can do damage with the product they sell. Just like there is no doubt that an inept attorney can do damage with the products he or she—essentially—sells. And simply finding a few examples of poor implementation of an otherwise good idea doesn't mean you’ve gathered enough evidence to declare the whole thing a sham.

When it comes to cash value life insurance, those who get it tend to love it, and those who don’t look elsewhere. But those who do get it enjoy the benefits of a truly unique and remarkable asset.

If you'd like to learn more about how you can make cash value life insurance work for you, contact us, we welcome the opportunity.