You can usually borrow around 95% of a life insurance policy's cash surrender value in any given year. The rules that govern life insurance policy loans do vary from company to company, however, so it's important to understand a few basic rules about how much and when specifically you'll have the option to borrow money against your policy.

When can I Borrow Money against my Life Insurance Policy?

Companies differ on the earliest you'll be able to take a loan against your life insurance policy. For some companies, you have the option to borrow against the policy as soon as the policy has cash surrender value.

For other companies, you might have to wait a few years before you can take a policy loan. This looks something like, you must wait two years after the policy begins to take a loan out against your policy. It's incredibly rare for a company to make you wait any longer than two years.

The good news is, beyond a possible two-year waiting period, there are no other timelines you must follow for loan eligibility. There is no specific time of the year that you must wait until to request a loan.

How Does the Insurance Company Determine how much I can Borrow?

There is no unified rule that governs all life insurance policies and how much of the cash surrender value is available as a loan. The maximum amount is company-specific and governed by company rules. Most life insurers will peg the maximum amount to the loan interest rate of the policy. Doing this ensures that you cannot accumulate enough interest throughout the policy year to have a loan balance in excess of the cash surrender value of the policy.

For example, let's say that you have a whole life insurance policy with $100,000 in cash surrender value and the policy loan option has a 5% annual interest rate. If the insurance company permits you to take a loan at a maximum amount of 95% of the cash surrender value, you'll have the option to borrow up to $95,000.

One year after borrowing this money, the interest accumulated on the loan (assuming you make no repayments towards it) will be $4,750. If you choose to add the interest to the loan balance, the balance becomes $99,750, which is still less than the $100,000 cash surrender value you had when you originated the loan.

But please keep in mind that the above is merely an example of what might be the case at a specific life insurance company. It's entirely possible that a life insurer with a 5% annual loan interest rate on policy loans limits the maximum loan amount to some number below 95% of the cash surrender value.

As a general rule, life insurers do not typically set the maximum loan amount to a percentage below 90% of the cash surrender value.

Lastly, please note that cash surrender value and not death benefit decides how much you can borrow against a life insurance policy.

Can the Maximum Amount I can Borrow Change?

Yes, the maximum amount you can borrow can change based on the following three situations:

- Loan interest rate change

- Product type change

- Loan type change

Loan Interest Rate Change

If your life insurance policy has a variable loan interest rate, an increase in the loan rate could reduce the maximum amount you can borrow. This happens because the insurer prevents you from taking a loan that will grow to a balance larger than the cash surrender value in the first year of the loan.

Using the example from above, assume that this same whole life policy has a variable loan rate, and several years later the rate is now 10% instead of 5%. This will definitely change the maximum amount you can borrow. That same $95,000 loan will now accumulate $9,500 in loan interest in one year, and added to the $95,000 loan balance would make the total loan after one year $104,500. The insurance company will not allow this if you have only $100,000 in cash surrender value.

Product Type Change

You should never assume that the loan rules for one product type are identical for all insurance products issued by the same company. If the maximum loan amount on a whole life policy is 95% of cash surrender value at one insurance company, it could be some other percentage of cash surrender value for a universal life insurance policy at the same company.

This happens because loans can differ by product type. A whole life policy will often have a different loan interest rate than a universal life insurance policy, and this will almost always impact the maximum loan amount.

Keep in mind also that cash surrender value is the basis for maximum loan value. Because universal life insurance policies generally have surrender charges for the first several years, you have to ensure that you adjust for the surrender charge and consider cash surrender value and not simply the cash value of the policy.

Additionally, it's very important to understand that variable insurance products will generally have more restrictive available loan amounts. Because these products are directly invested in securities like stocks, the cash value of these life insurance policies can go down–in some cases rapidly in a short period of time. As a result of this volatility in cash value balances, variable life insurance policies normally have lower maximum loan amounts.

Loan Type Change

Some life insurance products permit more than one loan option. Indexed universal life insurance (IUL) is a great example of this. Most IUL policies have at least two (in some cases more) loan options from which the policy owner can choose.

These different loan options will often have different maximum loan amounts available to the policy owner. This happens before the loan interest and functionality differs.

For example, let's walk through an indexed universal life insurance policy with an indexed and traditional fixed loan option.

Let's say you have an indexed universal life insurance policy with a $100,000 cash surrender value balance. This particular IUL offers both a fixed loan option with a 3% annual interest rate as well as an indexed loan option with a 6% annual interest rate.

You will have a higher maximum loan amount option on the fixed loan than the indexed loan before of the difference in the annual interest rate between these two loan types.

Information Readily Available to you

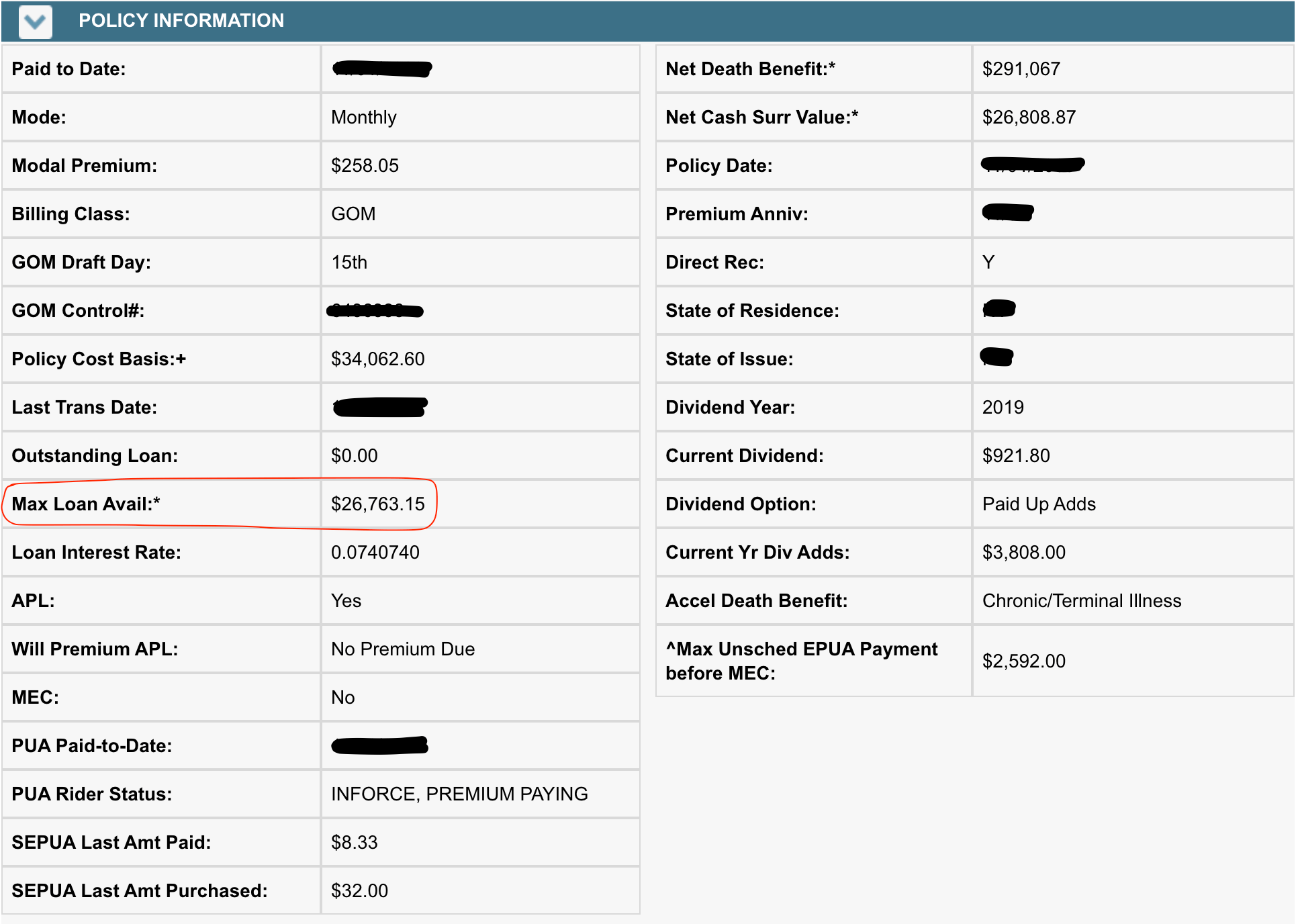

The really good news is that most life insurance companies regularly update and report on the maximum loan amount for their policy owners. You can usually look up your maximum loan amount by simply logging into your client portal and checking your policy's account values. Somewhere on that screen, you'll find an entry for maximum loan amount value. Here is an example of one company's reporting:

If you don't have ready access to your policy's online data, you can also call the insurance company to determine your maximum loan amount. Many insurers have automated systems that will tell you the maximum loan amount when you type in certain required policy data such as the policy number. Additionally, a customer service representative will also be able to tell you the maximum loan amount of your policy.