We’ve reported on operational cash flow among life insurers in the past and note that we hold this metric in high regard for a multitude of reasons.

Our philosophy is that operational cash flow shows us true profitability of a life insurance company, especially among whole life focused insurers. Why is that? Well, it's primarily because life insurers have a unique income reducing option at their disposal with policyholder dividends.

Unlike corporate dividends, participating whole life insurance dividends are technically classified as a refund of premium. This distinction allows life insurers to pay dividends to policyholders out of pre-tax income and reduce overall tax liability.

In addition, operational cash flow speaks to a degree of liquidity/flexibility and insurer has when facing various financial turbulence. In other words, if economic conditions deteriorate, a well established ability to generate a large amount of cash from everyday activity could cushion against the negative consequences of such an event.

It also Speaks to Dividends

We also believe that operational cash flow gives us some insight into potential dividend adjustments in the near term. Since most insurers make dividend payout decisions based on cash created from operations, a higher amount will hopefully sustain or increase the dividend payout to policyholders.

Since dividends are the key driver behind whole life insurance purchases were cash is paramount, we hold metrics that appear to influence dividends in the highest regard and place them under the highest amount of scrutiny.

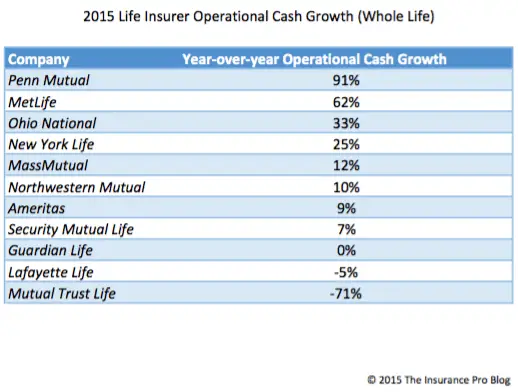

2015 Operational Cash Flow Results for Whole Life Focused Insurers

There is a wide spread among insurers in terms of year-over-year growth in operational cash flow. Here are the results for 2015:

Penn Mutual had a very interesting year, and its 91% increase should come with a degree of temperance. While Penn deserves kudos for such an impressive rise in operational cash, one must employ a degree of skepticism in the likelihood of the company’s ability to sustain or even come close to this result in subsequent years. One might also assume that this result is a function of a really bad 2014, this assumption would be mostly false. We will, though, be most interested in how 2016 unfolds for the company.

MetLife and Ohio National produced impressive growth in operational cash flow for 2015. We’d note that this feat is somewhat more impressive for MetLife given their sheer size and new woes combating the SIFI designation–something they’ve successfully removed.

Though not quite as impressive, New York Life, MassMutual, and Northwestern Mutual deserve praise for their double digit growth in this area from 2014 to 2015. All three are large life insurers so an increase of this magnitude deserves recognition.

Unfortunately, there are a few insurers who fared poorly in 2015. Lafayette Life’s decline of 5% is something we’re sure the company would have rather avoided. Worse of all is Mutual Trust Life’s sharp decline of 71%. One could argue that this result might be the cause of a particularly bad year, but the trend at MTL has been declines every year for the past five years (we’ll be evaluating this in more detail with all insurers later this year).

Limitations of this Analysis

While this review of insurers does give us some insight into operational excellence (or lack thereof) among life insurers, we must note the limitations of its usefulness. The dataset spans only one year and can significantly over or understate long term performance that is much more noteworthy. As I mentioned already, we’ll be reporting on this same metric under a longer time frame a little later this year.

This data is not intended as a sole decision making figure for any sort of life insurance purchase and a much more thorough analysis must be done to arrive at the appropriate life insurer and product for any individual circumstance.

Great article Brandon. I like this article’s view of cash flow and potential dividend performance. I have a couple of questions.

Do you think cash flow is the only or major variable in determining future dividend performance? If so, have you gone back to measure past cash flow analysis with dividend performance?

I know Mass Mutual has been busy lately, buying Metlife’s captive agency and annuity business, they have bought Oppenheimer at a nice discount, which may explain the low cash flow. Do you think these types of investments can affect the dividend performance just as much as cash flow?

Love the site, probably the number 1 go to site for whole life insurance.

Hi Justin,

I would say major but not only–though I suppose the argument could be distilled down to ultimately being cash flow is the overall consideration with several supporting variables affecting overall cash flow…perhaps.

There are other metrics we review that could be indicative of a rising or falling dividend. We certainly believer that overall investment yield could impact dividends (but this is a component to operational cash flow), we also look at interest margins (less so a function of cash flow, but tangential to the overall picture).

Surplus is a subordinate consideration insofar as it could be a place the insurer taps to sustain a dividend in a bad year (i.e. it might be particularly good news if the insurer has strong cash flow and a large surplus position since it has the option to use surplus if it experiences a temporary weak cash flow situation).

I’ve not personally evaluated dividend movement with respect to cash flow performance, but we do know from first hand conversation that most (if not all) insurers make dividend decisions based on operational cash flow results. There are some tangential variables, but none of them are sustainable without strong cash flow.

It’s absolutely the case that MassMutual can use subsidiary business activities to support the dividend and they are not the only insurer to do this. Guardian uses a substantial group businesses network to support it’s dividend payments and Penn Mutual generates considerable income from institutional and retail money management services it provides.

Thanks for the feedback, BTW. Glad to hear you enjoy the site!