For the conservative savers out there who have found frustration in plummeting certificate of deposit rates, we have an alternative savings strategy you’ll likely want to know about.

For years the insurance industry has manufactured an annuity product that functions similarly to CD’s and, for the right person, this product is often favored for its superior interest rate.

It’s a rather boring annuity product, however, with lower commission rates than most of the annuities you’ll hear your financial advisor or local insurance agent pitch. No wonder this product may be flying under your radar.

An Annuity Product well worth the Consideration

The products are known as Multi Year Guaranteed Annuities (aka MYGA’s) and they closely (but certainly not identically) mimic the functional working of your standard bank CD.

Unlike fixed floating rate annuities, fixed indexed annuities, or variable annuities, these products offer a fixed guaranteed interest rate over a relatively short surrender charge period. This means your money isn’t locked up by a surrender charge for nearly as long as would be the case with most annuity products and the interest rate paid on these products is substantial when compared to CD alternatives.

The annuities have a guaranteed rate period that usually also matches the surrender period–the length of time one must keep his or her money in the contract to avoid paying an “early cancellation” fee.

The longer the guaranteed period chosen, the higher the annual interest rate on cash values.

MYGA vs. CD Interest Rate

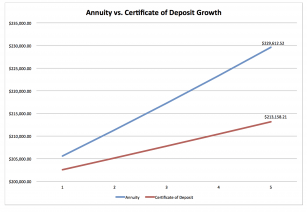

Using data from an annuity spreadsheeting tool I have access to and data provided from Bankrate, let’s compare a five-year multi year guaranteed annuity to a five-year certificate of deposit.

According to the spreadsheet (and additional fact checking with the issuing company) one can purchase a five-year MYGA from a very highly rated insurance company that pays annual interest on cash value of 2.8%. Bankrate tells me the current average interest rate paid on a five-year CD is 1.71% (as of the last week of September 2015).

It’s already obvious that placing money into the MYGA at 2.8% per year will net more money at the end of five years than the CD at 1.71%, but there are additional features to annuities that make returns far better.

Unless the CD is placed inside an IRA, interest is realized as ordinary income in the year the interest is earned by the depositor of the account. Annuities, on the other hand, defer tax liability until money is withdrawn from the annuity contract. The deferral of taxes means you keep more money each year and can continue to compound interest on a larger sum of money because you don’t have to pay taxes on a portion of interest earnings.

Consider the following example:

If we were deciding between placing $200,000 into a CD for the next five years or instead into a MYGA, we have the following results assuming the interest rates above for a non IRA situation where our marginal tax rate of 25% paid on ordinary income.

The annuity has $16,454.32 more than the CD. The annuity also comes with a host of additional benefits including:

The annuity has $16,454.32 more than the CD. The annuity also comes with a host of additional benefits including:

- The ability to continue deferring taxes by rolling the cash into another annuity via the 1035 exchange provision and continuing to earn interest in a new annuity

- A financial product that can bypass probate and send proceeds directly to named beneficiaries (this also means the payment of proceeds will not become public record as would be the case in the probate process)

- An option to turn the annuity into a guaranteed income stream for as long as the individual chooses

- The ability to further defer/mitigate income taxes through the exclusion ratio if a guaranteed income is initiated

- Protection against creditor claims in states where such protections are offered to annuity holders

There are drawbacks to annuities versus certificates of deposit that should also be carefully considered.

Annuities, unlike CD’s all generally have surrender charges which is a deduction from cash proceeds if the contract is cancelled during a specified period of time (in the example above within the first five years).

Surrender charges are assessed as a percentage of cash values and can result in the contract holder walking away with less money than was originally placed into the contract if cancelled in the first year or even first couple of years. It’s worth remembering that MYGA’s come in different guaranteed periods and often times one can get a better or matching interest rate on a MYGA vs. a CD when the MYGA has a shorter guaranteed period.

Some annuities also incur an additional adjustment to cash values upon surrender known as market value adjustment. This adjustment reduces the cash value in the contract when interest rates have increased over a certain time period and increases cash value in the contract when interest rates have decreased. Market value adjustments are only effective during the surrender period of the contract (again in the case above the first five years).

Annuities are not FDIC, NCUA, or SPIC insured and the interest rates and resulting cash values are subject to the claims paying abilities of the insurance company that issues the contract.

While it is true that life insurers must follow pretty strict guidelines regarding the assets they hold to guarantee contract promises, we highly recommend annuity purchases only from carriers that hold AM Best credit ratings of A- or better.

Additionally, the regulatory powers that be would most likely like us to point out that annuities are not deposits nor are they issued by depository institutions. Contracts are issued by insurance companies and the payment you make is legally considered a premium payment to the insurance company (though functionally that premium payment will immediately be cash value in the contract in most cases).

Not for Everyone, but Certainly for Someone

For those looking for higher returns than they are getting in CD’s who have a low likelihood of needing the money during the guaranteed period or for those who are interested in a similar interest rate with a shorter number of years holding up the money, multi year guaranteed annuities can be a great option for your money.

Superlative insurance companies are strongly encouraged as this is the best way to ensure the safety of your money. And keep in mind annuities afford several unique benefits CD’s do not that can further augment rate of return as well as save you time and money on other financial planning aspects.