Podcast: Play in new window | Download

There’s no doubt a number of people have made arguments against the ownership of cash value life insurance. You don’t have to spend a lot much time surfing ye olde’ interwebs to find such evidence.

Too many of these arguments are propped up on misinterpretations of the various products that exist–heck even the agents themselves can’t come to a consensus on how things work.

But one of my favorite literal interpretations about cash value life insurance that’s used to substantiate the opposition is the fact that life insurance companies keep the cash in your life insurance policy when you die. “You don’t get the cash when you die, the insurance company keeps it!”

They exclaim with sharp disapproval. And most of you who don’t know any better fall for it.

You can’t take it with you

The old argument goes something like this:

“When you buy permanent life insurance, the cash that accumulates inside your policy is not paid to your beneficiaries when you die. Instead the life insurer keeps the cash and pays you the death benefit.”

Oh the horror…

I’m here to confirm this statement. It’s true. Functionally speaking, no life insurer pays the cash value out of a life insurance policy to a named beneficiary. The cash stays with the insurer; the beneficiary gets the death benefit.

That’s Nice, but we like Proof

Alright, so I’m sure that you’d like to see evidence to back up this whole notion that “the product is worth more than the sum of its parts”…right?

Let’s do that.

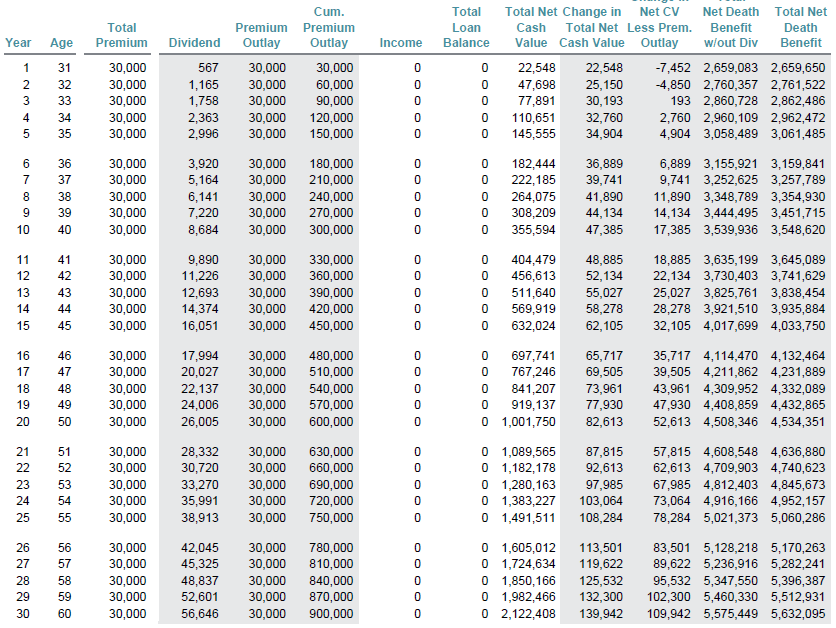

Here’s a blended policy designed to optimize cash and remain compliant with modified endowment contract restrictions. We have a hypothetical 30 year old who is placing $30,000 into the policy each year.

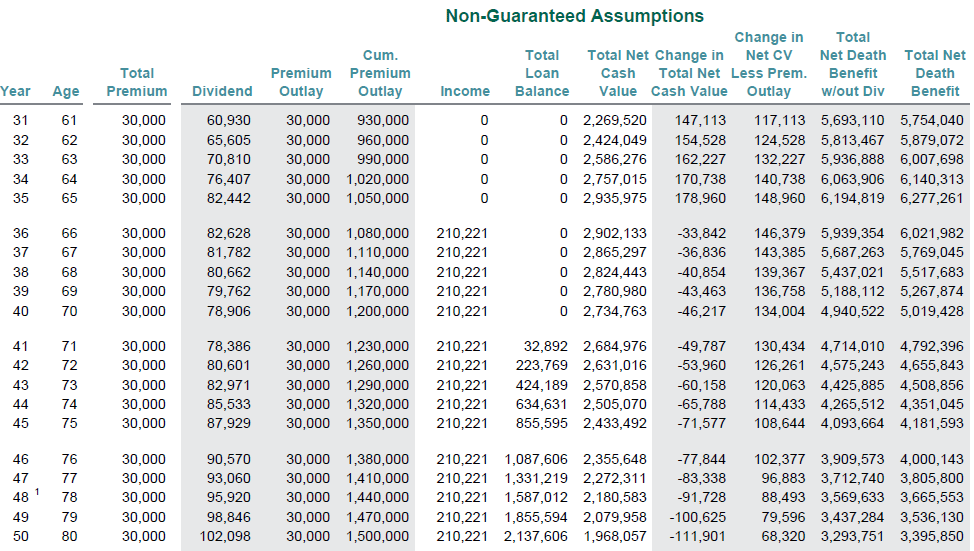

This individual will then take income from the policy from age 66 to age 80.

So we start with a $2.7 million death benefit and come age 60 that death benefit has increased to $5.6 million. To get there, our premium hasn’t changed at all. For those interested in the math, that’s an 8.04% return on death benefit.

But much more noteworthy (at least to our topic at hand) is the fact that the difference between the cash value and the death benefit is $3.5 million. So even after the insurance company “steals” our cash value we’ll have increased the death benefit by $800,000.

But why stop there? Let’s take a look at our income scenario.

The policy projects income of $210,000 per year.

That’s almost $3.2 million over the 15 year period. And at age 80 we have a death benefit of just a hair under $3.4 million. Let’s do the math on that, we’d need an equivalent investment account that yields a consistent 6.03% each and every single year in order to rival this plan.

That’s one hell of a yield in today’s market for a low risk asset.

When it comes to cash value life insurance, those who get it tend to love it, and those who don’t look elsewhere. But those who do get it enjoy the benefits of a truly unique and remarkable asset.

If you’d like to learn more about how you can make cash value life insurance work for you, contact us, we welcome the opportunity.