Whole life insurance dividend changes often happen once per year and we generally get excited near the end of the year when most companies announce these changes. We’ve been tracking and announcing changes when they become available for the past several years and will continue to do so in the future.

The anticipation for the announcement of the following year’s dividend focuses mostly around evaluating how well an insurance company is doing—especially with its block of participating life insurance—and how these results affect the dividend interest rate. We don’t get a lot of under-the-hood information about whole life insurance, so any metric we can use to look at how things are going is always appreciated, and dividend interest rates are one of those metrics.

The Dividend Interest Rate and how it Changes

The dividend interest rate is the portion of the dividend that investment income supports. Keep in mind that there are two other factors that go into the dividend payout (claims experience and expense). Since there is no hard standard across the industry regarding dividend rates and how a dividend is ultimately calculated on a policy, we can’t compare one company’s rate to another to make any evaluation of how the two stack up against one another. What we can do, however, is look at where the quoted dividend rate is going and make assumptions about how well the company is managing in prevailing economic conditions.

Looking at how dividend rates change over time for a specific company tells us if they are generally pulling more or less profits from some degree of their operations on a per policyholder basis. Additionally, it gives some insight into the relative increase in benefits current policyholders are enjoying (or not enjoying) by having purchased a policy from any specific insurance company.

Our Review: Methodology

We’ve calculated the per year change in dividend rates over a 10 year period for several life insurers using their stated dividend rates on current blocks of whole life insurance business. Some companies are still issuing whole life insurance policies and some are not. This is done with a simply regression using time as a explanatory variable. We’re not so much interested in the explanatory powers of regression analysis here as we are in simply identifying a trend—i.e. has the dividend increases or decreased each year and to what degree?

We did not exhaustively test results for compliance with required assumptions under ordinary least squares as the predictive precision associated with such rigor isn’t necessary in this case.

General Trend Down, but to Largely Varying Degrees

Not surprisingly the generalized trend for dividend rates has been down. Interest rates having slid for several years and still remaining low forces a tough investment environment for several life insurers.

However, not all companies are down for the past 10 years, and there is a wide variance in the degree of how much a life insurer has lost in dividend interest rate over the last 10 years. Some are only slightly negative having lost a few one-hundredths of a percentage point. While others have been shedding nearly a quarter of a percentage point each year for the past 10 years.

This spread in the negative territory is interesting and cause for some careful consideration when further evaluating some life insurers on the list.

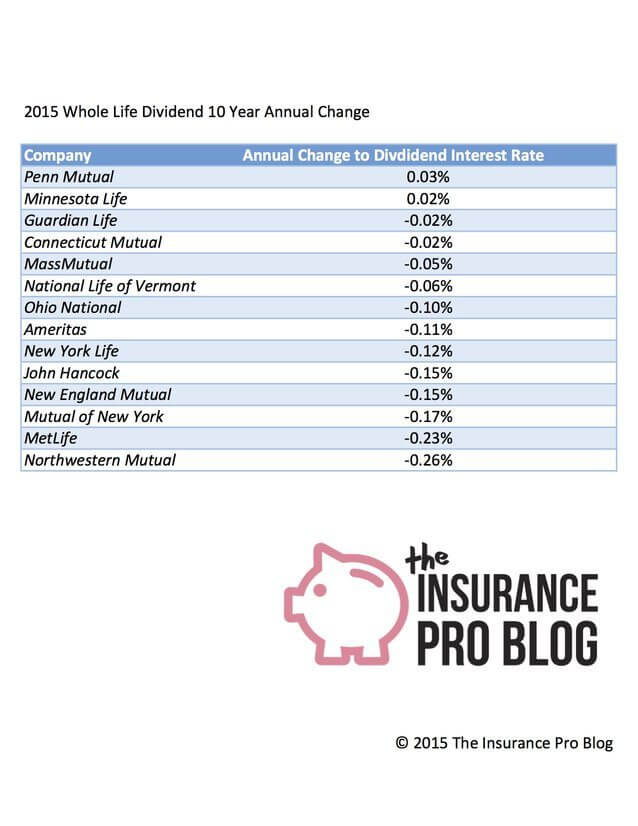

Historical Dividend Change: The Results

Here’s the chart that ranks each company by its per year change in dividend rate (click to enlarge):

![]()

![]()

We have two companies showing impressive results having effectively increased their dividend rates each year over the last 10 years. And while those increases may be modest, the industry trend would suggest those modest increases are quite praise worthy.

It’s also interesting to see that four companies on the list no longer issue whole life insurance policies, but they none of them rank at the bottom for annual changes in their dividend rate.

Limitations of this Analysis

Just as I mentioned numerous times in past articles that evaluate various metrics about insurance companies and their products, this is one angle of a very complex consideration and is by no means a definitive ranking of insurance companies or their products. There are far more considerations to ponder when selecting an insurance company.

One should look at numerous facets of life insurer’s product offerings and operational successes or failures to determine what company and product is best for his or her specific needs.