Some financial bloggers appear to hate whole life insurance. A good lot of them have blog posts dedicated to extolling the virtues of term life insurance over whole life insurance. According to them, whole life insurance is:

- Expensive

- Illiquid

- A terrible “investment”

- Sold not bought

- Confusing

And that's just a few of the not so nice things they say.

Whole life, they suggest, is an out-dated con that over-charges you for the same death benefit you could buy (temporarily) with term life insurance. So why the hate for whole life insurance and love for term life insurance?

Are these bloggers veteran insurance agents who discovered the ugly truth about whole life insurance after years of watching insurers gouge unsuspecting consumers? Are they researchers who extensively compiled data that points in the direction of term's superiority? No.

They are people with an opinion. How did they happen upon this opinion? Well, to uncover that, we have to follow the money.

Whole Life Insurance vs. Term Life Insurance an Original Discussion for your Blog

Contrary to what any financial blogger (me included) might tell you, the debate over whole life insurance vs. term life insurance stretches back far before the time of blogging. If we go back to the original arguments levied against whole life insurance in favor of term life insurance, we find an interesting link to the modern-day naysayers. There's a little bit of a financial incentive for them to not like whole life insurance.

A.L. (Art) Williams holds the crown on the charge against whole life insurance. At least he's made the most money doing it. More than practically all of the term-only peeps combined who popped up after him. The foundation of the A.L. Williams Life Insurance Company (now known as Primerica) hinged on one–and only one–unique (at the time) sales angle. Whole life insurance is expensive. So you can buy much more death benefit protection if you buy term life insurance. So you should do that. This later evolved into buying term life insurance and investing the difference (as the Stock Market became more mainstream).

Today, Primerica agents still prey on whole life purchasers with suggestions about how much less they could pay for the same death benefit. Virtuous crusade? More like a great excuse to cancel your policy and buy one from me. That way I earn a commission!

Primerica agents aren't the only ones who jumped on the buy term and invest the difference (BTID) bandwagon. It became a favorite recommendation among investment product salespeople. The reason should be fairly obvious. Hint: it helped them make money.

So what's the link to the modern-day financial blogger? They don't sell life insurance or investments…do they?

Not directly, at least not most of them. But they do love a good affiliate program, and when it comes to generating term life insurance leads over the internet, there are plenty of term life insurance brokerage companies looking to pay bloggers for lead generation.

Whole Life Insurance Sucks, and by the way, I Can Help You Buy Term Insurance

The most vocal whole life critics among financial bloggers all share one thing in common. They appear to be helpful little buggers with respect to hooking you up with a source to buy some term life insurance.

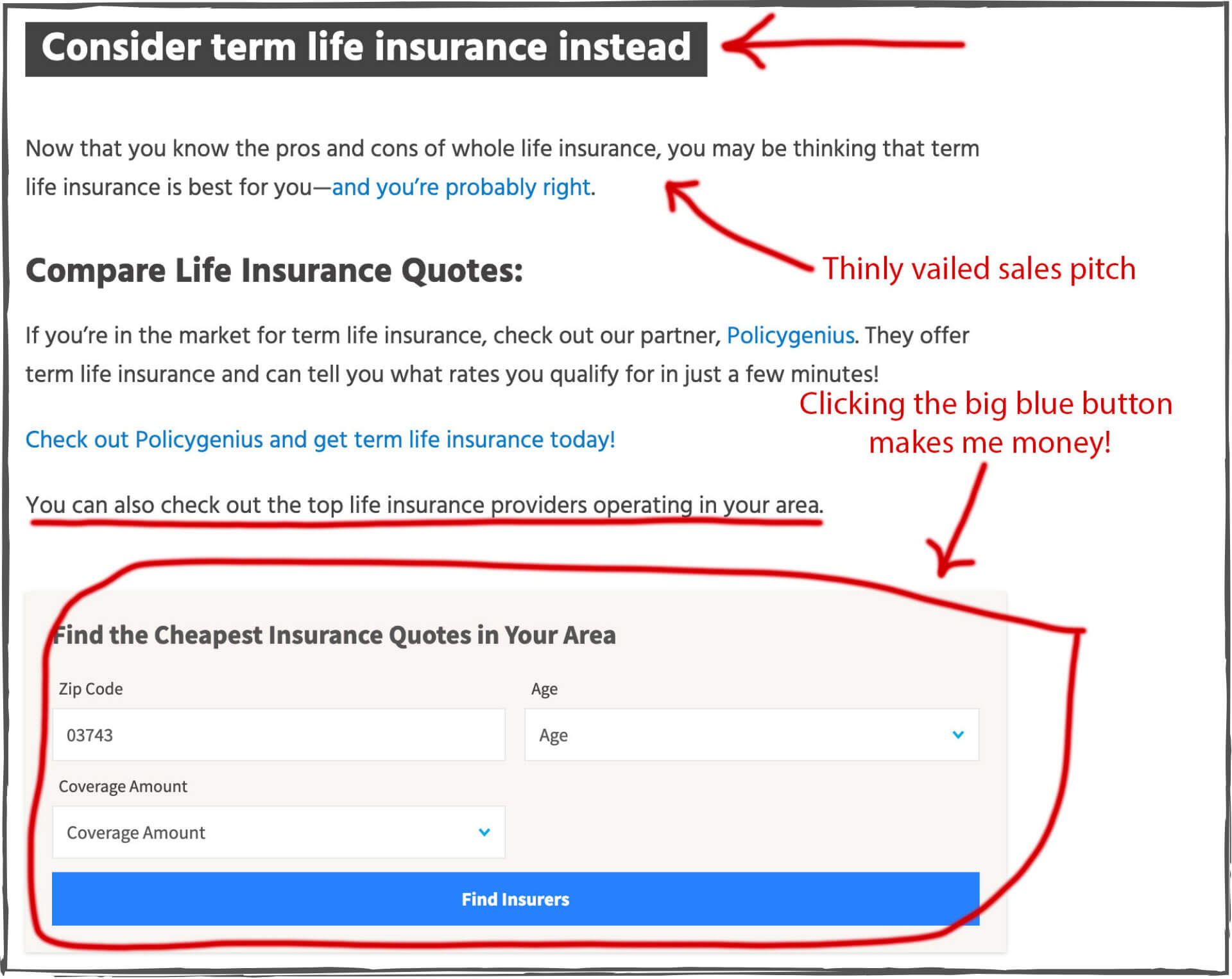

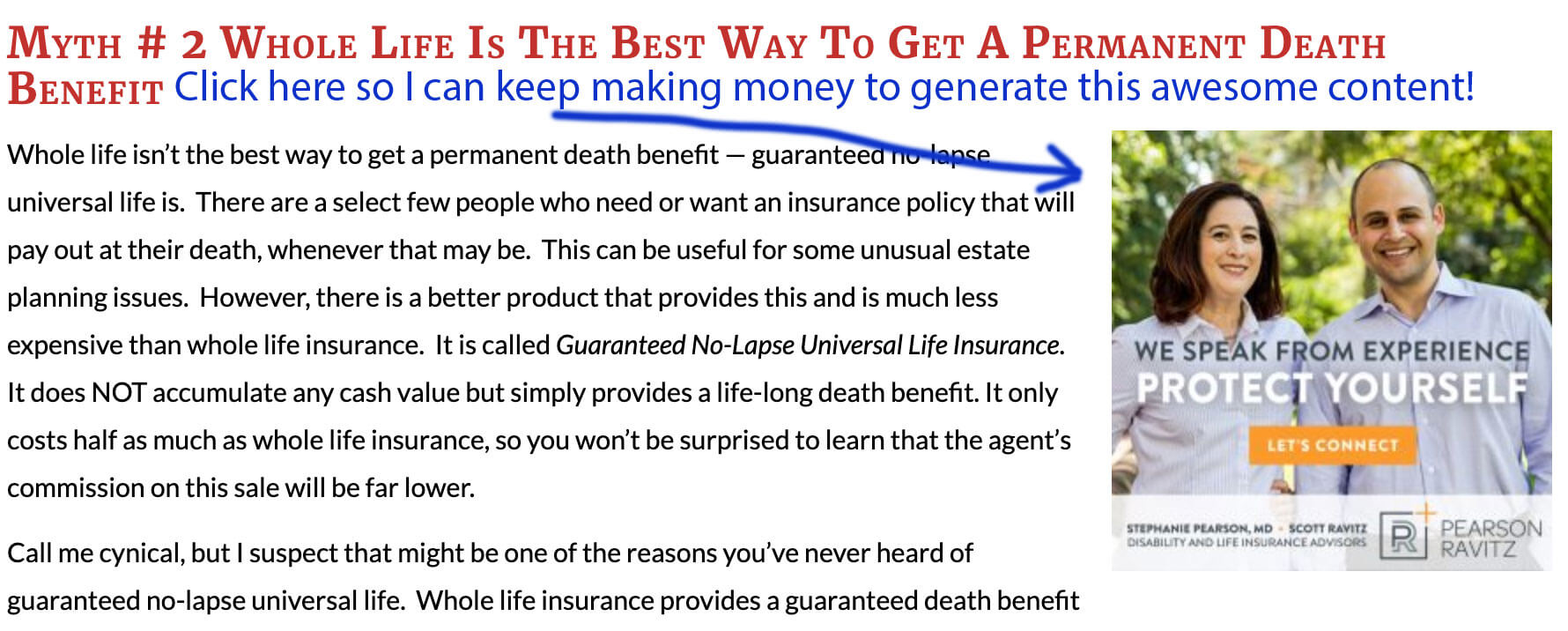

Here's evidence I compiled from six different websites that all bash whole life insurance:

As you can plainly see, these blog posts that seek to build the case against whole life insurance all conveniently have advertisements to help you help them make a little money by introducing you to a place to go by term life insurance.

Now, I'm not saying that all of them only prefer term life insurance because they have a way to monetize content through a lead generation tool with term life insurance. I am, however, aware of no lead generation tools available to bloggers for whole life or universal life insurance. It's also interesting that some of them talk about guaranteed universal life insurance, which is a product offered by many of these same online term brokers that are paying for lead generation for term life insurance.

Is Whole Life Insurance Bad? Or is this a Great way to Sell Term Insurance?

Bloggers blog to make money. Or at least that's the hope. So most bloggers have a funny way of taking up a position that has an advertising angle. Maybe these same bloggers came to the internet already in love with term life insurance and ready to argue against whole life insurance. I have no way of knowing. B

ut again, knowing that no current resource exists to compensate bloggers for advocating whole life insurance, it does seem odd that they overwhelming appear to favor term, and “serendipitously” have the opportunity to also advertise for a term life brokerage company.

Few, if any, of the attacks on whole life insurance are anything more than superficial. Even the more thorough attempts to tear it down lack substantial numerical evidence that it is bad and usually employ intentionally weak examples of a policy to make their case. You could say, their arguments often lack substance in much the same way a political attack ad does.

I bring this up because a lot of financial bloggers claim that insurance agents want to sell whole life insurance because there's a lot of money in selling whole life insurance. My experience is that most agents just want to sell life insurance–they don't really care what flavor it is.

At the same time, these same bloggers conveniently gloss over the fact that there is lots of money in hating whole life insurance on the internet. Sure most of them fulfill their legal requirements to disclose compensation earned on affiliate links (some do a much better job than others), but to criticize someone else for advocating a product because he/she will make money doing it, appears hypocritical given the circumstances.

But Don't You Sell Whole Life Insurance Yourself?

Yes, I make money selling whole life insurance, universal life insurance, AND term life insurance. I'm a licensed insurance agent and have been since 2008. One of the very first pages I created at The Insurance Pro Blog was an FAQ that explicitly noted that we sell life insurance. We've mentioned the fact that we sell life insurance numerous times in several blog posts and podcasts. Life insurance sales aren't the only way we monetize this blog, but it certainly plays a role.

I'm not suggesting that making money off an opinion about a subject makes you a bad person or even makes your opinion count for less. I'm merely pointing out that term advocating bloggers have the same incentive I do. We do differ, however in what I feel is a critical way.

I don't make money simply by sending people to a lead generation form. I only get paid when I also accept the responsibility of guiding someone to a life insurance design or purchase. This places a significantly larger responsibility on me to get it right. And I take that responsibility very seriously.

Your ending paragraph and point therein is truly admirable and respectful. I entered the industry in 2014 to help people and have been following this blog since 2016. There is a major reason for that: you all are caring, knowledgeable, educating, funny, enthusiastic, and impactful advisors. It’s great energy to follow that and learn from it. Thanks guys!

Travis Beyerl says it right, I am following your blog for a long time going back to 2011-2012. It’s very helpful and knowledgeable. Don’t be afraid of those so called online bloggers, there will always be people who like and appreciate what you do, and people who don’t. You can’t have everyone on your side, just look at it as a half cup full situation, the people who are smart know the facts about this. Lets keep up the good work Thanks again.

It’s not a matter of being afraid.

The issue is that uninformed, unlicensed, individuals, embed unjust negativity on an complex subject, onto persons who are easily influenced and who will settle for an inaccurate, incomplete, information, in lieu of properly researching an optimized solution to a multi-layered situation.

In essence, these hacks closed minds to the point that as an agent, it’s impossible to reopen that mind, gather proper and complete information, and discuss legitimate complex options, with said person.

Respect for you man as a fellow financial advisor here in Philippines. BTID is also the most common advocacy by financial gurus here and I feel that btid now is not the best choice out there. I realized that this market crashes might or would happen again in the future, and worse if happened a year before retirement.

I hope that there would be high cash value insurance soon here in Philippines.

Did my own research as a buyer , but an insurance company investing my money eating the majority of the profit and then eating me up in fees, ehhhh I rather just keep my retirement accounts at least I know I’ll have an actual pot of cash left over. Not a un-guaranteed vs. guaranteed being much less than I invested.

Hi JV, so you think you can do better with some alternative? That’s fine; good luck with it.