Ventricular Septal Defects or VSD’s are holes in the interventricular septum (the wall that separates heart chambers) of the left and right ventricles. To be clear, generally it’s one hole in the septum (not several, though not unheard of). When it comes to life insurance applications for proposed insured’s with a ventricular septal defect, the applicant generally has really good prospects for being approved, and being approved at better than standard rates (assuming the applicant qualifies for better than standard rates based on other health criteria).

However, there are a few considerations when it comes to individuals who have this condition that underwriting will review quite carefully. And to ensure efficiency in processing the application, it’s best to try and provide as much information as possible at time of application to avoid confusion and ensure underwriting has no apprehensions.

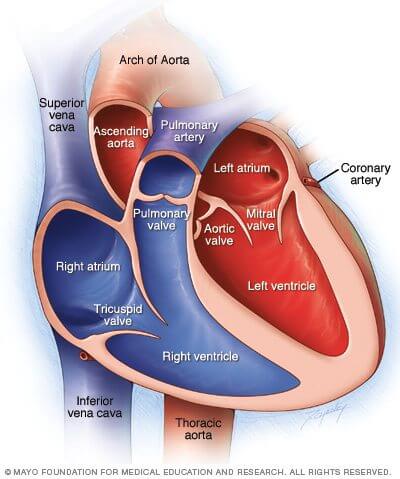

The Heart, a REALLY Basic Primer

I by no means want to suggest any of the following is an exhaustive account of the human heart, so if you work in cardiology I know I’m leaving a lot out. Let’s go back to middle school biology for a second and remember that the heart is compose of four chambers, two atriums (the upper chambers) and two ventricles (the lower chambers). There are valves that separate the atriums from the ventricles (the Tricuspid valve on the right and Mitral valve on the left). And the upper and lower chambers of are separated from each other by a wall known as a septum (as we’ve already covered).

In the picture above the septum (or interventricular septum, if you really prefer precision) is the thick pink line that tapers at the top between the chambers labeled right ventricle and left ventricle.

Size Matters

Large VSD’s can cause problems primarily due too much blood flowing (in fancy medical jargon they call it “shunting”) from the left ventricle to the right ventricle through the defect—which can also be reversed to a shunt that flows from the right to left ventricle (a much bigger problem)—that overloads the lungs and the ventricles leading to a host of nasty problems. For this reason, larger VSD’s are often surgically closed if they don’t close on their own.

Small VSD’s usually don’t present a problem. Some close, and others don’t. Those that don’t general require little more than regular follow-up with a cardiologist and periodic echocardiograms to ensure that the heart is functioning properly.

Life Insurance Underwriting and Ventricular Septal Defects

Providing there are no complications most applicants with a VSD do not fall into substandard territory (in fact many can be issued at better than standard rates if they would have otherwise qualified).

Being current on one’s health maintenance is key. This is specifically true regarding health maintenance with cardiology. Individuals with small VSD’s that remain through life are at a slightly increased risk of developing Endocharditis (an infection of a heart valve that requires medical intervention with antibiotics) and Aortic Regurgitation (essentially an aortic valve that doesn’t function properly). Both conditions can be serious medical conditions, but healthy individuals with up-to-date health maintenance generally have little to worry about. A clean history with no complications should yield favorable results.

How to Approach Underwriting…More is Better

While we often been of the opinion that one should only answer questions asked of them in a life insurance application, this is one area where more information is better (and yes all applications will ask about heart defects). Most people with VSD’s likely don’t know the technical term and have little understanding of what precisely is going on. Perhaps your doctor told you at one point that you have a “heart murmur.”

The term heart murmur is extremely vague and can mean a multitude of things, so being able to explain what exactly causes your murmur is helpful (but don’t freak out if you don’t know).

VSD’s will often trigger a requirement for underwriting to review your medical charts. Knowing where those charts could be (by listing the doctors you’ve seen) is helpful. As I sort of mentioned above the type of specialist you will almost certainly see for this is a cardiologist. Generally speaking, the cardiologist will have seen you for an office visit, listened to your heart, and reviewed echocardiograms performed to ensure that your heart is functioning properly. Being able to provide names of cardiologists or medical facilities where you were seen can be very helpful.

Ventricular Septal Defects are not generally a difficult condition to underwrite for life insurance providing there is no history of complications. If you have one, are healthy, and regularly see your doctor being approved at standard or better rates should be achievable. If you feel you need help with this, we welcome you to contact us to discuss in more detail.