The National Institute on Retirement Security released data during the first quarter of this year looking at how American’s view retirement and specifically retirement preparedness (or the lack thereof).

The outlook is grim. The 36 page report, which you can download here, details an array of charts that echo a constant message, “Americans believe there is a retirement crisis.”

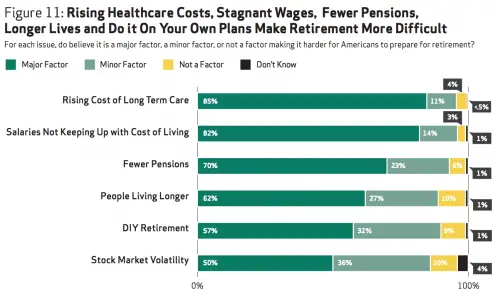

But one of the most interesting charts in the entire report—at least to me—reported on major factors “making it harder for Americans to prepare for retirement.”

One would assume the usual suspects would come up: lack of pensions, stagnant wages, stock market volatility, etc. All three items did come up, but none of them took the top spot. That position…it turns out…goes to the rising cost of long term care.

$205 per day…

According to LongTermCare.gov the average cost of a semi-private nursing home room is $205 per day. Times 365 days means the average cost of a semi-private room is $74,825 per year. What’s worse, this statistic is now five years old.

I can speak from experience when pointing out that the subject of long term care is top or near top of mind for a lot of people. This subject comes up in conversations we have with people about insurance/financial planning…A LOT.

Here’s the chart from the NIRS report:

Preparing for Life when it doesn’t go as Planned

The worry over long term care costs is complex. It’s natural to assume this means one’s own worry over the costs he or she will incur if in need of the care. But it’s a tad remiss to ignore the possibility that this worry also stems from concerns over aging parents and the financial strain they could place on a child who springs to pay the bill on the behalf of mom and dad.

I’ll go ahead and make some strong assumptions and infer that a lot of this worry likely originates from the sideline observance of a friend or loved one who encountered the expense of long term care and the ensuing aftermath.

There’s an Insurance for that

The insurance industry has attempted to tackle the subject of long term care costs. While it certainly hasn’t been a perfect answer, it’s one of the best ones we collectively have.

A 60 year old male in average health can address the problem of affording the above-referenced semi-private room (or many other possible expenses related to aging and failing independence) for about $5,000-$6,000 per year in premiums (possibly less with a few sacrifices in various benefits).

That’s not insignificant money to throw at a problem, but one year in the average long term care facility recoups every dollar paid in premiums for 12 years.

A Problem that isn’t likely to go away

Like it or not, you will age and aging comes with the probability of higher health and general living expenses related to your health and independence. Factoring this into your retirement plan unleashes a whole new set of despair, I’m well aware, but hedging the problem is certainly not out of reach.

We predict this problem will continue to keep American up at night, but it doesn’t necessarily have to.

Additionally, standard long term care insurance isn’t the only tool one has to prepare for this problem. The insurance industry continues to innovate and has brought several new products to market in last several years. If you’d like to know more about them, or standard long term care policies, feel free to reach out to us.