Podcast: Play in new window | Download

Did you buy universal life insurance between 1980 and 1999? If you did, you might be entitled to compensation from predatory life insurance sales tactics that duped you into thinking that you could buy cheap life insurance without any notice that what you were doing was a potential disaster. For years, life insurance companies willingly issued policies sold by unscrupulous salespeople who sought high commissions for the universal life insurance policy.

All of the above is a montage of various claims made by various media throughout the last decade concerning universal life insurance. They even went a step further to unearth some unlikely soul who bought a universal life policy that, after years of warning, lapsed due to inadequate premium payments. Oh if only there were some way to for insurers to have warned the unsuspecting public years ago that the premium they paid on a universal life insurance policy might not be enough to keep the policy in force…if only…

Universal Life Insurance Disclosures did Exist

I'll nullify these terrible anecdotes with my own anecdote. Recently, my grandfather passed away. This leads to the obvious task of sifting through a lifetime's worth of various documents (most of the things that should have been tossed out years ago).

We uncovered a collection of small life insurance policies held in a safe at my grandparents' house. This, of course, meant that I, being me, received the glorious task of figuring out if any of them are still in force–lucky me.

Within the collection of old policies was a large envelope from New England Mutual (the company eventually acquired by MetLife). In the envelope, I found a nicely written letter addressed to my grandparents from an agent who was following up with them on a recommendation to buy more life insurance. My grandfather was a longtime New England Mutual policyholder (he purchased a whole life policy from them back in the 1950s).

The letter was pretty basic life insurance sales tactic stuff. It Noted that his group term policy he had was only good if he remained working for his employer and that his whole life policy with New England was much too small to cover his lost income needs. Three sales illustrations accompanied the letter. Two were for variable universal life insurance, and one for what we now call current assumption universal life insurance.

The illustrations showed varying death benefit amounts, and I have no idea what conversation took place influencing the death benefit amounts. My guess is they come from traditional sales techniques to provide a few options using nice round numbers. I'm not so much interested in the death benefit amounts. What is interesting is what is clearly spelled out in the illustration, which is from 1996.

Universal Life Insurance Design and Disclosures

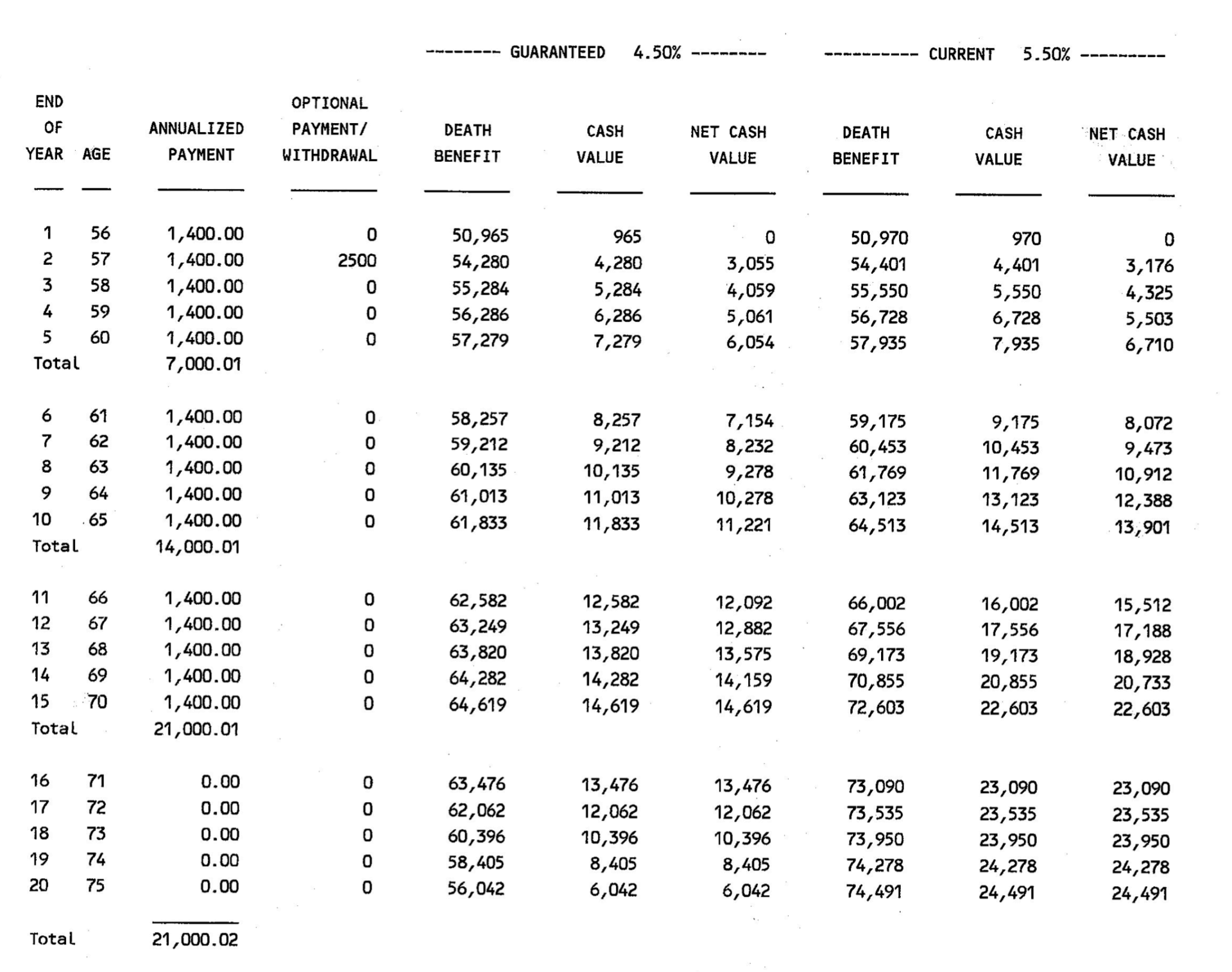

The proposed universal life insurance policy from New England Mutual lays out specifics in just three pages (oh the good old days…). The planned premium is $1,400 per year for a $50,000 death benefit. The plan was to pay the premium for 15 years. After that, the illustration assumes no premiums and yet the death benefit remains in effect. The death benefit option chosen for this specific policy is option 2 (increasing). I'm not sure why the agent would design the policy with option 2 for a short pay death benefit focused purchase, but there is no way to know what the agent was thinking in this case.

Here's what the illustration shows:

So we see a guaranteed and non-guaranteed ledger that shows what will happen to the policy assuming the current interest rate of 5.50% payable on cash value as well as what happens if the guaranteed interest rate of 4.50% and mortality charges increase to the highest allowable rates.

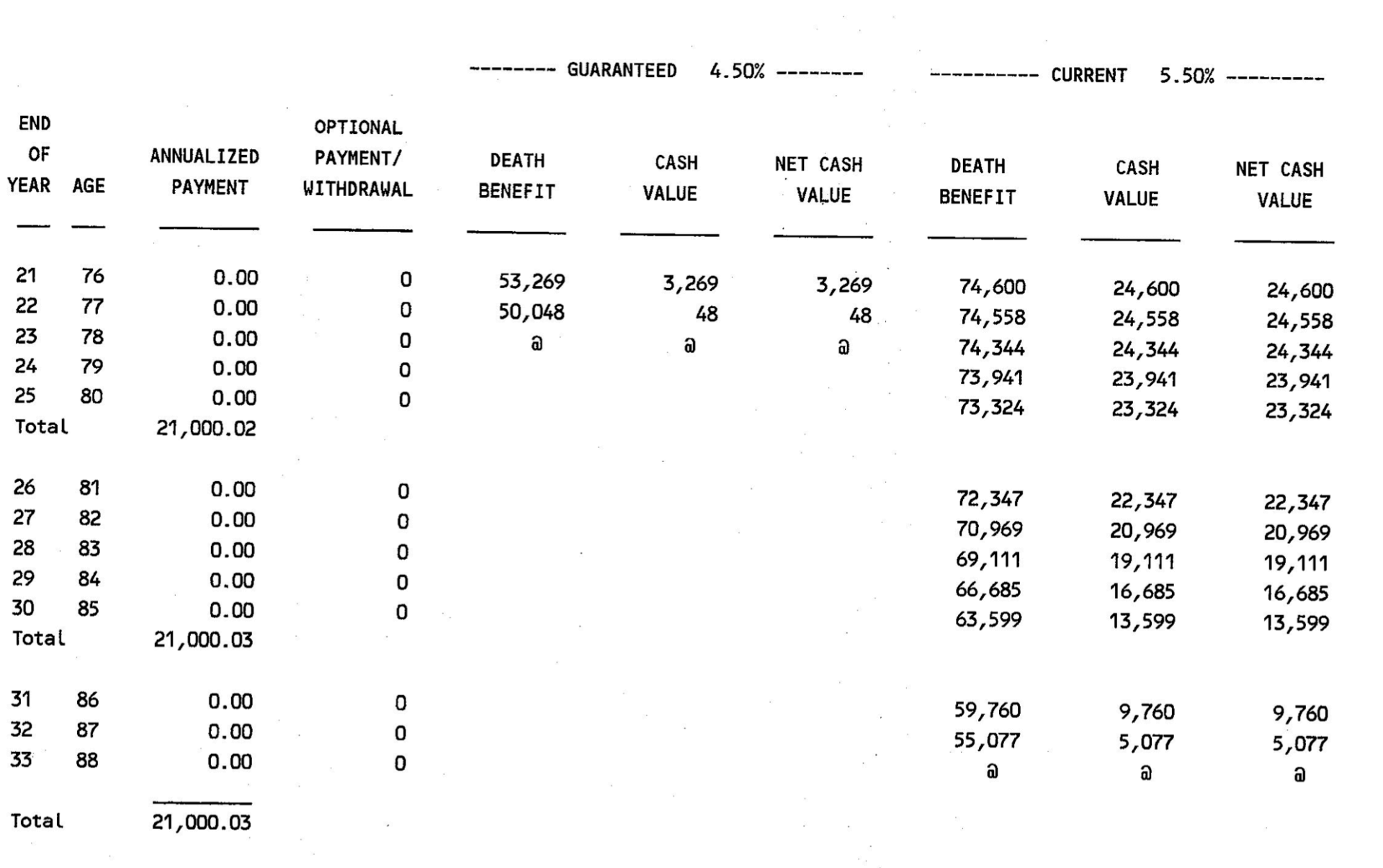

Here's the second page that compares the non-guaranteed and guaranteed ledgers:

This ledger is page 2 of 3 within the ledger. It clearly shows that the planned premium of $1,400 per year for 15 years (plus an extra premium payment of $2,500 in year 2) is not enough to keep the policy in force to age 100 when this policy endows. Even on the non-guaranteed side, the policy will lapse at year 33 the insured's age 88. If the guaranteed scenario played out the policy lapses at year 23 the insured's age 78.

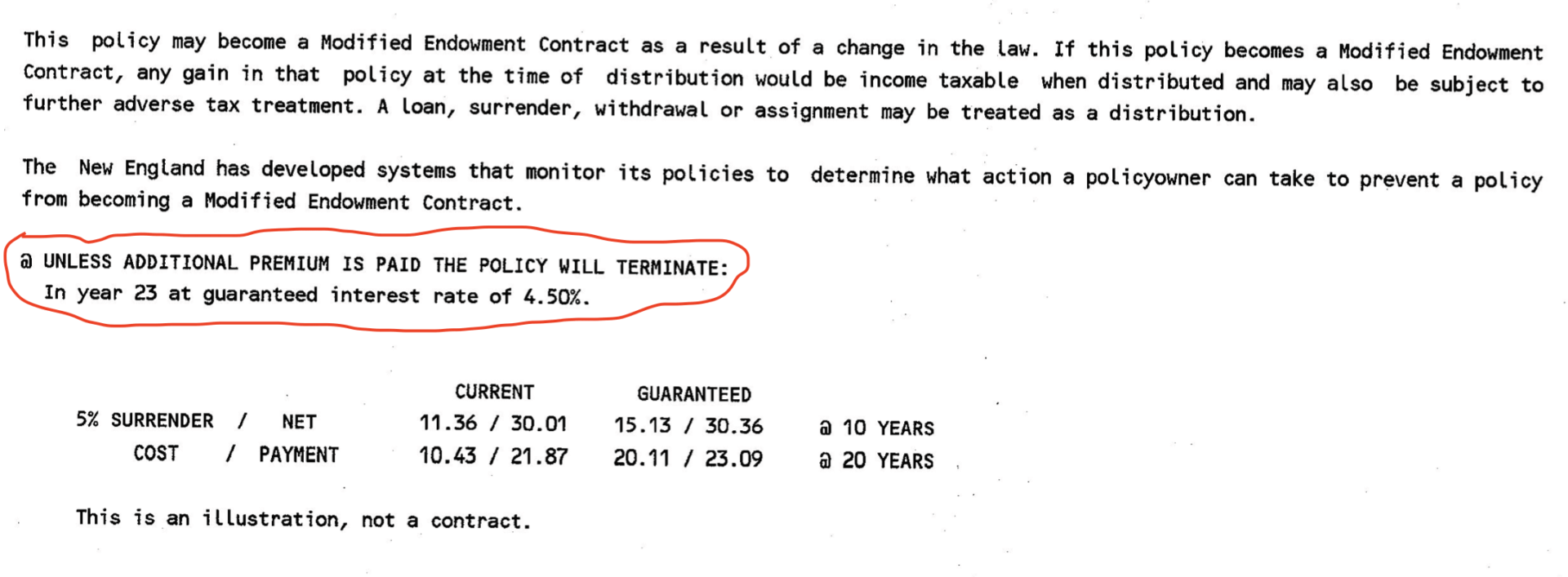

On page 3 of 3, there are several disclosure notices for the prospective buyer to review. Of particular note, is a statement made near the bottom of the page:

I circled in red the statement. It clearly calls out the fact that the policy will terminate given the planned premium if the guaranteed scenario plays out.

Variable Universal Life Insurance Design and Disclosure

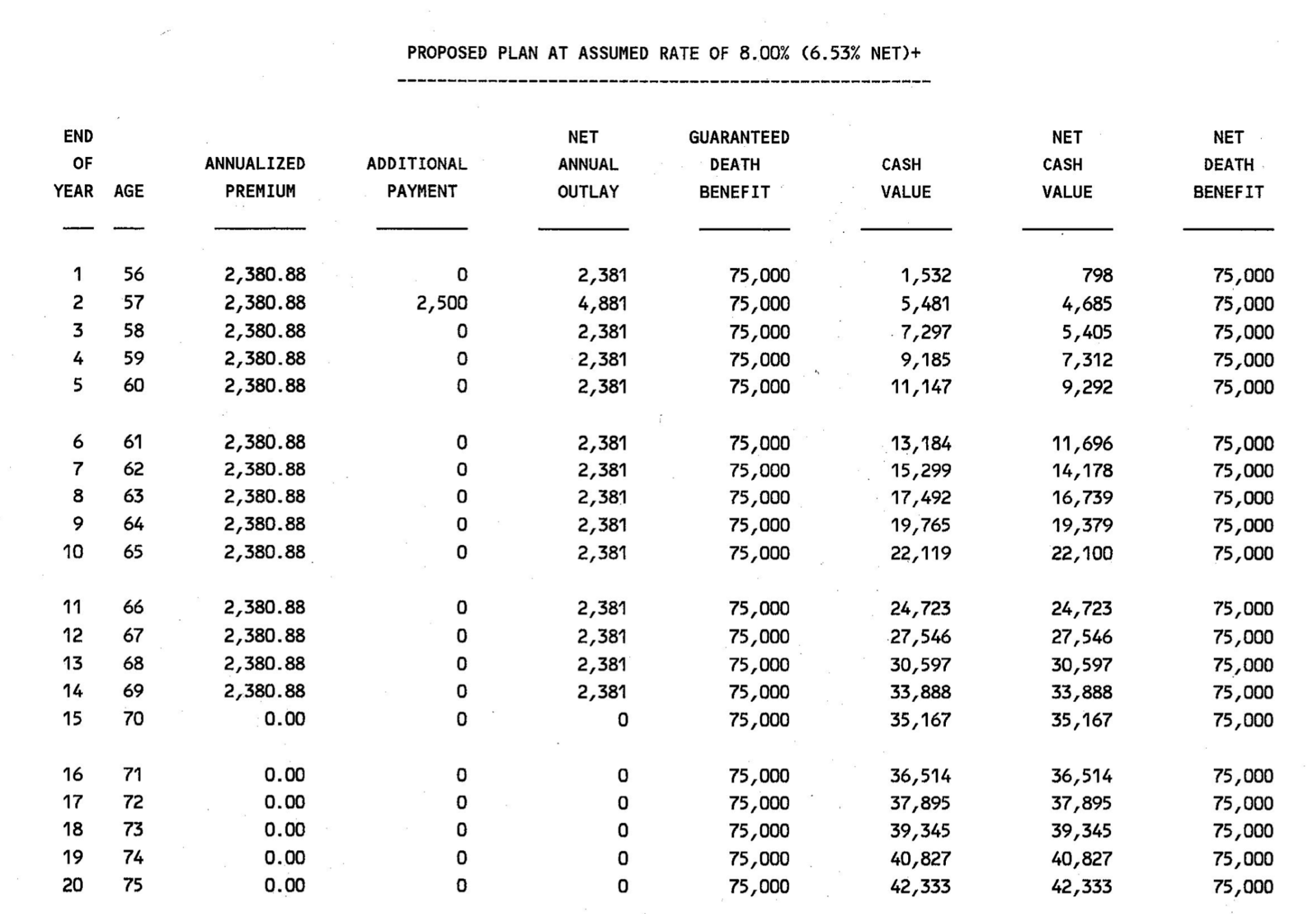

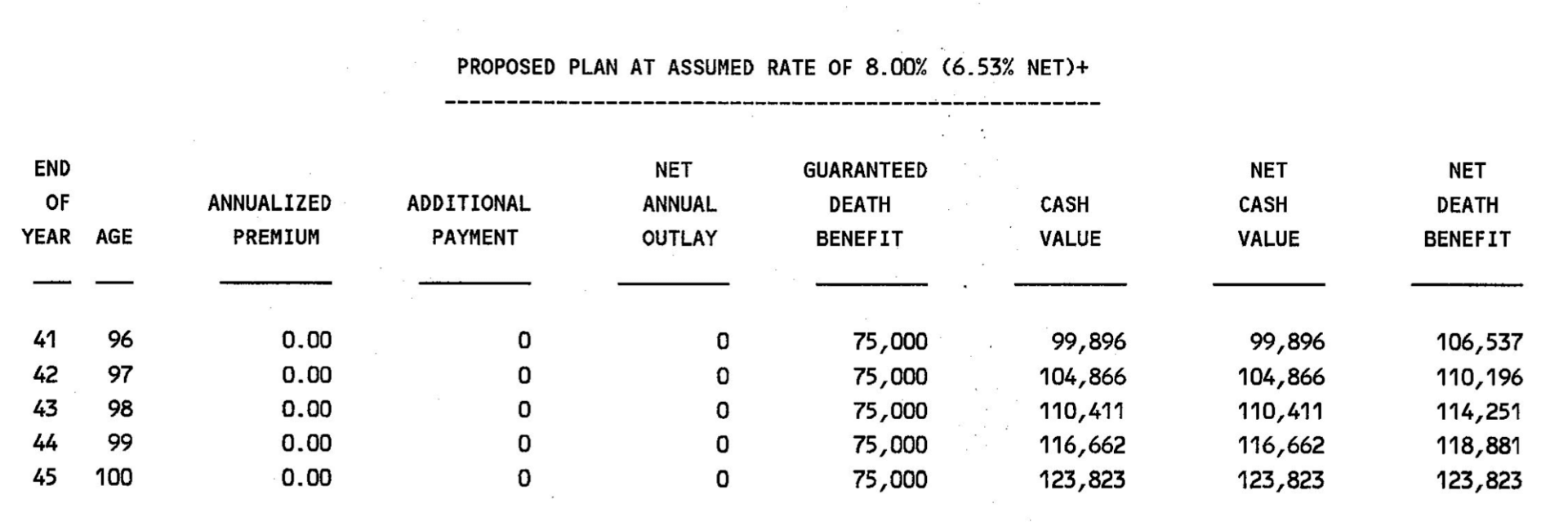

The proposed Variable Universal Life policy has a $75,000 death benefit and a planned premium of $2,380.88 paid for 14 years. There is also an additional $2,500 payment made in year two. This time the policy uses death benefit option 1 (level). The illustration is 13 pages long and assumes an 8% gross (6.53% net of expenses) interest rate for non-guaranteed values.

The VUL policy separates the non-guaranteed and guaranteed ledgers, but both are clearly within the illustration pages. Here's the non-guaranteed ledger first (since that is where the illustration begins):

The actual ledger is three pages long, but I've cut out page two. There's nothing remarkable about that page and I'm more interested in looking at pages one and three. You can see that with an 8% gross (6.53% net) assumed interest rate, the policy remains in force with the planned premium of $2,380.88 paid for 14 years.

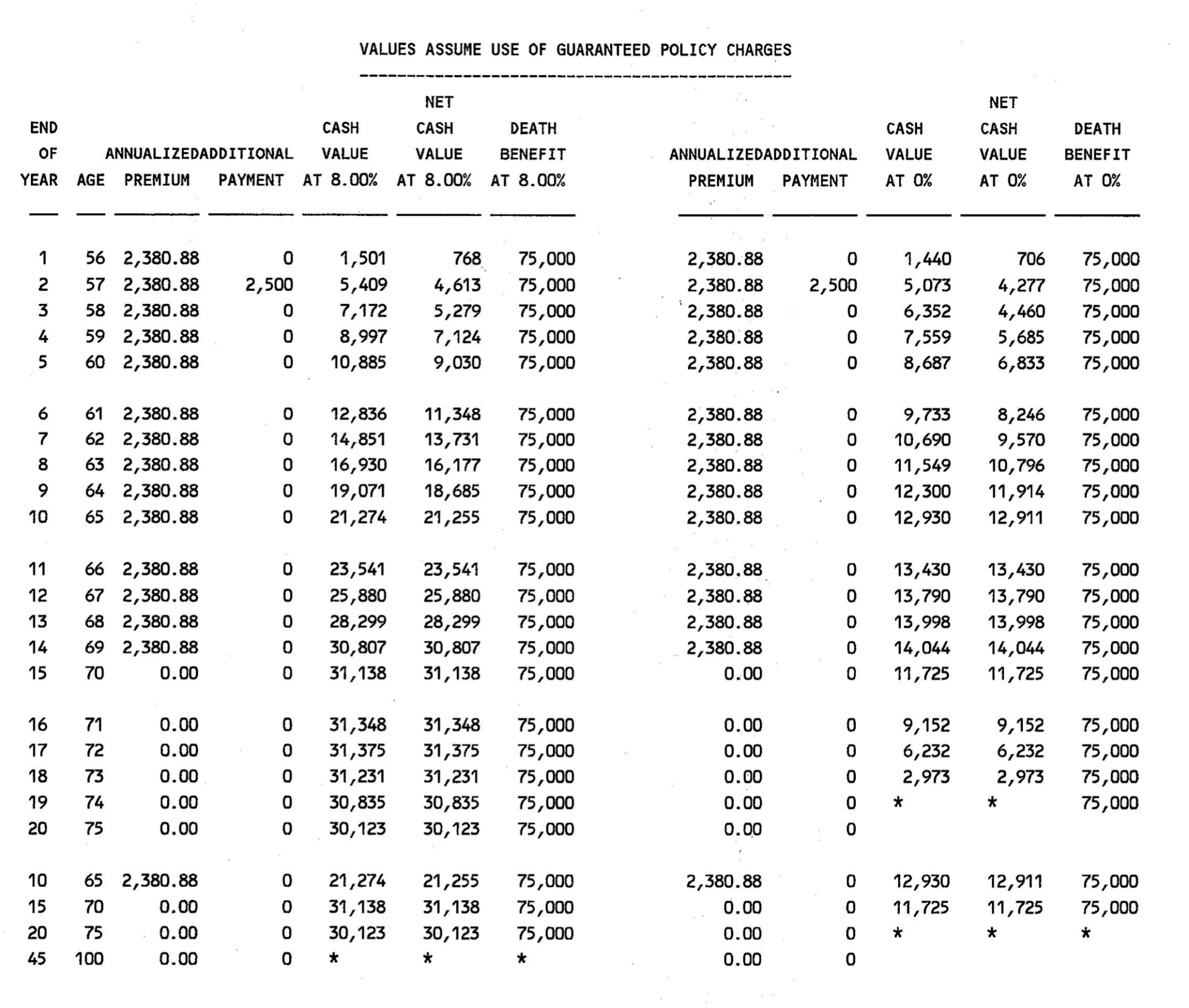

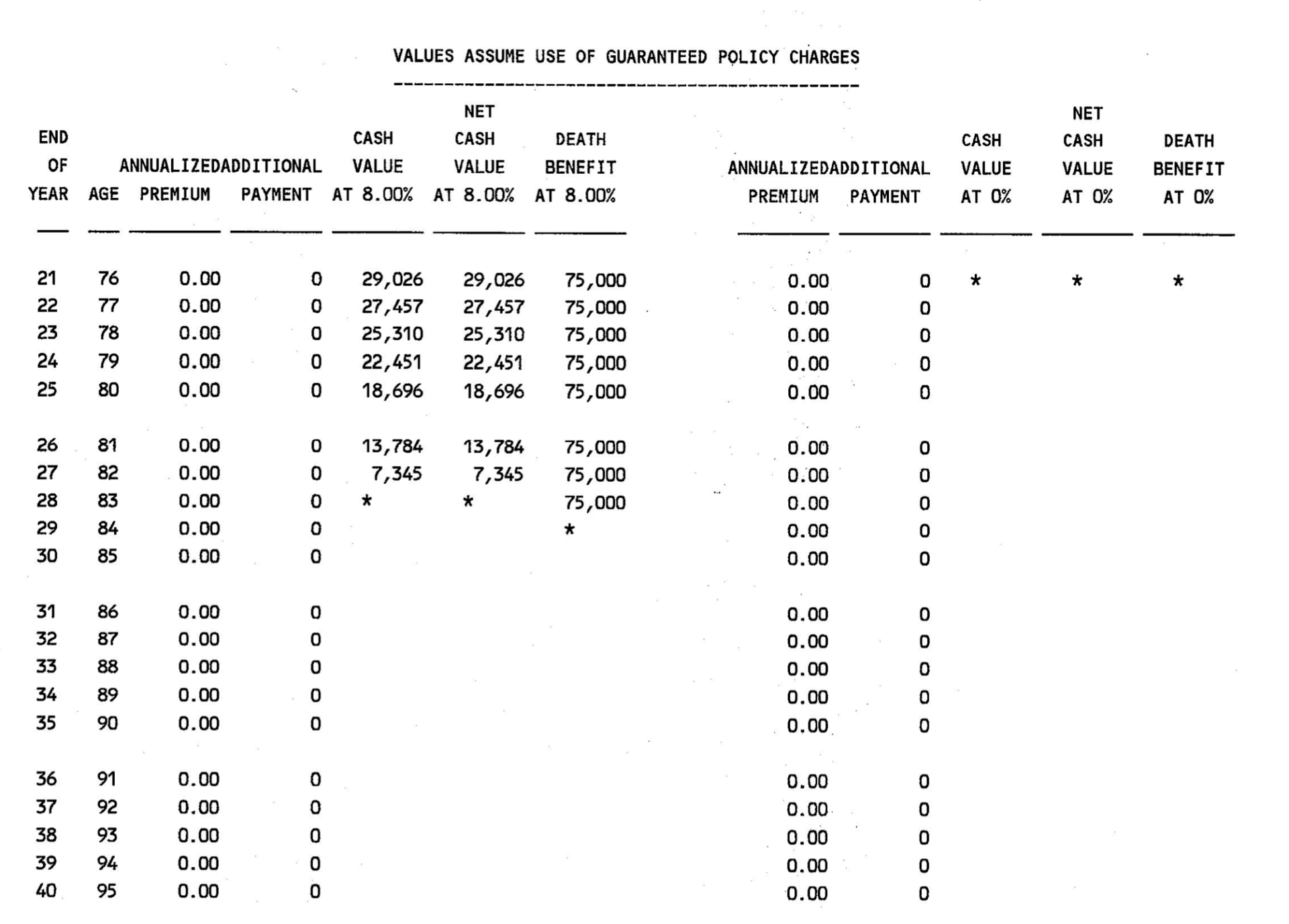

The guaranteed ledger pages immediately follow the non-guaranteed ledger pages; here's what those show:

The guaranteed ledger depicts two scenarios.

The first scenario (columns on the left half of the page) assumes mortality expenses increase to the maximum allowable and the policy earns the assumed 8% gross (6.53% net) interest rate in all years.

The second scenario (columns on the right half of the page) assumes mortality expenses increase to the maximum allowable and the policy earns 0% interest in all years.

As you can see from the guaranteed ledgers, the policy projects a lapse under the first scenario in policy year 29 (insured's age 85) and under the second scenario in policy year 21 (insured's age 76).

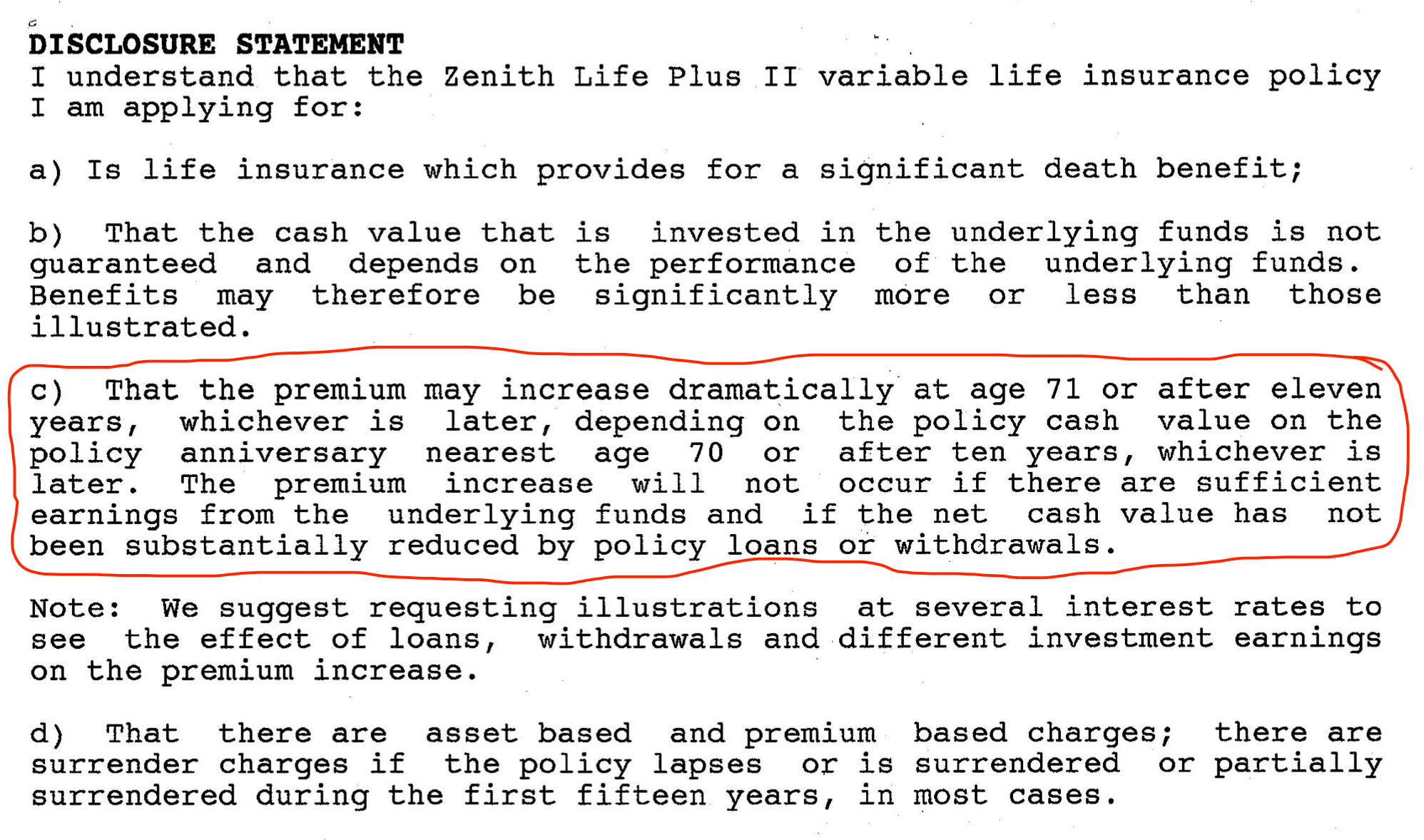

Page 13 of 13 in this illustration details several disclosures. One of particular note I've copied here:

I added the red circle to highlight the point. The disclosure under part C clearly notes that certain scenarios could unfold that would result in a premium increase. In fact, the disclosure uses the words “increase dramatically.”

Notice also directly under the paragraph I circled, that the disclosure suggests the prospective buyer look at several scenarios assuming various interest rates to obtain a better understanding of how varying levels of returns affect the policy values and premium increases.

The Sneaky Universal Life Story is a Myth

Since The Insurance Pro Blog launched in 2011, we tackled the subject of unwitting consumers buying universal life policies and finding themselves trapped in a situation of unknowable required premium increases to keep their life insurance protection. We noted every time that we doubted the policyholder never received any warning that this unfortunate reality was coming to fruition. We also showed (a few times) that rising universal life insurance expenses are traditionally modest and the bigger problems stem from a practice of some people treating universal life insurance like its a cheap alternative to whole life insurance.

You can see here that a lot of disclosure regarding premium adequacy and the differences between guaranteed and non-guaranteed existed as far back as 1996.

Also, note the size of these illustrations as I mentioned above. The universal life illustration is three pages long. The variable universal life illustration is 13 pages long. Today, illustrations for these products are many times larger. They traditionally range between 25 and 50 some pages long. I think it's reasonable to argue that it was significantly easier to read through an illustration back in the mid-'90s and get a good feel for what was going on. Today the same disclosures exist, but they are buried in a sea of endless pages seeking to over-explain even more policy features in a fashion that is largely helpful to no one.

The truth is disclosure existed for quite some time and many consumers chose to ignore those disclosures. I'm not suggesting that no agent ever manipulated information in such a fashion as to convince someone to buy a life insurance policy to which he/she would have otherwise said no thanks. But that is a problem of illicit activity and not a system-wide failure of the industry to properly warn its customers that implementing a policy on one fashion or another might be a bad idea.