I’ll be honest with you—writing this makes me feel a bit like Jack Nicholson’s character in the movie “A Few Good Men.” In the most memorable scene of the movie, Tom Cruise demands the truth, and Nicholson replies, “You can’t handle the truth!”

So, what in the heck does that have to do with average annual rates of return vs. compound annual growth rates, and why should you care about them, anyways?

I know it all sounds like a bunch of investment industry jargon, but hang with me here because this stuff matters.

One of the biggest secrets within the investment industry is that mutual funds, variable annuities, and countless other products tied to the whim and movement of the stock market advertise their average return numbers in a very misleading way. What’s worse is that they’re not breaking any laws by doing it.

Having been in the financial services industry since 2000, I’ve noticed that almost all investment product companies (mutual funds, ETFs, stock market indices, variable annuities, etc.) love to cite their “average annual rate of return” figures and always inflate what the particular investment actually returned to its investor.

Does this bother you as much as it bothers me?

2+2 always equals 4…except on Wall St.

This problem isn’t complicated or even nuanced (as the investment industry would have you believe) – it really comes down to basic math.

Average annual return, as it it’s described in investment literature (marketing pieces, prospectuses, etc.), is a deliberate shell game meant to confuse your perception of the actual returns by stating simple arithmetic mean calculations.

So, where’s the confusion?

The clincher is that the only return that matters is the compound annual growth rate (CAGR).

Now, I know it sounds like I’m splitting hairs, but hang with me through an example and you’ll understand my beef.

Here’s a little story to illustrate my point:

Let’s say that Bill invests $100,000 in his investment account at J.T. Marlin (Boiler Room, anyone?), and for the first year, his account grows by 25%, but the account shrinks by 25% the second year.

Those wild and crazy guys who do the math for Wall Street would say your average return is 0%. They’d be telling the truth in the same vein as President Clinton when he swore he “did not have sex with that woman.”

That is, they are clouding the truth with nonsense.

How’s that, you ask?

Keep Your Eye On the Ball

Because, your average rate of return doesn’t matter.

Here’s the proof

Year 1— $100,000 x 25% = $125,000

Year 2— $125,000 x (-25%) = $93,750

If Bill started with 100k and his account is worth $93,750 at the end of year two, his actual compound annual growth rate (CAGR) was -6.25%.

But hey, didn’t I prove in the example that his average annual rate of return was 0%?

I sure did.

So, how can Bill have less money than what he started with?

Welcome to the Wonderful World of Investments and the Imagineers of Wall St.

It’s all a matter of using the “right” words. I found this little tidbit on Investopedia.com when looking around to see what others were saying as regards CAGR (compound annual growth rate):

“CAGR isn’t the actual return in reality. It’s an imaginary number that describes the rate at which an investment would have grown if it grew at a steady rate. You can think of CAGR as a way to smooth out the returns.”

Honestly, I’m speechless. The Enron accountants have obviously taken up residence on Wall Street and are firmly rooted in content publishing for Investopedia.

I beg to differ, Investopedia…

Your real return is the only kind of return that matters. What’s imaginary is the percentage Bill’s account averaged – that would be 0% – over the last two years (see above)! Who cares if I “averaged” 0% over the last two years if my stack of Benjamins is shorter than it was when I started?

That’s the kind of dirty trick that would get you killed anywhere but Wall Street.

So, why would the investment world always quote the average return numbers? Because, average annual returns often look better than actual, real returns. If you look at Bill’s actual return over the two years, he’s down -6.25%.

If you go over to moneychimp.com, they have a neat tool that lets you look at the numbers as they really are. You can play with different time frames, adjust for inflation, etc.

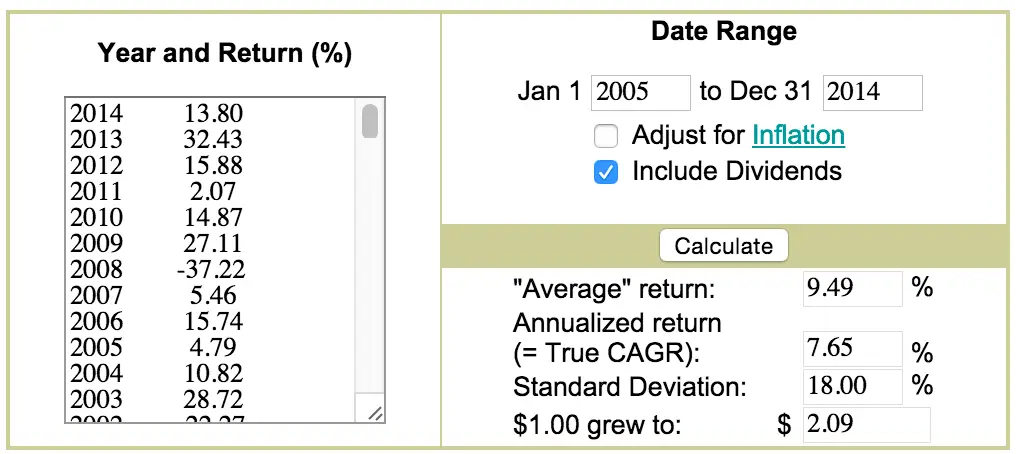

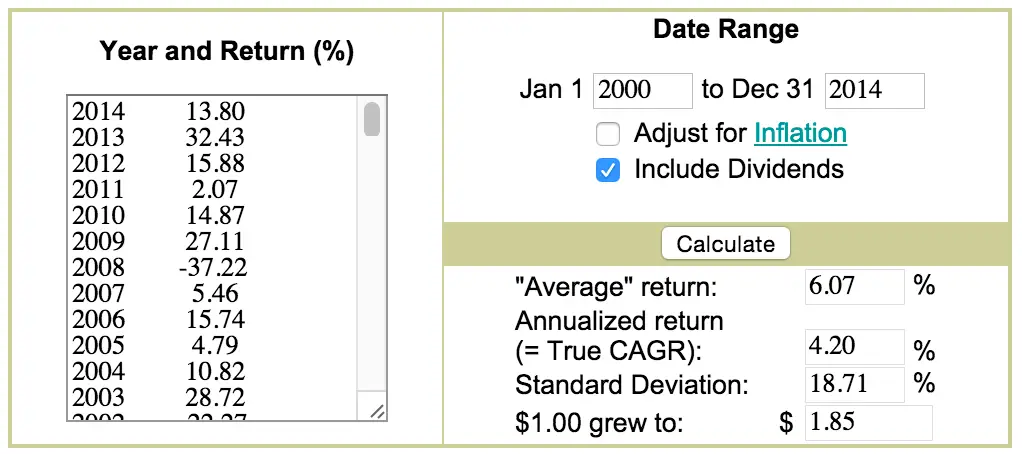

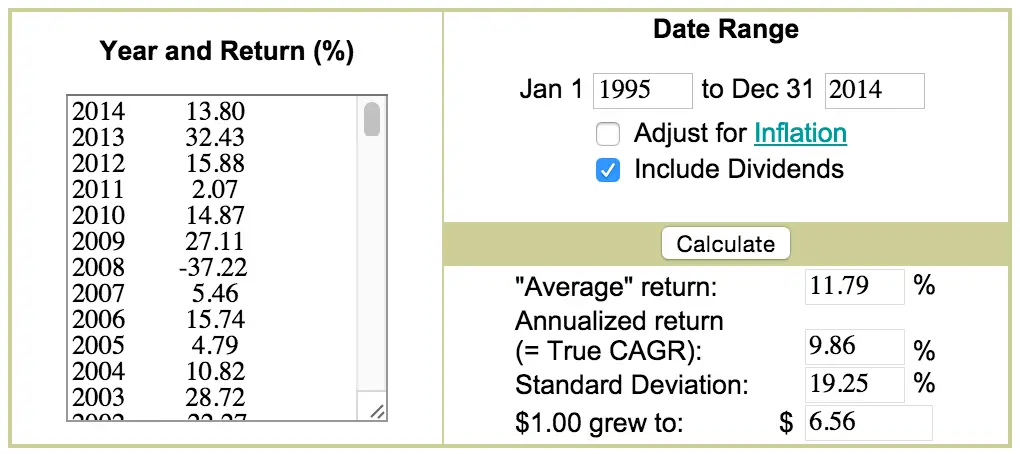

To give you a little shortcut, I’ve taken a few screenshots to show you the difference between actual return (CAGR) vs. average annual return over the last 10, 15, and 20 years.

10 year averages

15 year averages

20 year averages

The fact is that most stock market investments are volatile, and showing you the average return (arithmetic mean) makes them more attractive. Just look back at the pictures!

They speak for themselves.

What makes the average return so misleading is that there have actually been periods of time in the market where the “average return” is positive but the actual return on your money was negative.

Who cares what the average is?

It’s like talking about a company’s gross revenue. If you own a share of XYZ corporation, the only number that matters is net profit. Who cares if the company’s earnings were $1.25 per share but the net profit to shareholders was a penny?

Here’s a great quote from “The Essays of Warren Buffett: Lessons for Corporate America“:

Over the years, Charlie and I have observed many accounting-based frauds of staggering size. Few of the perpetrators have been punished; many have not even been censured. It has been far safer to steal large sums with a pen than small sums with a gun.

Take to heart what Buffett is saying in this quote – it applies here.

What’s even crazier about this whole situation is that I think the majority of people who perpetuate this lie have no idea they’re doing anything wrong!

The calculations ignoring compound annual growth rate are so embedded into the corporate culture that even advisors, financial planners, investment advisers, and other financial professionals spout off the numbers without questioning their validity.

I can’t say they are being deliberately dishonest, but I can say that most are ignorant of the facts, although I’m not sure which is worse.

My advice is to do the math or work with someone that can competently show you the math. And then…ask lots of questions.

Only then can you be confident that you’ve made a wise decision.

If you have questions about whether or not we could you protect your retirement savings from this legalized shell game, you owe it to yourself to take the next step.

With that said, I would like to invite you to arrange a no pressure whatsoever conversation.

This is a casual conversation conducted over the phone where we get to know a little about you, where you are in life, and what your trying to achieve. Don’t worry – it will NOT be a long, drawn-out pry session. It typically takes no more than 20 minutes.

From this brief conversation, we will have an idea of whether we can help you achieve your life dreams, and you will have a better idea of who we are and what we’re all about. Then, we’ll spend our time crunching the numbers for you, email them to you, and answer any questions you might have.

After that, if you feel we are good fit, we will work to design a strategy to help you keep what you’ve earned protected from the market and from the greasy hands of Uncle Sam.

The decision is totally up to you.

Here’s that link once more to book some time on our calendar.