Podcast: Play in new window | Download

Ernst & Young published a study this year that speaks very favorably about permanent life insurance and annuities. The TL:DR version of the 18-page reports is that when they incorporated whole life insurance and annuities into a retirement plan, they increased both retirement income and “legacy value” for the hypothetical retirees. So should we rush to our nearest insurance salesman or women and ask for whole life insurance and annuities? Maybe not so fast. There are a few things to unpack on this one.

Augmenting Retirement with Insurance Products

The report, which you can download here, analyses three hypothetical families and contemplates five scenarios:

- Investment only (i.e. stocks and bonds) plan

- Investments with term insurance

- Investments with whole life insurance

- Investments with deferred income annuities

- Investments with whole life insurance and deferred income annuities

Unsurprisingly, the term insurance with investments modeling performed worse than the investment only (i.e. sans term life insurance) scenario. This is rather intuitive. If we have to re-deploy some of the money we intended to save for retirement towards some other expense, we save less money.

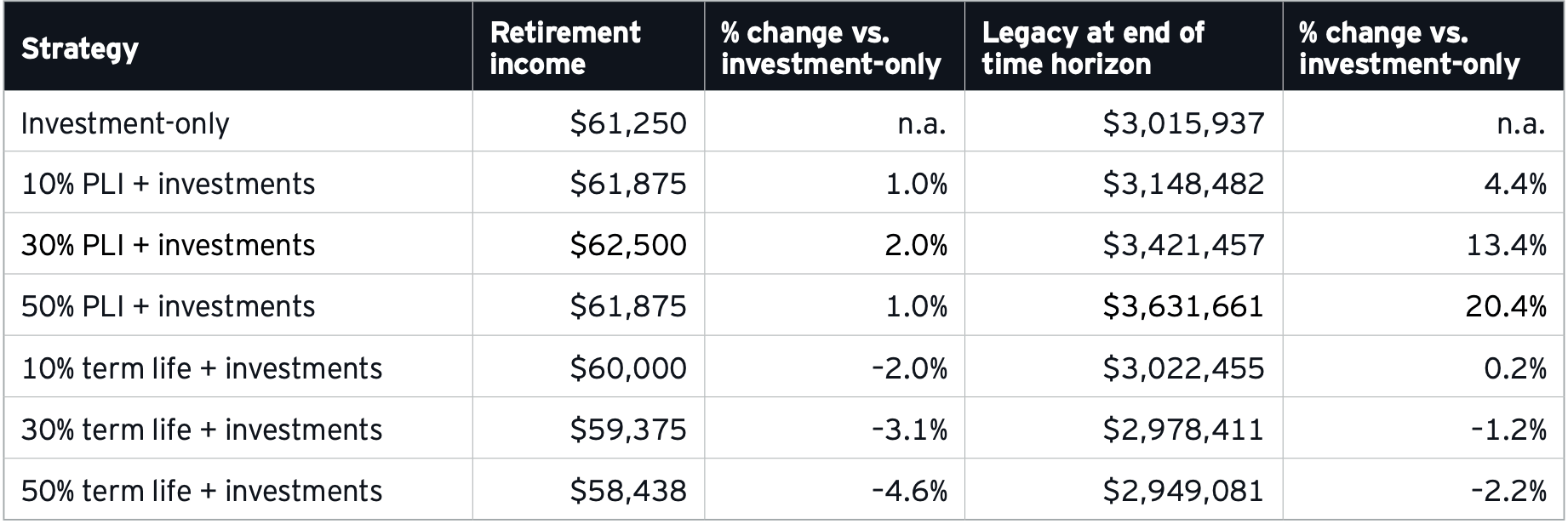

What is worthy of at least a moderate eyebrow raise is their findings that employing whole life insurance up to 30% of the money saved does result in both an increase in projected retirement income and legacy value (they defined legacy value as the balance of the portfolio measured in USD at the endpoint of their income analysis–age 95). Here's the chart from the report:

This increase isn't just over the term insurance mixed with a traditional investment approach, it's also above the income projections from the investment-only scenario where the couple owned no life insurance at all.

Does this mean whole life insurance somehow magically beats stocks? No.

The baseline investment-only portfolio is a 50/50 mix of stocks and bonds. When Ernst & Young added whole life insurance to the portfolio, they did it by subtracting some of the money allocated to bonds. So the whole life policy performed well against bonds in the portfolio.

There's one other element at play, which will also impact how annuities affect this analysis. Whole life insurance lacks volatility. When markets go down–and bonds tend to correlate moderately well with broader stock indices these days–losses created by the downmarket result in a decreased income generation potential. Whole life insurance is mostly unaffected by these events. Its complete lack of movement downward during market contractions usually provides a higher overall level of income creation.

The increase in legacy value is unsurprising. Whole life insurance provides a death benefit and this can augment what's effectively left over when the hypothetical couple dies.

Adding Annuities to the Analysis

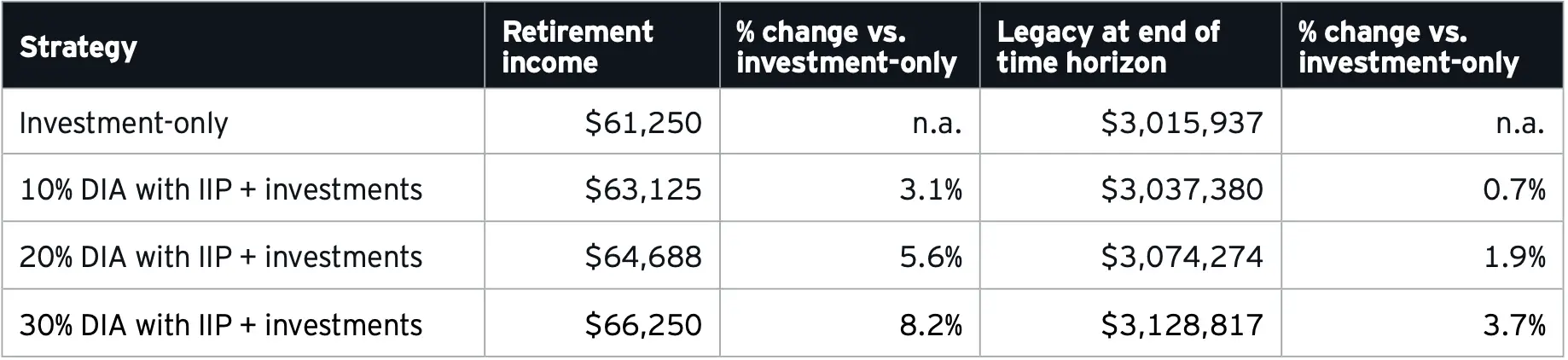

What happens if we swap the whole life insurance policy for annuities? We get these results:

Annuities produce a more significant increase in retirement income. Perhaps even more surprising is the positive effect annuities have on legacy value. This again comes from the subtraction of bonds and the limitation on volatility exposure these insurance products produce.

Using Both Whole Life Insurance and Annuities in the Retirement Plan

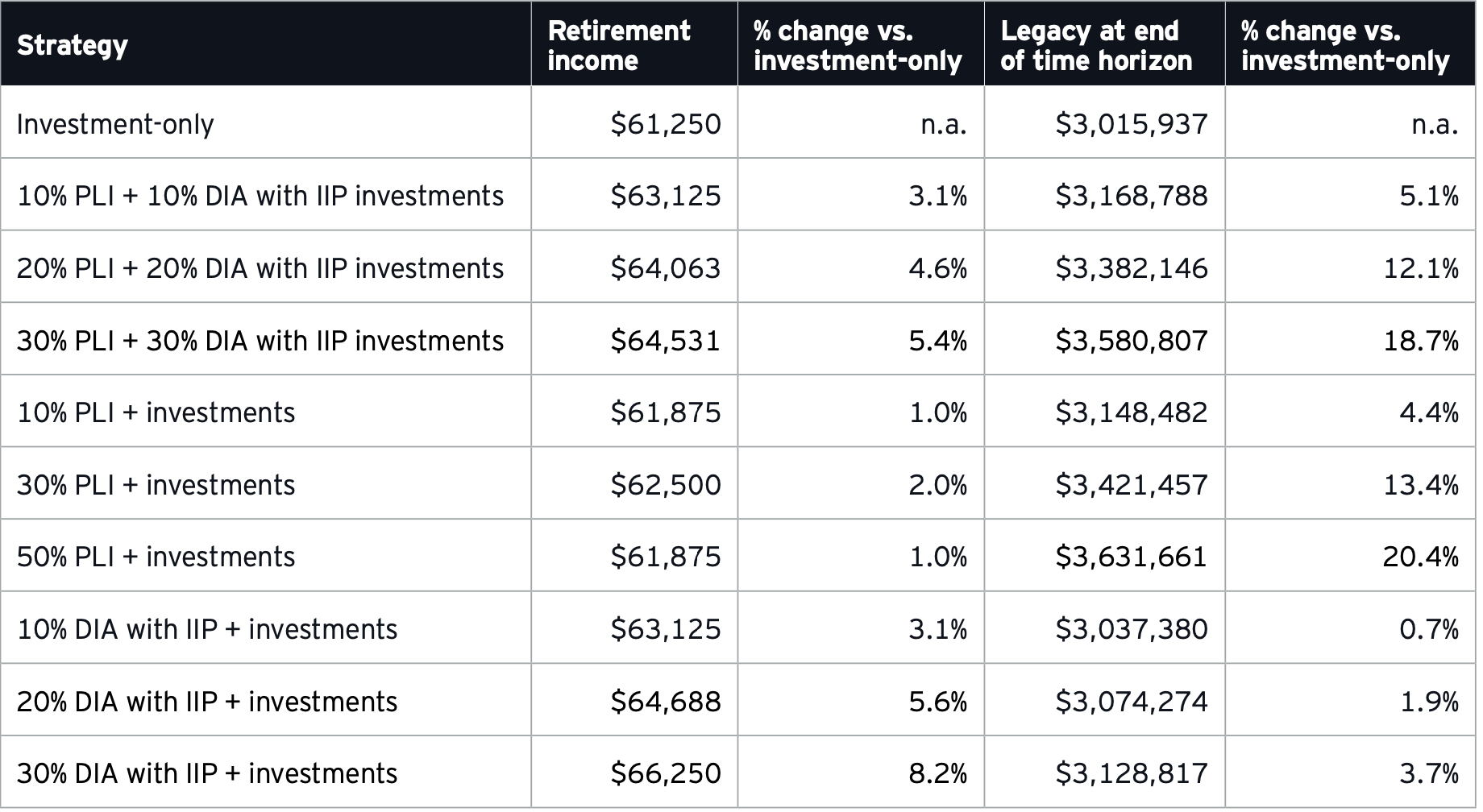

Now that we see the impact whole life insurance and then annuities had on the income and legacy value created, what happens if we use both as part of the retirement plan? Here are the results:

According to this research, there's a tradeoff made between income maximization and legacy maximization. Whole life insurance can augment income, but it more significantly augments legacy value. The inverse is true for annuities. So from here, it's essentially up to the individuals to decide what is most important and how they wish to prioritize objectives.

Criticisms Regarding this Research

The authors of this report noted that this is more a launching point for a broader discussion on how insurance products might help augment retirement accounts. It's a tad too easy to draw certain conclusions from the data that I think would be haste and sub-optimal. Here are some thoughts on where this data might go wrong.

First, the investment profile seems excessively conservative at younger ages. The 25-year-old couple used the same asset allocation of the 35 and 45-year-old couples in the investment-only scenario. While I do think the impact of owning cash value life insurance as part of a portfolio even as young as 25-years-old can have its benefits, I don't see any reason to further handicap the portfolio with bonds and a large equity position in the broad U.S. stock market. Greater risk can and should be taken at this stage in sectors with higher growth potential and risk–they can afford this; that's the point of incorporating the whole life insurance into the plan.

The term insurance example used annually renewable term (ART) life insurance to calculate the impact owning the insurance has on the end results. The authors further noted that they used an “industry representative” analog to compute values. ART is a nearly extinct insurance product offered by roughly a handful of insurance companies. It's surely not representative of how people buy term life insurance today, and it hasn't been representative for many decades. This misstep doesn't likely change the results much, but it's a significant blunder with respect to accurately modeling investor behavior.

The report presumably used regular participating whole life insurance to compute the impact of permanent life insurance on the portfolio. This is by no means an optimal way to approach whole life insurance as a component of one's retirement portfolio. The research also completely ignores the use of universal life insurance products. While I'll certainly concede that the majority of whole life policies purchased more closely conform to the theoretical policy used in this analysis, if they weren't worried about correctly modeling term life insurance, it shouldn't have hurt the analysis to review how tweaking whole life insurance to more optimal produce cash value–and very likely death benefit–results impacted results. The good news here is that there's a very strong chance the results of incorporating whole life insurance into a retirement plan–when done correctly–produce even better results.

The report is scant on details on the annuity products used. It also fails to address a common hold-up many people have regarding the income feature of annuity products. This being the fact that most contracts require someone to effectively hand over their money in exchange for a guaranteed income stream. While I'm not suggesting this should be an impediment for owning an annuity, it is a common tradeoff and there are also consequences to dying sooner than expected. How well Ernst & Young explored these considerations is not at all thoroughly explained in the report.

This said it's always nice to see someone take a look at how insurance products will affect retirement preparedness. This report is favorable to the idea and opens the door to more discussion.

Do they drop the term insurance at retirement? I think that is an appropriate plan to avoid high cost and fit with a busy term and invest strategy.

Hi Chris, they didn’t mention if they dropped the term insurance in their study.

Agree with your comment on a conservative portfolio allocation for 25 yr old. That said, I think the idea behind that analysis might be to show that even with a conservative portfolio allocation, incorporating whole life still outperforms an investment only strategy. So if the allocation is aggressive, it is reasonable to assume that investment portion of portfolio would just be better longer term in both scenarios, with and without whole life.