You can find the latest Whole Life Insurance Dividend Analysis here.

In 2013 we released the industry’s first public analysis on variation in dividends for major participating whole life insurance products. This analysis focuses on variation and trend of declared dividend interest rate at the seven most competitive life insurers who issue participating whole life and will publicly announce/disclose their dividend interest rate (more on this point later on).

We’ve long argued that this sort of analysis is the best gauge of potential cash value performance in a whole life policy because it allows us to review how the company has managed business and investment operations given the axiomatic assumption that these life insurers will move heaven and earth to deliver the highest dividend award to participating policyholders. This foundational assumption has substantiating legal precedents.

Comparing Dividend Interest Rate among Carriers, A Foolish Mistake

Both laymen and some industry professionals make the cringeworthy misstep of comparing the dividend interest rate of one company to another. Since there is no exact standard to dividend interest rate reporting (i.e. is it gross or net?) and since the basis off which the insurers pays this rate is proprietary information unique to the individual policy such a comparison is useless in the pursuit of making any discernible conclusion about the how good or bad one rate is.

Also egregious is the tendency to use multi-year average dividend interest rates compared across insurers as if this means anything à la the insinuation that a company with a higher average dividend interest rate over the course of several decades must be better than one with a lower rate for the same time period.

Variation: a better Measure

We can’t compare the specific dividend interest rates across life insurers, but we can compare how they move over time. We do this by measuring the year over year movement of the dividend interest rate over a certain period of time and compare the variation results. Our favored time period is 10 years because it’s a large enough sample size of give us adequate data, but not so long a time span to be seriously outdated (though by the 10th year we’re certainly pushing relevancy a bit).

The Approach

We calculate the standard deviation of declared dividend interest rates over the 10 year sample period and compare is across several life insurers to see how has varied the most and least. Lower standard deviation indicates an insurer that has been more consistent with dividend payments, but we should note that this measure could lead us astray if an insurer were to achieve significant operational and investment performance allowing it to dramatically increase the dividend interest rate over the sample period. To control this possible problem we also calculate the 10 year compound annual growth rate for the dividend interest rate.

Doing this allows us to determine if a high standard deviation is a good or bad thing. In the case of a flat or positive compound annual growth rate, a high standard deviation is likely a good thing. If the compound annual growth rate is negative, this is bad news.

The Results

The results are found in these tables:

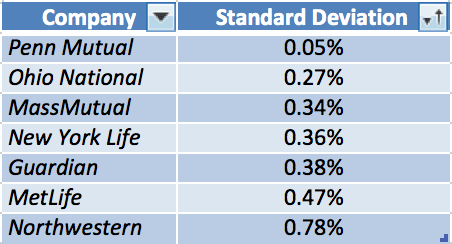

Standard Deviation

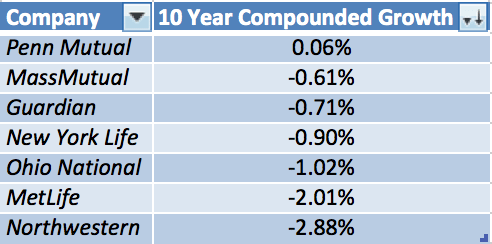

10 Year Compound Annual Growth Rate

The average standard deviation was 0.38%. One company did considerably better Penn Mutual and one considerably worse Northwestern Mutual.

The average compound annual growth rate was -1.15% and again Penn Mutual did considerably better with Northwestern Mutual doing considerably worse. These results are very similar to the analysis the last time we did it.

Some insurers improved while others have not. Notably Northwestern Mutual remains the laggard of the group with the highest degree of deviation and the most negative growth in dividend interest rate over the last 10 year period with MetLife also substantially lagging. Ohio National achieved the greatest improvement with a reduction in deviation and improved 10 year growth vs. two years ago. Penn Mutual continues its impressive run with the lowest deviation, but a strong drop in 10 year growth vs. two years ago, the company still remains the only insurer with a 10 year positive growth rate.

Wow, do I feel smart owning Penn Mutual whole life now!

Good analysis, but did you look into what it took to support those dividends? Meaning, what percentage of current income was used to support those rates over time? If you look closer at Penn Mutual’s numbers they are sacrificing surplus growth to support their dividend. If you look at their financials from last year they paid out over 300% of current income in dividend. Compare that to the major mutuals who paid between 68% and 97% of current income to support their dividends. Penn Mutual may look good on paper, but their $41,000,000 in whole life dividends paid as a company is minuscule compared to their competition. I think Guardian paid out about $800,000,000 in dividends last year using only 68% of their earnings to do so? Mass Mutual paid out over a billion in dividends using about 97% of their earnings…

My point, what Penn Mutual is doing is not sustainable. They may look good now, but back out the surplus note they took on and take a hard look at their income and they aren’t even close financially to the big 4.

Hi InTheKnow,

I actually know a lot about all companies’ financial backgrounds and I’m quite familiar with Penn’s as well as every company in this analysis.

You’ve made some errors in your claims. Since the term “current income” is not an official one it’s hard to know exactly what income number you are referencing, but I suspect I know what you were attempting to reference.

It’s unlikely you meant net income since all of them have dividend payouts that exceed their net income (that would make perfect accounting sense).

I suppose instead this reference was to earnings before dividends. You are partially correct. It’s true that Penn did have a year when dividends paid exceeded earnings before income, but this wasn’t last year, it was the year before that. Last years dividend payment was just a hair under 61% of earnings before dividends.

There is something else about Penn that you are ignoring. They (as well as MassMutual) have significant non-insurance related income that can certainly help make up differences in P&L elsewhere.

Your comment about the total dividend payout is meaningless. It’s almost likely suggesting I move to Detroit, MI instead of living in my hometown because Detroit spends more money on municipal services–I assure you despite this the town I live in is much nicer.

All of these companies have outstanding surplus notes. Surplus notes are very much a regular part of doing business for a mutual life insurer.

Your last statement about not being even close financially to the “big 4” (which if we’re using your weird metric of inclusion should be more the big 3 since Guardian is much much smaller “financially” than the other three) teeters on ad hominem. An insurer can earn less gross revenue, manage fewer assets and still deliver more value to policyholders. If bigger were always better, New York Life would win across the board, and this is certainly not the case.

The fact that the author mentions that dividend calculations are not standardized and therefore not useful in determining value, yet goes on to highlight “good” vs. “bad” companies using the standard deviation of each company’s dividend doesn’t make sense.

Internal Rate of Return (IRR) is the only true measure of performance as it nets out cost which levels the playing field (meaning the author is correct in his statement that every company uses their unique, proprietary dividend calculation which then makes it difficult to compare). IRR is the true return a policy holder earns net of all commissions, cost of insurance, etc.

Ironically, when you look at IRR, Penn Mutual drops to the bottom of the pack. LIMRA (3rd party company that is not bias towards any one company) recently came out with a study that reflects the 20 and 30 year IRR results for leading companies within the industry.

If you find the report you’ll see that Penn Mutual’s IRR doesn’t fare well relative to other companies.

Hi Dave,

Why does it not make sense? The point of such a comparison is to remove the fact that there’s no uniformity and therefore the numbers do not represent the same thing across the board.

I don’t disagree that internal rate of return on cash value is a useful comparison tool, but there’s far too much variance in terms of product type, risk class, etc. to make a meaningful comparison across carriers from a historical perspective. This is the reason the NAIC encouraged (and state regulators all came to agree) dropping such reporting from statutory reporting requirements, which happened back in the early 90’s.

Roger Blease attempted to replicate the report AM Best generated from this data but was held somewhat hostage to whatever data insurance companies felt like giving him. If they gave him anything at all.

We have tons of historical data on policies from all kinds of insurance companies but since we don’t have a common denominator among them, we aren’t going to publish any results claiming one has performed exceedingly better than another. For what it’s worth (since you named them publicly) Penn Mutual has tended to look quite impressive within our compilation of historical policy performance.

I find it interesting that someone would make an anonymous post quoting a supposed study but then decides not to provide an actual source to verify what he reports. LIMRA is a marketing research association and does not generally perform research in the capacity of product performance of any kind. Unless you can actually produce a report and give us a link to it in its entirety to review, I find your claims highly suspect.