Blended whole life is a concept we really like. We maintain that it’s the way to purchase whole life insurance if cash accumulation is your primary goal.

Anyone who has learned that you can use whole life insurance as an asset and income tool should probably also take a look at a blended policy.

If you’ve been shown a standard whole life policy (i.e., no paid-up additions and no blending used to maximize paid-up additions), we invite you to challenge the performance of that policy against what can be done with the advantages of this truly unique blended design.

Perhaps you’d first like to see some proof to back up our claims that this blending business is truly beneficial?

Never mind that anyone with a strong fundamental understanding of life insurance products will declare blending superior. It took me a while to realize that this understanding is often lost on other agents (I had assumed they merely ignored it, but that doesn’t appear to be the case).

Such a comprehensive understanding of product mechanics is all well and good, but since we can’t immediately download it into your brain à la The Matrix, how about we show you some historical evidence?

Historical evidence, you say?

I could call upon the policies that I’ve put in force, but I’m rather tight-lipped about clients and their policies.

I make a point of respecting the privacy of anyone that entrusts me with their personal information. Thankfully, finding a third party for an example is no problem. Allow me to turn your attention to the Bogleheads forum.

Bogleheads?

Yes, I mean that funny online forum frequented by people who idolize Jack Bogle.

And, while Brantley and I champion an analogous Bogle-like position within the insurance industry (i.e., there’s more money in making a lot of people really happy with superiorly designed life insurance products than in trying to suck as much money out of everyone we meet), there seems to be a dislike and distrust for life insurance over in Bogle-land.

So, when someone came along asking if anyone had mathematical evidence that buying term and investing the difference really works out better, it’s no surprise that the elder Boglers rallied to vilify that awful insurance product that pays high commissions to insurance agents.

Regretfully, several members with extraordinary post counts threw their opinions into the ring.

According to them, you should buy term and invest the difference because you’ll get 8% on stocks, and insurance products pay commissions to agents. I’m not sure how those two pieces of information constitute a mathematical proof, but if you have time to accumulate 5,000+ posts on a forum idolizing one guy, you may not have time to learn complicated high level math.

Thankfully, the newbie didn’t cave and actually received a little backup from others who weren’t buying the transient shrug-off some of the more indoctrinated senior members were satisfied with.

Then, along came the Actuary

Then, along came an individual who named himself “actuary.” I have no idea if he really is an actuary (he did mention that he’s not an insurance agent), but he dropped this little note on the forum participants:

The commission and expense for whole life policy can be minimized. Many people in this forum don’t understand whole life insurance and don’t know the commission structure. So, they think whole life policy is expensive. An agent’s commission is directly related to the base face value of the policy. If you minimize the base face value and maximize the paid-up addition to the supplemental face value, the commission is minimized. Every mutual company provides this design to the customers through the blending ratio initially set when you take out the policy. Most of the time, the agents just set the base value equal to the total face value so that they can maximize the commission. That’s why the commission is 70% to 100% of first year premium for these high commission WL policies.

Okay, this is not 100% correct—insurance companies don’t start out with a blend of any sort of a given death benefit allowing the agent to just wipe out the blend and make sure that the entire thing is only whole life insurance—but it’s pretty close in terms of what we’re talking about when it comes to blending and policy design.

For more on blending whole life insurance, you can check out other articles we’ve written here, here, and here.

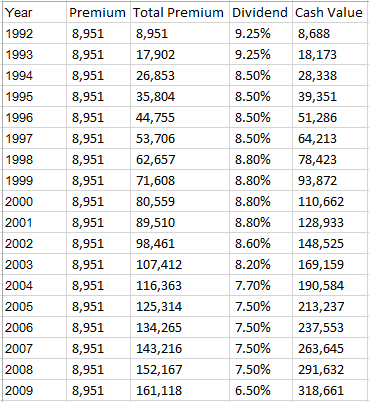

Anyways, the conversation went back and forth a bit more, and the actuary obliged a request to show the numbers. Here’s a screenshot of the numbers for those who don’t wish to visit the Bogle forum.

Universal life insurance wasn’t the only product that benefitted from higher interest rates

This policy started in 1992 with a premium of $8,951/year and ended up with $318,661 in cash surrender value by 2009 (the last full policy year prior to the discussion on the Bogleheads forum).

For those who are scared of doing the math themselves, that’s a year over year return of 7.76% (according to the trusty TI-83 Plus).

Gee whiz! With returns like that, who needs the stock market? I’m kidding, of course.

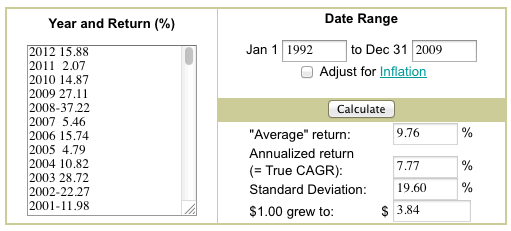

But, I would like to point out that, according to the awesome S&P CAGR calculator over at Moneychimp, the year over year return on the S&P 500 over the same period of time (1992 to 2009) was 7.77%. I’m attaching a screenshot if you don’t believe me.

Of course, that return would only be achievable if you paid no trading or account maintenance fees and could place all of your money into the S&P 500 from day one.

Oh, and for those looking to really have fun and keep score, I should note that the much-beloved Vanguard 500 Index Fund posts a miserable 2.55% per year return for the same time period.

And, let me also shove in that one aspect life insurance agents love to talk about: taxable equivalent yield. $8,951 is way beyond the allowable IRA limits back in 1992, and a plan started in 1992 precedes Roth IRAs by six years (they weren’t available until the passage of the Taxpayer Relief Act of 1997 and became officially available in 1998 with an initial contribution limit set at $2,000 per individual).

Taxable equivalent yield in this scenario would be approximately 10.61% – so much for those evil fees that destroy your savings potential.

Of course, it probably isn’t nearly as fun as buying term and squandering the difference. You would have needed that extra $8,000 in 1992 to buy a cell phone to call all your friends who didn’t have cell phones.

But, Blease doesn’t agree

We’ve had a few people tell us that agents they spoke to reference Blease (aka Full-Disclosure) and point out that the 50/50 blend historical results lag the non-blended historical results. The more informed among you will immediately see the flaw in the logic. For those that are bit newer to this whole blending business, allow me to explain the problem.

Blending wasn’t originally designed as a means to stuff lots of extra cash into a life insurance policy. That practice was the product of people with way too much extra time on their hands who didn’t listen to their sales managers and spent their days studying life insurance mechanics instead of obnoxiously trying to sell their (former) friends life insurance.

Blending was originally an answer to an industry that went mad over driving prices down and trying to be the cheapest purveyor of lost income via death protection.

You see, some people look at a cardboard box and tell you it’s just a box.

You can put things in it and carry them around, and that’s about all it’s good for. Others look at the box and realize it could also be a fort, a race car, a cat toy, a hiding place, and a temporary solution to a broken window (among other things).

Blending gained prominence (and is still mostly used) for the purpose of lessening those “expensive” whole life premiums when an agent insists you MUST have permanent life insurance protection.

Universal life insurance allowed insurers to assume really high interest rates that conversely reduced the amount of assumed needed premium to keep the policy in force. It looked amazing on paper; in practice, it didn’t work so well, but that’s another story for another day.

Blending quickly became a method for combating this promoted feature of universal life by using term insurance and a high (at that time) dividend assumption to bring premiums closer to universal life assumed premiums. This too failed miserably to materialize in the fashion purported.

To this day, blending is a common practice used to compete on price. We don’t talk about this application often because we don’t believe it’s generally a great idea.

Instead, we use blending to do exactly what our friend from the Bogleheads forum did: reduce the base whole life premium as much as possible and extend the death benefit to increase the allowable premium under TAMRA (i.e., Modified Endowment Contract) limitations.

Doing this allows us to dramatically shift the incoming premium from an expense-heavy base whole life premium to extremely inexpensive paid-up additions.

The Blease historical report shows a lagging performance among the 50/50 blended policies because those policies were designed to calculate a premium based on a stated death benefit.

Or, more directly, it shows us the performance of policies designed to address the more traditional application of blending, cheapening the premium. It does not address blending in the sense we are discussing.

What about the historical performance of non-blended policies?

If we look at Blease, the top performer over 20 years (which is a tad longer than our example above, but that’s all they have) comes in at around 5% year over year. We can also use these pieces put out by MassMutual and Guardian to look at specific historical non-blended policies. They aren’t bad, but they’re not as good as our blended example.

Be wary of the agent who bad-mouths the idea

There’s A LOT less money in blending when it comes to how an agent is compensated.

Agents know this, and it’s one of the primary reasons they pretend it (blending) doesn’t exist.

We’ve heard a fair number of ridiculous reasons not to blend, such as, “Only non-blended whole life insurance is pure whole life insurance, and that’s what you want.” Few things could be further from the truth.

Also, don’t fall for any claims that a product is pre-designed to be optimally funded to the modified endowment contract limit.

No company has a product that seeks to accomplish this and beats a blended product. We proved this a few weeks ago when we pointed out that one of the most aggressive marketers of such a policy, Ohio National, performed miserably compared to its own blended style product on income projections.

We have happened upon one new whole life product that appears to work better for competitive income when not blended, but this is a very unique circumstance, and it has limited applications. Most people will do far better following a blended design.

It removes considerable liquidity risk and gives the consumer way more control over the reserve development of the policy. As we can see, historically, it has smoked non-blended whole life policies in practice.

As always, if you have any questions, we are here for you.

I guess I should consider myself one of the lucky ones. I bought a whole life policy designed like this about 15 years ago and it’s worked out really well.

My only regret is that I didn’t buy more…

Hey Cheng,

We could help you with that regret… 😉

Good evening Brandon and Brantley:

Thank you for sharing this Blog to the Life Industry.

I Just read again, Blended Whole Life, what incredible information and value for the consumers, idea to use instead of a bank loan, fantastic value for the consumer and the broker.

Your firm really cares and offers so much to this industry.

Brenda and I really enjoy your site, and have you to thank for many sales. We have referred your site to many Producers.

Thank you

Michael j Travers

Mike Travers

Is there age restrictions on blended policies? Meaning if you reach a certain age like late 60’s that a 50/50 policy or a 25 whole/75 term will not work? How does a blended policy compete against a single premium traditional whole life policy which is geared to increase cash value almost immediately.

Hi Clint,

Some carriers restrict the age at which a policy can be blended and some do not.

The single premium policy will likely (if done correctly) have more immediate cash value and have a higher rate of return on cash since there is more cash from the outset and it ignores the need for a higher death benefit to remain compliant with Modified Endowment Contract rules (i.e. it is a MEC).

But the Blended policy will not bet a MEC and have the tax benefits a regular life insurance contract comes with so the real analysis comes down to whether or not the after tax value of the single premium product truly outpaces the blended whole life policy.

What do you mean by “blended”? Are you talking about blending whole life with term? Or are you talking about blending base premium with paid-up additions?

When we refer to blending, we are referring to using a combination of term insurance and paid-up additions. Unfortunately, there is not a uniformed way that all participating whole life insurance companies do this.

I wished I read your post before purchasing my first WL guardian policy last year. I’m thinking of purchasing 2 more policies for my 2 young daughters (age 3 and 5). Any practical advise on how to design it for max cash accumulation and best tax treatment.

Ie. should I buy one blended WL vs IUL policy and put them both as beneficiaries or 2 separate policies. Alternatively, is it better to buy life insurance policies on their healthy mother (age 38) or aunt (age 30) and list them as beneficiaries – is cost of insurance less for healthy young adult vs juvenile or does length of held policy trumps incremental saving on cost of insurance.

Hi Alan,

Having the parent as beneficiary will be the better bet for a few reasons:

1. Juvenile policies comes with additional expenses to accommodate the risk the insurer faces with the very limited underwriting information

2. Most carriers place very restrictive limits on the premium amount. Actually the death benefit amount, but due to young age and the required death benefit (much higher at this age) to remain compliant with MEC and 7702 the correspondingly allowable premium is small.

3. From a strategic point of view, you can pretty easily get money to them when they need it and you also have a death benefit that can pass tax free, which further augments value to them.

4. Several carriers restrict design options for juvenile options (e.g. several whole life companies don’t allow blending).

Using their aunt will be tricky unless you have a strong case for insurability.

If we can be of further help, or if you’d like some assistance policy design, feel free to reach out to us here.

Do you have any historical evidence for indexed universal life insurance?

Hello,

Yes we do and here it is: historical indexed universal life policy