Buy term and invest the difference has long been the mantra of investment salesman(women) and Primerica built an entire company around the idea. The premise behind the concept has always been that one could achieve a greater return with “investments” vs. traditional whole life insurance and it’s cash surrender value build up.

For the investment industry, this was a way to take premium dollars away from the life insurance industry and redirect it into investment accounts. For Primerica, this was a way to replace current life insurance contracts with term insurance juxtapose on the cost today of achieving a given death benefit.

Other financial talking heads have jumped on the buy term and invest the different bandwagon, mostly because they know it draws a lot of attention from life insurance agents who want to argue the point—and few things draw more attention to you than a fight.

As insurance brokers/agents, one would anticipate that we’d very much dislike the notion of buy term and invest the difference, but one would be wrong to make that assumption.

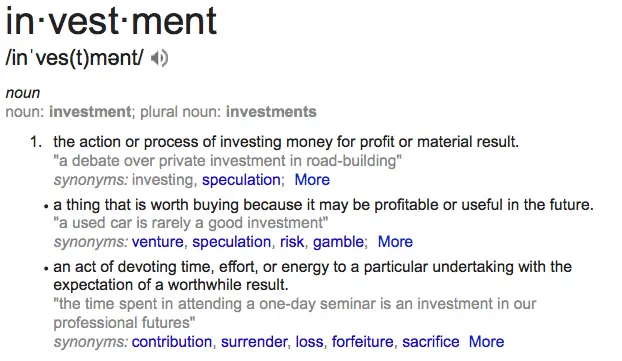

What is an Investment?

Here’s the definition of investment as it appears at dictionary.com.

Notice the underlying theme behind all three iterations of the definition. The commitment to some “thing” under the assumption that later in the future it will be worth more than it was originally.

Buy term and invest the difference is less about investing the difference in cost between whole life insurance and term insurance and more about taking that difference and buying mutual funds (mostly, maybe stocks in some cases). But mutual funds are not the only investment that exists in the world. Before we go down that road, let’s stop for a moment to talk about something else.

Term Life Insurance is a more Efficient way to Buy Death Benefit

The foundational claim behind A. L. Williams and later Primerica was that term life insurance was a more efficient way to purchase death benefit. And in the short term, they are correct. There’s no arguing that from year one, there is far less outlay that would be needed to achieve a given level of death benefit on any individual vs. whole life insurance (and universal life insurance).

There should never be any confusion about this among our industry. From time to time we will have people ask us how they should go about getting the death benefit coverage they need while not having the premium they are placing into a contract be enough if we design it to maximize cash value. Our answer has always been the same: buy stand alone term insurance.

We’re not all that interested in ruining a perfectly good life insurance contract, designed to optimize cash value, because someone wanted/needed more death benefit for a period of years while they were working or whatever other obligation existed that forced them to need the additional protection.

And making this suggestion does not nullify the fact that whole life insurance and universal life insurance can be phenomenal savings plans. We could even argue…investments (see the definition above, it fits). In fact, I’d argue that it’s the confusion many agents like to make about this, that leaves a lot of consumers in a really bad situation, with a sub-optimal product for both cash value accumulation and death benefit goals.

One Product will not Cure all your Woes

As much as we might want to try and convince ourselves otherwise, the life insurance industry has yet to manufacture a product that fixes all of our problems better than any other product. Instead, most problems require a focus on (and therefore purchase of) more than one product.

So if you’ve discovered that cash value life insurance is a wonderful tool for wealth accumulation, retirement income, education funding, etc. we’d strongly argue that you purchase your product with the intention to maximize that feature. Trying to wrap everything up into one product will do you no favors, and attempts to do this are the biggest reasons regulators breathe down our backs and suggest we’re not acting in a clients best interest (because, honestly, if you try to accomplish both with one product you probably aren’t acting in a client’s best interest).

Whole life insurance and universal life insurance are phenomenal ways to acquire cash that has a lot of benefits behind it. And analogous to these products’ incredible cash building abilities, term life insurance is the rockstar when it comes to death benefit protection. It’s as simple as that.

So for those with a serious death benefit need, yes you should buy term insurance. And then you should invest the difference. Now the big question becomes…what should you invest the difference in. And that’s where the true debate lies.