We’ve discussed whole life dividends a good bit at the insurance pro blog. We’ve also compared a lot of other insurance company stats in the past, and will continue to do so in the future. One such comparison is the effect a changing dividend has on projected income. This is important because it helps us determine who is the safer bet as defined as the company whose product is more reliable in the income projection side.

We’ve discussed whole life dividends a good bit at the insurance pro blog. We’ve also compared a lot of other insurance company stats in the past, and will continue to do so in the future. One such comparison is the effect a changing dividend has on projected income. This is important because it helps us determine who is the safer bet as defined as the company whose product is more reliable in the income projection side.

We live in no delusion about the fact that a policy illustration is merely a tool used to sketch the general function of the policy. It makes no promises regarding actual performance (unless we are looking at the guaranteed column). Still many, us included, use income projections to evaluate policy expenses overtime and dividend policy—remember, we can’t categorically declare non-direct recognition superior to direct recognition we have to look at specific company policy.

Income Relative to Dividend Variation

As I’ve mentioned a number of times, inferring information with statistics requires an evaluation of change. For example, we cannot declare that people who eat a lot of fat in their diet will by virtue of eating that fat become fat themselves (i.e. merely eating the fat and being fat shows a correlation, but correlation does not give us much insight into cause). If on the other hand, we measure the change in BMI given the change in consumption of various macronutrients and we find that as fat intake increases BMI increases as well we might just be on to something when it comes to suggesting that consuming fat will make you fatter.

The point then to looking at how projected income changes as the dividend interest rate assumption changes give us insight into internal mechanics and whose projections are more likely to hold true given the fact that the dividend will in fact change over time.

The Method

We took 5 whole life company products from our top whole life carriers list and ran the following scenario:

- Male age 30

- Standard Risk Class

- $20,000 premium per year

- Premiums paid to age 65

- Income withdrawal to basis and then loans from age 66 to 100

We took the initial income projections and then compared them to a 100 basis point drop in the dividend interest rate. Now, I want to be very clear about something. A drop that large to the dividend interest rate is a HUGE drop. I point that out merely to say that the scenario we’re evaluating is a pretty substantial change in the assumed dividend rate. And I also want to be clear in pointing out that this drop is assumed in all years.

We ran the illustrations non-blended. That means just base whole life policies. The major reason for this was mostly for convenience sake. It takes a lot of time to put some of these blended policies together, and we didn’t have the free time for that on this one. Additionally, I’ll note that based on what we’re comparing, the fact that these policies aren’t blended makes no difference as we’re chiefly concerned with how the change in dividend effects income. Though there are certain aspects to this that might affect some companies when it comes to a changing dividend, so we will revisit this in the future.

Instead of showing multiple products for the same carrier, we chose to only to evaluate the products that projected the highest initial income (interestingly that product at Ohio National that we’ve been pretty harsh about in the past, turned out to be their best bet in this scenario, sometimes it does work).

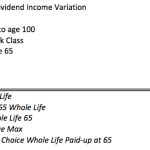

The results are as follows (click the picture to see):

Our Thoughts

It’s interesting to see MetLife has the most stable results when the dividend changes. Though there is some math at play that removes some of the mystery in awe in all this. MetLife presently has the lowest dividend interest rate of the bunch at 5.25%. Anyone who has sketched out an exponential curve knows that as the exponent increases the slope of the curve increases as well. This means, dropping 100 basis points on a lower current dividend rate should yield a smaller impact on everything as the downward shift in compounded cash accumulation growth over time is less. This would be the anticipated trend.

But that’s not what took place universally…

Interestingly, the next lowest dividend interest rate comes from Ohio National at 6%, and the drop in income there was much more dramatic than it was for three carriers with higher current dividend interest rates. It’s also worth noting that the current dividend rate at the Guardian is slightly higher than the current dividend interest rate at Penn Mutual, but the income projection there dropped at almost the same rate.

It’s also somewhat fascinating to see that net impact of such a drop significantly closes the gap in projected income between MassMutual and Penn Mutual despite the disparity in dividend interest rate, 6% to 5.34% respectively after the 100 basis point drop.

Also, it’s worth bringing up the direct recognition vs. non-direct recognition debate. The most stable result comes from MetLife, a non-direct recognition carrier. But the least stable result also comes from a non-direct recognition carrier, Ohio National. So, insight on that issue is a tad all over the place and comes back to a point we made a while ago, details matter more than simply what you call it.

Ultimately you should all take from this the fact that dividend rates can and do change from time to time and since a lot whole life for wealth accumulation or retirement income is a long ways off, trying to get a handle on accuracy is at least something to consider. Whole life dividends play a crucial role in the overall strategy, so it’s worth spending some time picking through the details.