Podcast: Play in new window | Download

Just yesterday, we realized that since we started the podcast back in November of 2015 we've not discussed anything specifically regarding single premium life insurance.

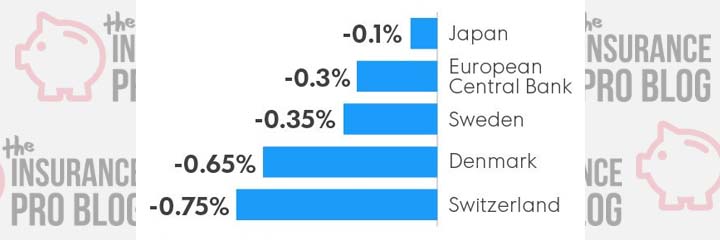

With interest rates today at their lowest point in recent history and for a protracted period, many life insurance companies have chosen to pull their single premium products. But there are still a few available.