Indexed Universal Life Insurance is well-known for its ability to generate a retirement income stream, but how can you tell a good product from a bad one?

Most attempts to compare company products fail to find a solid basis for comparison or are foiled by marketing gimmicks.

Where Others Have Failed

The problem with most indexed universal life comparisons is that too much variation is allowed across carriers. All carriers have a defaulted interest rate for their various indexing strategies, and these are loosely based on the cap and participation rates stipulated in the policy.

While this may make some intuitive sense, the logical mechanics behind indexed universal life would suggest that, with the exception of some very specific situations, all indexed universal life contracts will yield more or less the same.

Again, this doesn’t mean we should completely ignore specific variations among carriers when it comes to current cap rates (participation rates are mostly the same).

We can still control a macro evaluation of expenses if we assume the same credited interest rate. Whether or not the additional cap rates justify the additional expenses is part of a fine-tuning process of selecting the best contract for a given situation.

So, failure number one is the lack of a universally assumed interest rate.

Death Benefit Assumptions

While this isn’t a universal problem, it is a prevalent one. For income comparison purposes, death benefit should be solved to minimum non-MEC and use the Guideline Premium Test to qualify as life insurance in compliance with DEFRA.

Some comparisons have specified premiums and solved the death benefit to the “target premium” – bad idea.

Maximum income is our goal. As such, we want the minimum death benefit in order to mitigate insurance costs as much as possible and build the best-performing universal life contract.

Preferred Best Assumptions

More important than comparing companies with each other is choosing among scenario comparisons for an individual who wants to apply for life insurance.

Most comparisons (including those run by the life insurance companies themselves) assume best-case scenarios with a preferred plus (best) risk class.

The truth is, most carriers issue a large portion of their policies as standard, and that’s where most assumptions should start.

It is true that this life insurance as an asset class thing gets better the healthier one happens to be – longer life expectancy begets lower insurance costs – so again, better risk classes are one of the fine tuning considerations.

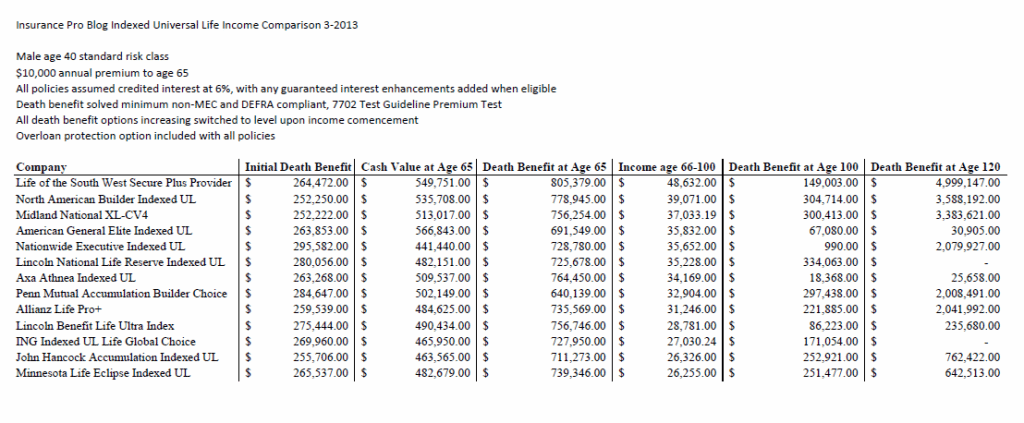

The Comparison

Our comparison takes a 40-year-old male standard-issue placing $10,000 annually into an indexed universal life contract for 25 years.

After 25 years, he begins an income stream until he reaches age 100 (years 26 to 60).

We solve the death benefit for minimum non-MEC and DEFRA compliance, increasing until the year income starts, at which point we switch the death benefit option to level.

The only rider we’ve included is the over-loan protection rider (sometimes, this is not a selectable rider but rather a built in feature; regardless, it’s included with all policies compared).

We’ve sorted the results by income derived.

What the Results Tell Us

While it’s tempting to draw definitive conclusions about who has the best product and who doesn’t, it’s important to remember that this is a narrow evaluation of a specific circumstance.

Still, the comparison gets us started and pointing in the right direction.

There are certain less easily quantifiable considerations.

For example, Life of the Southwest (LSW) tops the chart quite impressively, but with a disappointing Comdex and a junk bond position that totals 75% of the company’s surplus position, we remain hesitant to strongly recommend them in most cases.

It’s important to keep in mind that this is merely a starting point, and further consideration of company/contract specifics is always in order.

Some Notable Omissions

Due to problems with company software, a few companies are missing from this list. We’re working on this and hope to update have an update for you once these issues are resolved.

The missing companies include Prudential, Transamerica, Pacific Life, and Aviva.

If you feel we’ve neglected someone, we'd be happy to hear from you.

The Next Step

From here, it would be prudent to evaluate such specifics as available riders, premium loads, caps, minimum guarantees, additional contract benefits/options, and company strength.

Though many agents skip it, there’s also lots of reasons to pay attention to the fixed account.

Lastly, keep death benefit performance in mind. This asset can be leveraged for more than just its potential income. Among companies with similar incomes, favor could fall to the one that performs markedly better in terms of death benefit.

In your first paragraph here, you say that an IUL is “well known for its ability to generate a retirement income stream” yet these plans have only been around for barely more than 15 years. How many people have successfully use an IUL to produce the income stream that is advertised? And in that time, how many have imploded?

The biggest thing that IULs generate is mismanaged expectations due to rosy illustrations that are nowhere near reality. Of course, this is just my opinion…

Hi Greg,

Your asking a question that has no answer as you and I both know there are no stats collected on what sort of policies work out as intended.

We could of course ask this question of any financial product and again, there’d be no answer.

There’s no doubt that there are people who do harm with IUL, just as their are people who do harm with annuities, whole life insurance, mutual funds, 401k’s, hedge funds, and the list goes on.

My issue was the use of it being “well known.” It’s not well known because it’s not proven. That’s my only point. The other products you mentioned have at least some kind of track record. IULs simply do not have that.

I have no quarrel with you…hell, I don’t even know you! I am just concerned that using such flowery language is going to bite you, and worse, your CLIENT’s ass when the plan blows out because the internals just can’t support it.

Good luck… 🙂

There’s actually no proof to substantiate the falling apart stories. Universal life insurance has more than enough track record to support its position as an income generation tool.

Greg, I agree, we have to be careful about the terms that we use when talking with clients. I, and all the other agents in my office are careful to make sure that we explain how the product works and how you can shoot yourself in the foot if you don’t follow the rules. I’ve seen 2 people in my years her that have had a bad experience with the IUL. In both instances the client had only been putting in the minimum then canceled the IUL after a couple of years. They expected to have a huge cash value, even though they were specifically shown that they IUL needs 15+ years to do what it can do, and that in order for it to be a feasible cash accumulation vehicle you had to put in the max not the minimum premium. People are always going to find bad if they look for it. They make up their minds before even going into it that something isn’t going to work, and funny enough, they will find just what they are looking for. I’ve seen it with countless deferred plans. They always want to break the rules with no consequences. As long as we fully explain what the rules and consequences are, we can do tremendous things for people.

Thank you for the useful spreadsheet comparison. I was a bit confused why I didn’t see Pac Life initially, however realize further down on your post you had issues.

Here is my view on IUL. Over fund and review annually. If you use an early cash value rider the cash value at the end of year one will be much higher than without it. Your clients will appreciate it, and liquidity won’t be much of an issue.

Insurance carriers are buying the same bonds and have access to option markets via the same investment banks. Options have been around a lot longer than Indexed Universal Life so it is fair to say Investment Banks price and know their risk. We can probably assume that option markets are efficient as well.

It comes down to how efficient the life insurance company is with their costs.

My opinion is that participation rates and caps are marketing tactics. Higher participation rates probably means higher costs. Eventually these participation rates will converge.

LSW is a wholly owned subsidiary of National Life, is there a legal wall that keeps National Life off the hook from the potential negative consequences of LSW’s junk bond holdings? Is this why you look at LSW and withhold the favorable recommendation rather than looking at the parent National Life?

Thank you both for the great work

Hi Tod,

National Life of Vermont could theoretically be involved in shifting assets to assist LSW if there was a problem, and that’s always the implied hope for subsidiaries. For example, Penn Mutual’s IUL is issued by the Penn Insurance and Annuity Company, which is a subsidiary of Penn Mutual and we’d anticipate that the mother ship looks after the subsidiary.

Hi Guys

Wondering if you are planning on running this analysis again in the next month or so; that is have the company software issues been resolved.

When you present this data again would you point out some of the comments you’ve made over the past year about each carrier. In this post you mention LSW and their junk bond position. Recently you mentioned your concerns about Aviva. These caveats are a valuable insight to consider.

Thank you again for the tremendous work and delightful presentation.

Tod

Hi Tod,

It may be a little longer than the next month before we can come back to this, but it is on the to-do list.

Regarding the next point, this is a slightly more delicate piece to navigate. We are working on a few items. More to come.

Thanks for the comments.

Sorry that last post should have been on this page….

For the income illustration.. Did you use a variable loan rate or fixed? If Var. what was the loan rate used? One other question, I am curious how LSW so far ahead of the others?

I did not see and answer to the question about which loan type was used in the analysis. Was it a fixed or variable loan?

Hi Howard,

Loans used are indexed loans.

In regard to the variable loans, what loan interest rates did you use for each product. Some company’s software uses the current rate of about 4% for the entire illustration while others use close to the maximum rate that can be charged for the entire illustration. Where the rubber meets the road is when one is taking money out of the policy and how flexible the company is in regard to loan rates as well as conversion to fixed rates or wash loans when the market is going sideways or down.

Loan interest rate was 6% unless guaranteed fixed.

I believe that the assumption of “standard” placement is an unrealistic presumption.an alternative spreadsheet should compare best class i.e. preferred plus or super preferred is more realistic for 40 year olds. furthermore all over loan protection riders are not the same. there is only 1 carrier listed that has 2 requirements to prevent the lapse all the rest have at least 3. that third being that the accrued loan and interest must exceed the face amount.

Warren,

No, quoting these at preferred or better is not more realistic. I’m not even sure what “more realistic” is supposed to mean. But feel free to elaborate.

The over-loan use and requirements to trigger is irrelevant since all income solves were set to trigger in all situations.

In reading through your comparison I believe you have a made a significant error. You “assume the same credited interest rate” in a failed attempt to control for policy expenses.

What you have actually done is to hamper the projected performance of products that are designed to provide a higher cap rate than a product that is not.

Here is a simple example. Both North American and Midland are sister companies and their products are designed by the same people. Yet North American has a 1% lower cap on it’s S&P pt to pt index strategy than Midland does. The reason is the NA policy has lower expenses in other areas of the policy than the cousin product at Midland.

What assuming the same return assumption does is penalize a product like Midland’s and favor a product like North American where certain expenses are already baked into the lower caps/participation rates.

There are two places a company can take it’s profit – lower crediting terms or direct policy expenses. What you have done is benefit all of the products that take those dollars from lower crediting terms at the expense of products that take them at the policy level.

John,

Leaving the assumed credited rates level does not fail to accomplish what I was shooting for. We have to start somewhere, and I very explicitly mentioned towards the end of the article that there are other factors to consider (and caps was on that list of considerations).

This is only one piece of a much larger puzzle, nothing in this article is laid out in a way to ignore that fact. Taking Midland and North American as an example, projected income is very close, and it makes a lot of sense to try and internalize the higher cap at Midland and consider if 1. the difference is even significant enough to assume one will truly outperform the other or if that far into the future its close enough to pretty much be the same and 2. that the higher cap at Midland might outperform based on the closeness.

So no significant error made. And further, if I was going to try and accommodate all of the different caps out there, there would be even more complaining about whether or not I allowed an adequate crediting rate for various caps. This comparison is fine, and it also leaves considerable room for margin if caps were reduced among carriers with higher caps.

Hello~ wondering when you are planning to update the comparison. Would like to see Western Reserve Life on it. Thanks.

I see you used a 6% loan rate across the board, however that’s not a realistic projection unless the carrier caps it at at 6%. The rates on most variable loan provisions are based on the Moody’s Corporate Bond Index plus a spread. Carriers like LSW who are showing 4% from day one are doing a MAJOR disservice to their policy holders by creating such unrealistic expectations, when the average Moody’s yield is over 8% since 1982. Even bumping the loan rate up to 6% isn’t an honest projection (again, unless there’s a guaranteed max cap of 6%) based off of historical averages. To do a more accurate comparison, the variable loan provision needs to be run with the 30 year Moody’s yield, plus any applicable spread – up to the guaranteed maximum loan rate – just as they’re showing 30 year lookbacks on hypothetical crediting.

No Dave you’ve forgotten that we’ve also adjusted the assumed rate of return. If we’re going to use historical data to guide the loan rate, then we’d also use historical bond assumptions to guide the assumed interest rate and we’d be around 8% there as well.

But that assumes historically high interest rates will prevail again, which is an awfully lofty assumption. Truth is 6% is a number we can use to bring parity among assumed loan interest rates across all carriers and that’s why we chose it. That being said, it’s very wrong to assert that if loan interest rates were to rise due to underlying interest rate market conditions, caps would not also rise to affect yield. These products are designed and managed to target a given interest rate and that interest rate is based on what the carrier believes it can support given market conditions, which is heavily supported by bond yields.

By bringing assumed credited interest down and bringing loan interest rates up (in most cases) these are much more realistic projections.

Actually, I have an excel of Moody’s bond yields since 1980. While we may not see 80’s interest rates, it’s also likely we’ll never see such historically low interest rates for such a prolonged period of time. The average over the last 30 years is over 8% (and that includes these ridiculously low rates for such a prolonged period). Illustrating anything less than 8% on the loan, if the loan doesn’t have a cap, is irresponsible. That’s actually why I only recommend products which have a cap (6% with NA, Lincoln, or Voya) on the variable loan rate. If there’s no cap, it needs to be illustrated with the higher loan rate or the wash loan feature.

The comparison is not even close to being an accurate depiction of the selected products. YOU CAN NOT RUN THE SAME INTEREST-RATE ON EACH PRODUCT TO COMPARE THEM. Considering that the caps on each of those products is vastly different and the participation rates are different. Your asking us to compare a Ford eco boost with a Dodge 3/4 Ton Turbo Diesel. yes they are both six cylinders yes they both have turbos, but no are they even close the same truck.

Jameson,

You can use all the CAPS you want, it doesn’t help to make your point any less ridiculous.

Reading comprehension doesn’t appear to be your strong suit, as I mentioned numerous times in this post that this is by no means a definitive answer to who is good and who is bad, and further noted that looking at other considerations was extremely important (hey look at that, I even mentioned index caps as an example).

Further, I’ll note that our use of an identical interest rate was to evaluate underlying expenses in these contracts, without arduously looking through expense ledgers. This sums up the comparison really well. No, this doesn’t suggest that LSW is the best, and no it doesn’t suggest that Minnesota is the worst. We were pretty clear about that.

There’s no need to get so indignant because your favorite carrier didn’t top the list. As I’ve suggested to others who have felt the need to spew their BS here, this is just one look at a very narrow angle of a very large picture.

I’ve been looking at life insurance as an investment and it seems advisors can’t understand that my goal is to minimize the life insurance and maximize the investment without MECing the policy.

So I looked at a VUL policy and what I looked at was comparing investing in a low cost index fund versus a VUL and after 30 years seeing at what CAGR I would need to beat the index. I assumed with the VUL I will take the money and pay tax at the 39.6% tax rate. What I came to was at a CAGR of 7% or higher I’m better off with the VUL. I looked up the history of the stock market which has a CAGR of 8.5%.

Now, since 2000, the average return of the stock market has been 4%, so for the next 16 years one would need around 12% or so to get back to that CAGR of 8.5%.

So it seems to me one needs to be pretty close to the average rate of return of the stock market to start making life insurance a better investment than life insurance. Could you comment on my thoughts.

Basically it seems to beat the stock market index one needs to have a pretty good rate of return because of the fees of the life insurance.

Hi Geoff,

This will depend a lot on the VUL used as these can vary wildly with respect to fees and expenses. This product also has issues with expenses in declining markets as it tends to increase the net amount of insurance in place, which also increases the expenses in the policy.

As far as your comment about needing returns close to the average rate of the stock market to do better than the market, I would argue there’s a good chance that you’ll need more than this when it comes to VUL, and since VUL comes with considerable risk given the likelihood you’ll be invested in the market, it often begs the question on why bother with this product. Generally speaking, it’s a coveted product when one wants to place a larger sum (beyond IRA limits et. al.) into a deferred account and maintain stock market exposure without facing the early withdrawal fees (before age 59.5) that would become a consideration for a Variable Annuity. Whether this deferral is truly worth the cost of insurance again depends a lot on the specific product chosen and it’s fees.

This only applies to Variable Universal Life Insurance and not the case for fixed forms of universal life insurance (e.g. current assumption or plain universal life insurance and indexed universal life insurance)

The most popular EIUL product has been the Omega Builder from Minnesota Life… yet you don’t even have it mentioned……

This product was distributed through an extremely limited proprietary distribution chain until just a few months ago, so it’s highly unlikely it was the most popular IUL product on the market when this post was written almost two years ago.

Further, all of Minnesota’s products combined don’t total number one in IUL sales.

I don’t really want our first conversation to involve my accusing you of product hawking on our web site, but you sure are quacking like a duck at the moment.

as a follow up, Minnesota like all other IUL carriers will shortly be limited to illustrating a lower interest rate of somewhere close to a maximum of6.85% and only wash loans for the stream of incomes generated.likewise their overloan protection rider requires that the loan plus accrued interset exceed the face amount of the contract. so large lump sum distributions in the early years will greatly diminish the likelihood that the rider will work as expected. also the reider requires that the OWNER of thepolicy notify the carrier to exercise the rider. remeber loans do not reduce the face of the policy . eventhough the software shows the lower death benefit as a net death benefit.

Hi Brandon,

Related to “Blended Whole Life” thread, following the same logic, blending IUL with Term rider will enhance income accumulation and distribution.

For income purpose, Blended IUL > IUL > Blended WL > WL ? Do you agree?

Hi Jay,

Sort of agree (but mostly disagree) on a very case-by-case circumstance.

Not because your logic is wrong in terms of what blending is supposed to accomplish. But because very few universal life carriers offer any sort of blending option, and those that do don’t often provide any sort of reduced cost benefit behind it. Whole life blending essentially turns whole life insurance into what universal life insurance already is, so blending isn’t a necessary step.

There are a very few carriers that do offer supplemental term riders to their indexed universal life policies, and in some cases these riders enhance cash values. They don’t often enhance long term cash and income though. Instead, they tend to reduce surrender charges. Which is great for liquidity purposes, but sometimes counterproductive to income goals largely since they alter expense and guarantee assumptions that require more death benefit per incoming premium dollar.

You’re on the right track though, so where it’s available, it’s worth looking at in terms of building a higher performing contract within that specific carrier’s product line up. Our comparisons have always shown that carriers that don’t offer it often still perform better.

I’m an end user as opposed to a broker. So I need a bit more education. I’m very interested in what policy factors to look at to select an IUL product. You did try to level the field by using the same interest assumptions, yet the other factors to consider were mostly lacking. What caused LSW to do so much better income wise than the others? Is it just that the LSW fees were so much lower? The only thing I am interested in is the income stream. And will you share your spreadsheet model so I can adjust for starting at age 60 not 40?

Hi Walt,

We sent an email to further assist on some of this, but I’ll also address your main question regarding LSW. How they came out ahead like they did was always a bit of a mystery to us. We sought further explanation on why this happened, but never received an adequate answer.

Subsequent comparisons have not generated the same results for LSW.

Was this ever updated with Pacific Life and I would love to see Voya as well.

thanks!

Hi Caleb,

We never revisited this comparison due to other priorities. Perhaps one day. Thanks for the request.