We receive phone calls and emails every week from people looking to “de-risk” their portfolio and possibly add life insurance as a complement to their other investment and savings strategies.

A comment that tends to trend among these good folks notes that while we’ve done a pretty decent job explaining the more esoteric aspects of life insurance (according to the comments) it’s still somewhat difficult to understand exactly how this works and why it’s beneficial.

I can accept and agree with this comment and in an attempt to build out more comprehensive understanding I'd like to present a case study today that highlights some of the power behind life insurance when used as an asset in one’s portfolio. We’ll be publishing several more of these in the coming year. While we’ve been given permission to share these stories, names have been altered a bit to protect identity.

Daniel a Longtime Bond Investor

Daniel, a 48 year-old software engineer, came to us with a degree of frustration over available bond yields. He’s been pretty aggressively saving money in bonds for years and was quite well read on the subject of bond investing. His concerns were two fold:

- Low yields left him worried about total return forcing him to consider riskier investments to squeeze out better ROI

- Potentially rising interest rates could greatly diminish his principal invested in current bonds

Whole Life Insurance as a Solution

We used a lump sum funding strategy for a whole life insurance contract to transfer $500,000 into a policy making heavy use of paid-up additions and blending ensuring max cash accumulation in the policy. Projected results were very attractive.

By year 10 projected annualized return on Daniel’s money was 4.66% and by year 20 it was 5.72%. He was quite happy with these results and noted the difficulty he’d have in finding bonds to compete with returns like this.

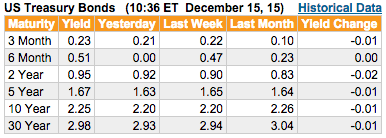

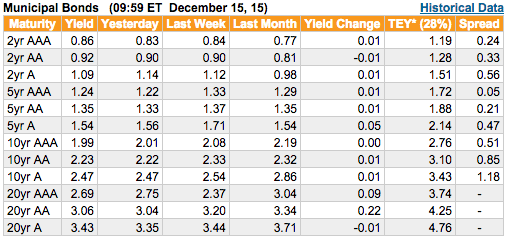

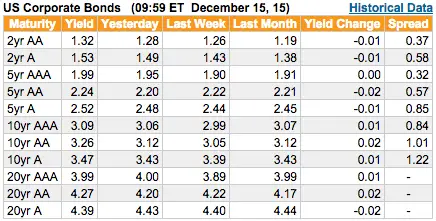

To give you a better idea, using data from BondsOnline here are the current yields (as of 12/15/2015) for various bonds:

As you can see, A-rated corporate bonds are the best in terms of yield (excluding tax considerations) at 3.47% with 10 year maturities and 4.39% for 20 year maturities. But there’s more to understand.

Bond yields, however, are the income produced by the bond. One cannot automatically reinvest bond income. One could take the bond income (if large enough) and buy new bonds at whatever the newly prevailing yield is (maybe higher or lower than the original bond). There is no easy way to compound bond earnings.

The annualized return on the above referenced 10-year A-rated corporate bond for the same amount of money is 3.02% and for a 20-year A-rated corporate bond 3.20%.

But that’s not all…

The Additional Benefits

Beyond a higher return on Daniel’s money, the whole life insurance contract afforded these additional benefits:

-

- Principal Protection: If interest rates go up, his current cash value in the policy remains without loss due to the “bond seesaw.” In fact, not only is he protected against principal losses due to rising interest rates he will likely achieve higher returns as well as insurers buy up newer fixed interest investments and raise dividend rates due to higher investment income.

- Liquidity: If Daniel wants more cash than his bonds generate in income, he needs to either sell bonds or pledge them as collateral (generally at no more than 50% if their current market value). With life insurance, he has access to any fractional sum of his current cash value (generally up to 95-98% of current cash surrender value). He does not need to sell anything, nor does he need to go through a credit application and pay loan origination fees.

- Tax Deferral: The growth in cash values inside Daniel’s policy are not subject to tax liability. Further, if/when Daniel decides to remove cash from the policy he can do so without incurring tax liability provided the policy remains in force

- Funding Flexibility: Though we set this policy up assuming a specific systematic movement of cash into the whole life insurance policy, Daniel can adjust this as necessary. He can even decide to place more money into the policy in later years if he desires and he doesn’t have to make those payments to the policy in large chunks as would be potentially necessary with direct bond purchases.To be clear though, once the initial $500,000 was placed into the policy, Daniel is under no obligation to place any additional money into the policy.

- Death Benefit: While not a huge benefit in his eyes the whole life policy definitely comes with a death benefit. While that death benefit may not be a major selling point at this stage, it’s existence opens up an array of options in later years. Daniel could leverage that death benefit to more freely spend other assets, use other financial tools like reverse mortgages with the plan to repay the loan, sell the policy for an amount between his cash value and death benefit, or use the policies accelerated death benefit to defray long term care expenses.

The Whole is Greater then the Sum of its Parts

Not to be all cliché or anything, but this statement is true. Life insurance offers an array of benefits that no other financial tool can accomplish.

On top of all that, it’s a pretty spectacular tool purely for rate of return on your money. Add in the additional perks that it brings along, and you have a very unique and powerful financial tool.

The policy used for Daniel was not a standard off the shelf policy, though. So please don’t assume that any plain old whole life policy will do. If you’d like more information on how this might work for you, please don’t hesitate to reach out to us. We’d be delighted to discuss with you.

“We used a lump sum funding strategy for a whole life insurance contract to transfer $500,000 into a policy making heavy use of paid-up additions and blending ensuring max cash accumulation in the policy.”

What is done to avoid the MEC conflict here? Does the structure of the blended policy suffice, or is there more to it?

And why WL vs IUL? Is it a case where you looked at both and WL won, or can this sort of move always only work with WL?

And out of curiosity, what was the actual initial death benefit on the half-million dollar blended policy? And at what year out did the policy have more cash value in it than was placed in the policy?

I love this stuff.

Great blog post!

-Jeff

Hi Jeff,

I’m not exactly sure I understand what you are asking with questions #1.

Not a specific reason that whole life insurance wins out. In many cases indexed universal life insurance is a great or even better option (I’ll be publishing another case study in a few weeks that used indexed universal life insurance in a similar circumstance). This particular client simply felt more comfortable with whole life insurance.

Initial death benefit was just slightly shy of $2.3 million.

Policy projects a positive return on cash at year five.

I am a new agent, how did you come up with the rate of return for the 10 and 20 year period? Can you send me a illustration so I can sell something like this?

Hi Henry,

I simply calculated rate of return in a TVM calculation given the initial $500,000 and using the projected cash value reported by the life insurer as the future value in years 10 and 20.

I don’t think the illustration for this will be particularly helpful for selling something like this as it’s not going to speak to much of what was discussed in this blog post. The data was extracted to make the point.

Just to clarify, the 4.66% is the 10yr IRR on premiums out of pocket? Does this include dividends or is this only against the guaranteed CV part?

Hi Andreas,

This includes dividends.

Also, can you comment on how such a policy would be affected by rising or negative interest rates?

An in force policy wouldn’t necessarily see much of an effect for a few years. The insurance company already bought the bonds with the premiums paid to that point and uses the income from those bonds to provide the policy benefits. The impact depends on how long rates stay where ever they moved.

Negative interest rates are usually a federal debt phenomenon. While insurers do buy some federal debt, it’s not the majority of their bond holdings.

Rising rates would likely have a delayed positive impact. Insurers won’t be able to immediately increase returns on policies because they’ll still own a lot of older debt that is paying a lower yield. That yield will continue to fund policy benefits and the insurer will achieve higher yields on bonds purchased with new premium dollars, but it will take time for the insurer to make any significant increase in returns on policies.