Podcast: Play in new window | Download

In episode 75 of the Financial Procast:

- Hartford wants to buy back old fixed annuity contracts

- The National Women's Law Center says Long Term Care insurance is covered by PPACA

- Advisors whine about their clients not giving referrals

- Changes you can expect for 2013 tax return

Hartford wants to buy back old fixed annuity contract

In an announcement recently, the Hartford Financial Services Group offered to buy back some of its legacy fixed annuity business.

This is not new territory for the company as back in 2012 they offered to buy back some it variable annuity business from clients who had contracts with enhanced living benefit riders. Those features raise the potential income benefit payments over time in spite of market performance.

In other words, features the company now deems to be too costly for them to keep on the books.

Now, the Hartford would like to buy back fixed annuity contracts. Estimates say that some 90,000 contracts will be affected in the offer. Most contract holders that are being offered a buyout are holding onto fixed annuities that have guaranteed minimum interest rates of 3%.

The National Women's Law Center says LTC insurance covered by PPACA

It seems the cascade of “unintended consequences” is beginning for PPACA (aka Obamacare).

A nonprofit legal organization that represents women's interests has filed complaints with Health and Human Services, as well as, the Office for Civil Rights. The complaints claim that charging women more for private long-term care insurance violates section 1557 of the Patient Protection and Affordable Care Act (PPACA).

Insurers have always claimed that women have higher costs associated with long term care due to their longevity. The insurance companies argue that LTCi is not covered by PPACA as it's not major medical insurance.

PPACA Section 1557 states:

An individual shall not be excluded from participation in, be denied the benefits of, or be subjected to discrimination under, any health program or activity, any part of which is receiving federal financial assistance, including credits, subsidies, or contracts of insurance, or under any program or activity that is administered by an executive agency or any entity established under this title (or amendments).

Since many LTCi contracts provide “partnership” programs with the states (they coordinate with Medicaid nursing home benefits), there may be a case here. Only time will tell.

Remember when then speaker Pelosi said, “But we have to pass the bill so that you can find out what is in it, away from the fog of the controversy.”

Well, the bill is passed–the fog…not so much.

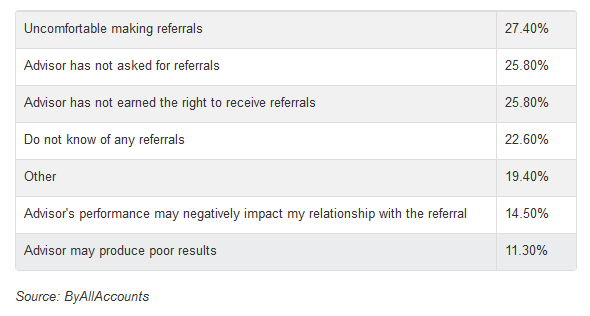

Advisors whine about their clients not giving referrals

Research conducted in a survey from ByAllAccounts shows that less than 50% of respondents have given referrals to their financial advisor.

Here's a chart of their results

Changes you can expect for 2013 tax return

There are quite a few changes to look out for in your 2013 tax return. We discuss each one in detail.

Here's a list to make note of:

1. Additional Medicare Tax

2. Changes in the Net Investment Income Tax

3. Tax rates change–top bracket is now 39.6%

4. Tax rate change on capital gains

5. Must be 10% or more of AGI to deduct medical expenses

6. Increased personal exemption (by $100)

7. Increased limit on itemized deductions

8. Rules on same sex marriage filing status

9. Change in home office deduction