Podcast: Play in new window | Download

We are exhuming the body of the Retirement Income horse. Yeah, we figured we haven't quite beaten this horse enough, so we're gonna dig him up and beat on him some more. This is all metaphor of course, we don't have any real hatred of horses or any other animals for that matter.

Recently, in my quest to bring our audience ever relevant information in our weekly podcast, I stumbled upon a Forbes article written by Rob Russell that cites a Morningstar report from earlier in 2013 that caught my eye.

The data from Morningstar suggests that the proverbial 4% withdrawal rate of your retirement portfolio, may not work so well after all.

Sequence Matters

For those of us who've been talking about this for a number of years, it's always nice to see further validation of the realities as they exist. The afformentioned report brings it's hypothesis to the fore in it's opening paragraph:

Bond yields today are well below historical averages. This has significant implications because portfolio returns in the earliest years of retirement have a larger impact on the likelihood that a retirement income strategy will succeed than returns later in retirement. The majority of research on sustainable withdrawal strategies has used a stochastic (Monte Carlo) simulation process based on long-term averages, where the expected return of an asset class is the same for each year of the simulation. While this approach is reasonable when markets are near long-term averages, we believe it is less useful when there is a significant and sustained deviation such as the current low bond yield market.

There's the rub.

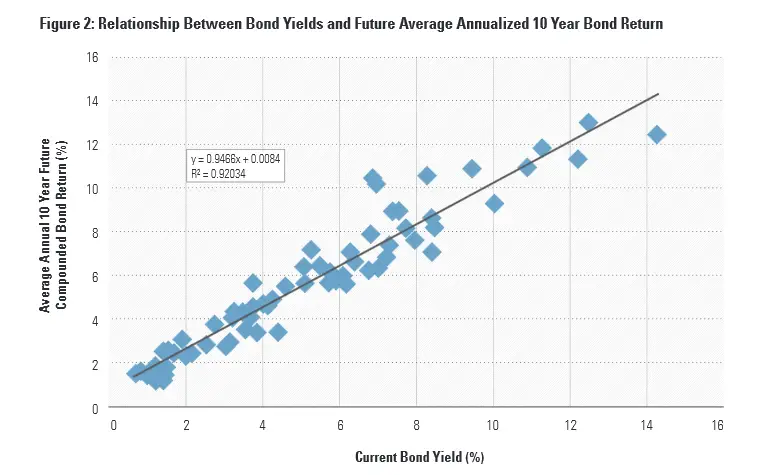

To further illustrate the problem, take a look at this chart (credit the Morningstar report once again for this)

Are you still with me? I hope so.

I know it all seems overwhelmingly technical and slightly boring, however, there's an important takeaway from Figure 2. There is a direct correlation between bond yields in the present and what one can expect as an annual average return in the future.

So, this means (according the research and illustrated in figure 2 above) that “the current yield on bonds can describe 92.03% of the average annual 10 year future compounded bond total return.”

Ouch. That puts a significant dent in the assumed rate of return for a bond portfolio going forward. Consider this, according to the Ibbotson Intermediate Term Government Bond Index the average annual return from 1930 to 2011 was 5.5%.

The research from Morningstar shows us that over the next 10 years we can expect about 1.8%. That's nearly 400 basis points lower.

What sort of impact do you think that will have on a 50/50 portfolio of equities and bonds? Especially if you're starting your retirement income withdrawals today. Assume for a minute that your retirement income simulations assume a 5.5% return on the bond portion of your portfolio in the first year. Now, consider that the current intermediate term government bond portfolio yields about half that today.

You're starting off your very first year behind–the returns were grossly overestimated. Whatever your projections were–they're now wrong. And because the power of compounding can work for you or work against you, your assumptions will be impacted geometrically. In other words, your probability of failure goes from 10% to about 50%.

I've shortcut some of the finer points here but I figured you'd all appreciate that after the opening.

How Do We Fix It?

Save more, then double down.

It doesn't do much good to point out all the problems without providing a solution…right? And I'm guessing none of our audience can guess what we'd suggest would be the solution.

Sidebar: If you're new to our site, we welcome you and suggest you spend some reading some of our 300+ other posts. You'll quickly discover what we like as a solution.

A properly designed cash value life insurance policy would certainly help with the retirement income problem. Actually, that along with a clever use of certain types of annuities can provide a great deal of certainty during your retirement. And as far as we're concerned certainty trumps all when you're now dependent on your pot o'money to generate an income for you.

If you'd like to see how our strategy might work for you, contact us.