Podcast: Play in new window | Download

In the world of risk there are specific things that typically get mentioned–market risk, liquidity risk, interest rate risk and systemic risk. But before you all run away thinking that we're going to get in some mind-numbing conversation about such esoteric concepts…don't fret, we're not.

No, in fact we're going to discuss a different type of risk altogether. One that is much more practical and is very real. Or at least should be very real to us all.

There's one risk that is the most infamous of them all (or should be)…sequence of returns risk. I know we throw around such terminology as if it means anything to the rest of the world.

We refer to it as if it's as common as Advil®.

But what does “sequence of returns risk” really mean? It's the risk that you face as you accumulate and/or spend down the assets you've accumulated and having returns that occur in a particular order that accelerates the risk that you'll run out of money more rapidly than you thought.

It's a concept we've outlined before in our very obscurely named post:

Why Life Insurance Works So Well for Retirement Income.

An Illustration to Make it Real

Let's talk about Bob.

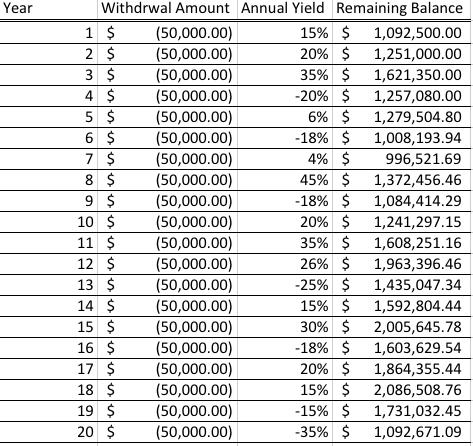

Bob has a portfolio with a value of $1 million. He has decided that he's going to take $50,000 (5% of his balance) each year from his portfolio as “income” to supplement his social security and his small pension.

For this illustration we're looking at a 20 year time period and we're assuming an assortment of various returns (in our attempt to model how the market might behave–ups and downs).

The average return for the 20 year period is 6.85%.

If we're being super geeky, we would refer to this 6.85% as the arithmetic mean.

Assuming this set of random returns, we distribute Bob's $50,000 per year from the $1 million balance. And after 20 years, Bob has a bit more than a $1 million.

By virtue of market appreciation, Bob hasn't lost any of his principal balance. In fact, he's a little better off than when he started out and he's managed to take out $50,000 per year.

So, he's taken a total of $1 million (20 years x $50k/year) from his portfolio and he still has a bit more than a $1 million.

Pretty sweet.

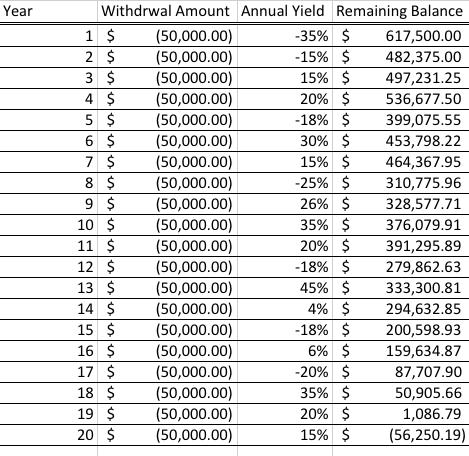

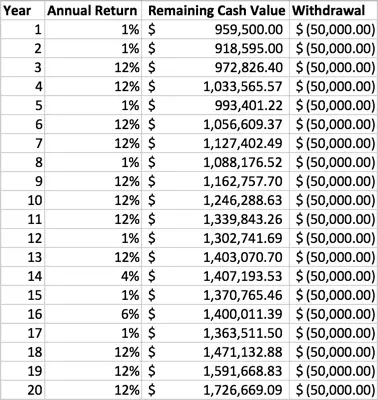

Now, to get show clearly illustrate for you sequence of returns risk, we've taken the exact same returns…only we flipped them over so that they occur in reverse order.

Bob starts with the same $1 million and withdraws $50,000 per year. The average return is the same 6.85%.

But because the returns fall at different times during the 20 year timeframe, Bob runs out of money at the end of year 19. See the numbers below.

What's happening here? Why does Bob run out of money if his average return is the same?

Assume that scenario #1 is akin to Bob starting his 50k “income distribution” in the late 90's when the tech bubble was the tide raising all ships. Scenario #2 is like Bob taking the same 50k but starting in early 2007 or maybe the spring of 2000 is a better example.

As a result of being hit with negative years at the very beginning, the portfolio takes a beating. And because Bob is taking out 50k every year, he compounds the effect of the problem.

The big issue here that's totally out of Bob's control (and everyone else's for that matter) is the timing at which a particular return takes place. You can diversity all you want and you can reduce certain risks.

But the diversification is too often misapplied. Too many people assume that a certain portfolio mix (stocks, bonds, commodities, real estate, etc.) with a particular risk profile allows them to project an average rate-of-return(ROR) of “x”.

Therefore, when they model income distribution scenarios, they can assume a static ROR. And that resulting ROR allows me to move forward with confidence.

It works…on paper. In a scenario where Bob assumes a static 6.85% year after year, he never runs out of money.

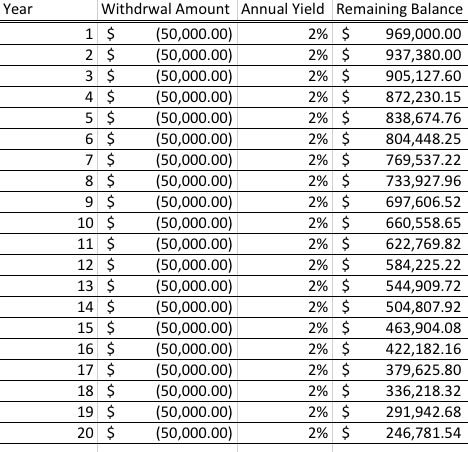

In fact, if you go back and assume that Bob was able to achieve a static 2% each year, he would not have run out of money during the 20 year time period. Here's a chart to illustrate that:

Our point is that you can't control when a particular return takes place. You only get one shot to get this right. You can't go back and undo a bad scenario after the fact.

The best advice any financial planner/advisor could offer in a scenario like #2 is, “Hey Bob, you need to make some adjustments to how much money you're taking out of this portfolio. Otherwise you could have a problem on your hands that looks a lot like you running out of money.”

You don't get to swap out good years for bad ones, once it's happened, it's done and baked in.

What Does This Have to do with Life Insurance?

Last week we pointed out that life insurance isn't heavily impacted by this “sequence of returns risk” problem. One of the many reasons we're such big fans.

Yes, there can be some variability with life insurance in terms of return–dividends can change (whole life) and indexed interest rates will vary (indexed universal life). But the lack of ever experiencing the negative years greatly diminishes the potential problems associated with sequence of returns risk.

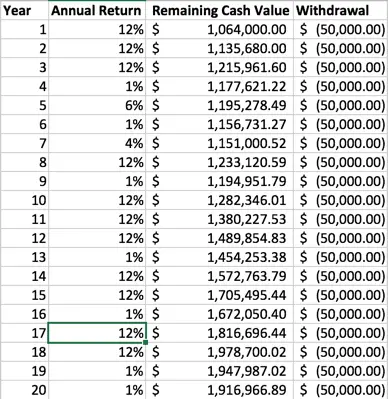

A hypothetical illustration using Bob again. In this example, we're substituting an IUL policy with a 1% floor (worst it can return in any given year) and a 12% cap (best it can return in any given year).

In both scenario #1 (good returns early) and #2 (bad returns early), regardless of when Bob experiences the negative returns, he ends the 20 year period with well over the $1 million he started with.

Scenario #1 (positive returns early)

Scenario #2 (negative returns early)

Granted, in a situation where he experiences good returns early on in the “income distribution” period, he ends up with more money. But the difference as you can see is less than $200,000. And in either scenario using the IUL policy puts him way ahead of the initial $1 million balance.

Another Point Worth Making

With life insurance as your income generating tool, there's no adjustment that has to be made in going from the accumulation phase of life to the distribution or income phase. Bob doesn't have to figure out what he's going to sell to raise cash so that he can take the money out.

He's not in a situation where he's having to hunt around for yield (forcing him to take on more risk) and he doesn't have to sell positions where has large gains (creating capital gains taxes).

The policies actually become more efficient as time goes on. No decisions about what to buy or how to rebalance. So that means that sustained periods of negative returns are not nearly as big of a crisis when Bob uses life insurance because he's not “double compounding” his downside by selling positions that have already taking a tumble in market value.

He doesn't have to worry about being forced to sell at the wrong time because he needs the money.

To sum it all up, using life insurance to create retirement income great diminishes the sequence of returns risk.

If you'd like to explore how this strategy might work for you, please reach out to us.

Brandon,

Would it be correct to expect that a blended whole life policy employed similarly would look much like the static 2% example? (since the cash value of the policy would continue to grow at the (relatively) static percentage rate of the nonguaranrteed dividend (~2-3%) during the time that the annual $50K is being removed?)

Thanks,

Greg

Hi Greg,

Yes and this is an important, although somewhat subtle, point. Because whole life insurance (and in many respect indexed universal life insurance) has little variability in return year (for whole life) or at least no negative return (for indexed universal life insurance if employed correctly) the sequence of returns risk exposure is greatly minimized (though not completely eradicated) so the predictability of future income has much higher confidence. This will always be true of savings plans or investment plans that have lower volatility in year over year returns.