Podcast: Play in new window | Download

(Complete Show Notes Below)

![]()

![]()

In the 40th episode of the Financial Procast:

Yes there are times that Whole Life Insurance is NOT the answer

I know many of our regular listeners may be shocked to hear us make that statement. But it's the truth.

There are times that whole life insurance and all other types of cash value life insurance is not the right answer. We actually recorded this episode in response to an article that we saw published in the last couple weeks that was lamenting the fact that Dave Ramsey, Suze Orman and other financial entertainers are doing a disservice to Americans by leading them down the road to purchase ONLY term life insurance.

Actually, we think that in a great many cases, they're absolutely correct. And their certainly correct when speaking to a vast majority of their respective audiences.

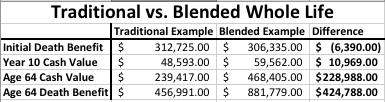

Also, as promised in the episode here's the infographic Brandon was referring to. This comes from Penn Mutual, a company that we like and do business with on a regular basis. However, we use this graphic to point out the disconnect when marketing whole life insurance.

Click the picture to see the complete infographic

Here's a recap of the numbers:

Example is awful for perm life. In the fine print – the yearly premium is $5000 for the perm life. Typically, the cost of term for the same duration (say 30 years here) is 1/10 the premiums. So, $500/year for 30 year term. Invest the difference ($4500) and make a meager 5% in a roth ira (no taxes on earnings & likely you can do better) and u have ~$600K at age 60 when u stop paying. With the perm life, I can pull out $250K OR die and have the $450K. This is a no-brainer

With an argument as original as this, I’d have been much more impressed if you had chosen a more creative anonymous name. Perhaps Bill Murray. Or maybe Punxsutawney Phil.