Pension maximization refers to a specific retirement planning technique that can be used by couples to weigh possible pension payout options. You can also consider these options to be annuitization options as they are quite similar to what you will find in a single premium immediate annuity, like the ones I referred to in this article on creating your own pension.

So you've been slaving away for the past 30 years at your post and now that day is in plain sight. What day is that?

Your retirement date of course. That time where all of your hard work, saving, planning, and preparation culminate in that glorious event of no more alarm clocks, no more morning commutes, and no more TPS reports (for all my fellow Office Space fans).

Retirees are often faced with a difficult decision when sifting through the payout options for their pension, and unfortunately, they are forced to make an election without having complete information.

If you've worked in a place that has a pension or defined benefit retirement plan (most likely a government position), then you're going to be forced to make a very tough and irrevocable choice.

Irrevocable Choices for Your Future Retirement Income

That's right, you'll have to make a choice regarding your retirement income checks that can never be changed once elected.

That's right, you'll have to make a choice regarding your retirement income checks that can never be changed once elected.

You will be obliged to choose between the two most common payout options:

- Life only—A higher payout that stops when you die. This means that you get the most money possible every month but if you're married, your spouse gets nothing when you die.

- Survivorship—A lower payout that will provide some income to your spouse when you're gone. This option varies depending on your particular plan.

Life-only is fairly self-explanatory. If you die the week after your retirement checks start rolling in, your spouse is “up the creek” and has lost the income stream and cash value of your pension.

If you elect the survivorship option, you receive a reduced amount of money while both you and your spouse are living, however, it guarantees an income to your spouse in the event that you were to die first.

In our practice, our clients who are facing tough decisions surrounding survivorship options in regard to their pensions are typically retiring municipal employees, state government employees or federal government employees.

To further complicate the lack of good information that’s available to them, many folks have been misled regarding their survivorship options and are more likely to make a bad decision.

A major problem is that most people have no idea how long they will live after they retire and they don’t know how long their spouse will live into retirement. It seems even more impossible for people to make an educated guess on either by themselves.

Consider the financial risk of someone choosing a survivorship option instead of the life-only option.

If they do outlive their spouse, the retiree has now forgone a significant portion of their potential income stream. In many cases, they are being paid half as much as if they had chosen the life-only option.

How Does Pension Maximization Solve the Problem?

Our solution to your dilemma: a strategy that's been around forever but really isn't discussed very often—pension maximization.

It’s not a difficult concept to grasp and will make perfect sense after looking at an example. Take a look at the numbers below if you're a visual type of person and the different options will be cleared up for you.

It’s really a matter of comparing the numbers. There is no good way of projecting or assuming figures when you consider if this is a viable option for you, the best or should I say, only way is to know the exact amount of money that your pension will pay you for the various payout options.

When you look at the difference between the “life-only” option and the survivorship options you can see the difference in the payout and those are the numbers you have to use to solve the problem.

For instance, assume that Bob Jones is 59 and he plans to retire next year when he’s 60.

If he chooses the life-only option from his pension he receives $2,000/month. On the other hand, if he opts for the survivorship option he receives $1600/month and his wife will receive $800/month if he dies before her. This is a very typical “life with 50% survivorship” option.

Now if Mr. Jones is anything like most folks today, $2000/month is barely adequate. So, why would we think that Mrs. Jones would be able to get by with $800/month when he’s gone anyway? The math just doesn’t work.

In comes pension maximization to save the day!

We would evaluate Mr. Jones's situation fully to understand his options and any other sources of income. Then we would determine the difference between his two options.

In this case, there is a $400/month difference between the life only and the survivor option.

Assuming Mr. Jones is healthy and able to get a decent offer from a life insurance policy, he has $400/month to use to purchase a policy that will more than replace the income Mrs. Jones would have received if he had chosen the survivorship option.

It’s really six of one, half dozen of another.

We find that people can understand this concept, it’s not difficult to wrap your head around.

We find that people can understand this concept, it’s not difficult to wrap your head around.

However, they often times feel like there’s no way they could afford to pay $400/month for life insurance, especially after they’ve retired.

First off, we’re not saying they should…necessarily. Every case is different.

But we’re just making the argument that you could, mathematically.

Think about it this way:

Let’s say that you opened up a new cupcake bakery. These places are all the rage down in my neck of the woods. You are tickled pink to be baking up delectable culinary delights and don’t even mind your workday that now starts at 4 a.m. The store is packed with walk-in customers all day, you have more orders than you can handle and you’ve been able to raise your prices consistently with no customer complaints.

You just have one, tiny problem.

To offer your customers the convenience of paying with credit cards/debit cards, you have to pay 3.5% of your gross card receipts to the merchant service company.

As any good business person will do, you pass along your cost to your customer. However, as a courtesy, you decide to post a sign out front notifying your customers of the change.

Your sign guy has come up with two options for your sign and they are:

- There will be 3.5% added to the total for customers who pay with a credit/debit card

- All customers who pay with cash will receive a 3.5% discount

Don’t they both say the same thing?

Of course, they do.

But as a store owner, you should definitely choose option 2.

Why?

Because the psychology of a discount is always preferable to the agony of a surcharge.

Most people think that by choosing a survivor option on their pension payout they’re just reducing their payout. What I’m saying is that you are actually incurring an expense.

If your monthly pension is $2,000/month, what difference does it make if you choose to have $1600/month direct deposited into your account instead of having the full $2000/month deposited and then writing a check for $400/month to pay a life insurance premium?

The net result is exactly the same.

But the psychology of seeing a reducing bank balance cannot be discounted. We all know that life insurance is an expense. However, isn’t it the same expense as choosing the survivor option?

To make a rational decision you have to look at choosing a survivorship option as an expense…because that’s what it is.

An Example of How Pension Maximization Works

Let’s assume that Mr. Jones has decided to look at purchasing a life insurance policy to maximize his pension payout. Remember the difference in his case is $400/month.

So, assuming that he’ll have to pay the state and Uncle Sam some taxes on that $400, we’ll look at having $300/month available for life insurance premiums. Looking at the companies we have available, it looks like he could purchase a permanent life insurance policy (whole life or guaranteed universal life) with more than enough death benefit—around $250,000 for Mrs. Jones to generate a replacement income.

Also, in the interest of all things being equal, we have to factor in that life insurance proceeds are income tax-free.

So that $250,000 is the taxable equivalent of $312,500 (of we assumed a combined 25% tax rate). This gives equates to a present value of $167,720 in today’s dollars if we used a 3% rate of inflation for 21 years which is Mr. Jones's life expectancy at age 60 according to the life expectancy tables over at ssa.gov.

So, what’s the point?

Mr. Jones is simply reducing his monthly payout by $400 in choosing the survivor option but he is actually accepting an increasing expense.

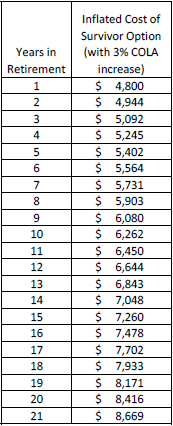

Keep in mind that every year he will most likely receive a COLA with his retirement benefit. Let’s assume for the sake of argument that he gets a 3% COLA increase every year.

During Mr. Jones’s first full year of retirement, he has sacrificed $4,800 in income by electing the survivorship option for his payout.

But if his payout increases every year, what does he really give up?

Let’s take a look at a chart that helps to illustrate the point.

Contrast the increasing cost of electing the survivorship option with the level premium cost of life insurance.

The longer Mr. Jones lives, the more appealing the fixed cost of the life insurance becomes.

Should You Look at Pension Maximization?

Using a pension maximization strategy involves a deeper discussion and some very specific calculations that will be dependent on your situation. In over 20 years of looking at these scenarios, I've never seen two that were exactly the same. But in every case, there was a clear winner, at least based on the math.

Using a life insurance policy can definitely help you maximize your own retirement income from a pension, however, you should get the policy as soon as possible. We have had quite a few instances over the years where someone waited and the cost was too much because of age and health.

Everyone’s case is different and you certainly have to consider all of your options, get in touch with us for more help.

I like your analysis. When I was working I developed an Excel template similar to yours. I found two issues: 1. The producers consistently ignored taxation of the additional pension benefit. 2. If the client waited until age 65 the insurance was going to cost too much. I never found a case where pension max worked. In running numbers I did conclude that if the client started as age 45 it would work. I always used NLG UL as the replacement policy.