Podcast: Play in new window | Download

Several years ago, I published a blog post that used real whole life data results to compare to passive index investing results. The results showed that a well designed whole life policy that maximizes cash value comes extremely close to the results we can anticipate from passive index investing.

That's not, of course, to flat out suggest that stocks cannot beat whole life insurance–I believe strongly on the contrary. But, it does call into question just how much of a delta exists, and to what degree that delta is worth pursuing.

Sadly, the last data point from that real whole life policy ended in the late 2000s and I don't have a way to uncover the results from that time. Though I did perform some number crunching to speculate what the results would be some years later, I don't have anything current.

So wanting to know how the market compares today against blended whole life insurance (base+term rider+paid up additions rider) left me with one option…my own whole life policy.

Well, one of my whole life policies. One that I purchased in 2012. One that is now eight years old and one that I intimately know. One that I can also go back and use the premiums to make a hypothetical investment in a passive index ETF to compare how the results compare today.

The Boring Details

I know the premium payment history for my whole life policy. So it's easy for me to recreate an investment scenario using those identical premium payments.

Compiling data using the portfolio visualizer for the Vanguard 500 Index ETF (VOO), I recreated an investment scenario that captures the real investment results I could have achieved (this means dividends included) if I had taken the same premium dollars and instead bought shares in the VOO.

I've made one minor adjustment to the results, I've assumed that I paid a 1% per year fee that covers any advisor fees or taxes due. I'm assuming this is non-qualified money.

Here's why:

- I already make contributions to an IRA and

- My life insurance premium amount exceeds the annual contribution limit for an IRA.

The whole life policy in question is a blended whole life policy that makes optimal use of the paid-up additions rider. It was issued on my life as the sole insured in 2012 when my attained age was 26. The policy risk class is preferred plus. The dividend option used in all years is paid-up additions.

My whole life policy technically started in late April, so I'm not at the end of the policy year just yet. I decided to ignore this and assume the ETF investment took place from April 1, 2012, through March 31, 2020. This is close enough.

It handicaps my whole life policy slightly because my values are missing this year's dividend payment. That handicaps my whole life policy by a few thousand dollars, but it doesn't change the results enough in my eyes to worry about it.

Because I'm not crazy about exhibitionism, I'm not going to share the actual numbers, but I will share the graphs and relative results (percentage differences) of this exercise. That's the more intriguing and educational part of this endeavor.

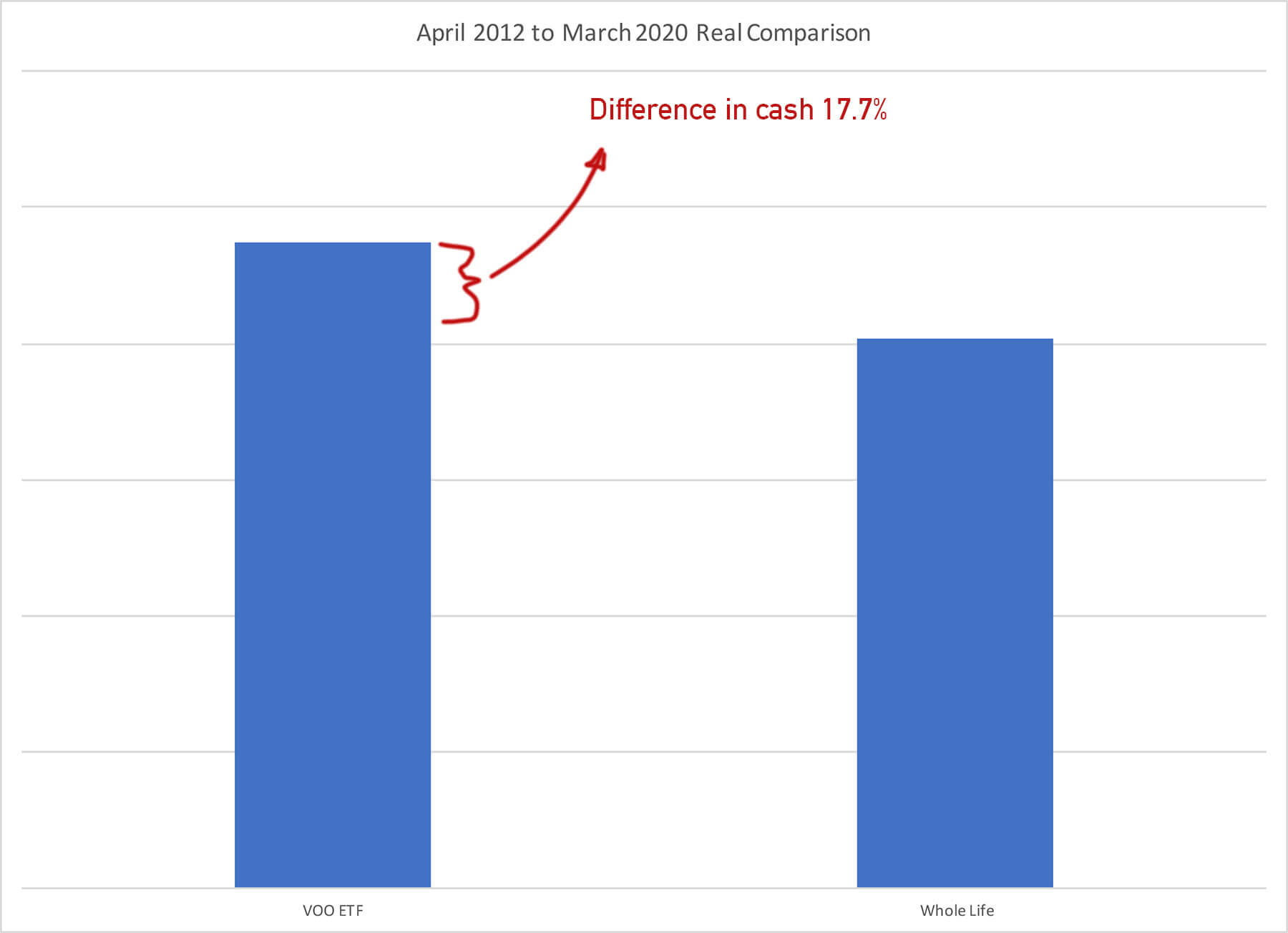

Results Part 1: Whole Life Versus Vanguard 500 Index Fund (VOO)

The ETF investment produced 17.7% more cash than the whole life policy. Assuming this is a non-qualified investment, I would have to pay capital gains taxes upon liquidating the investment, so that does adjust the difference somewhat. If I factor in capital gains taxes (not included in the chart above) the difference becomes 13.4% more cash in the ETF investment.

This 17.7% difference appears large in percentage terms, but in real dollars, it's not quite as impressive. As you can see in the above chart, it's a modest increase over the whole life cash value. The real dollars amount to a sum that might cover the average family's living expenses for a few months. It's certainly not an earth-shattering difference.

Making the investment in the ETF also forgoes the death benefit provided by the whole life policy, which is not an insignificant sum. This death benefit not only provides income replacement if I died prematurely, but it also provides supplemental protection from a catastrophic event that might require long term care (through the chronic illness rider or accelerated death benefit rider). This very likely reduces my expenses of addressing this risk as I get older.

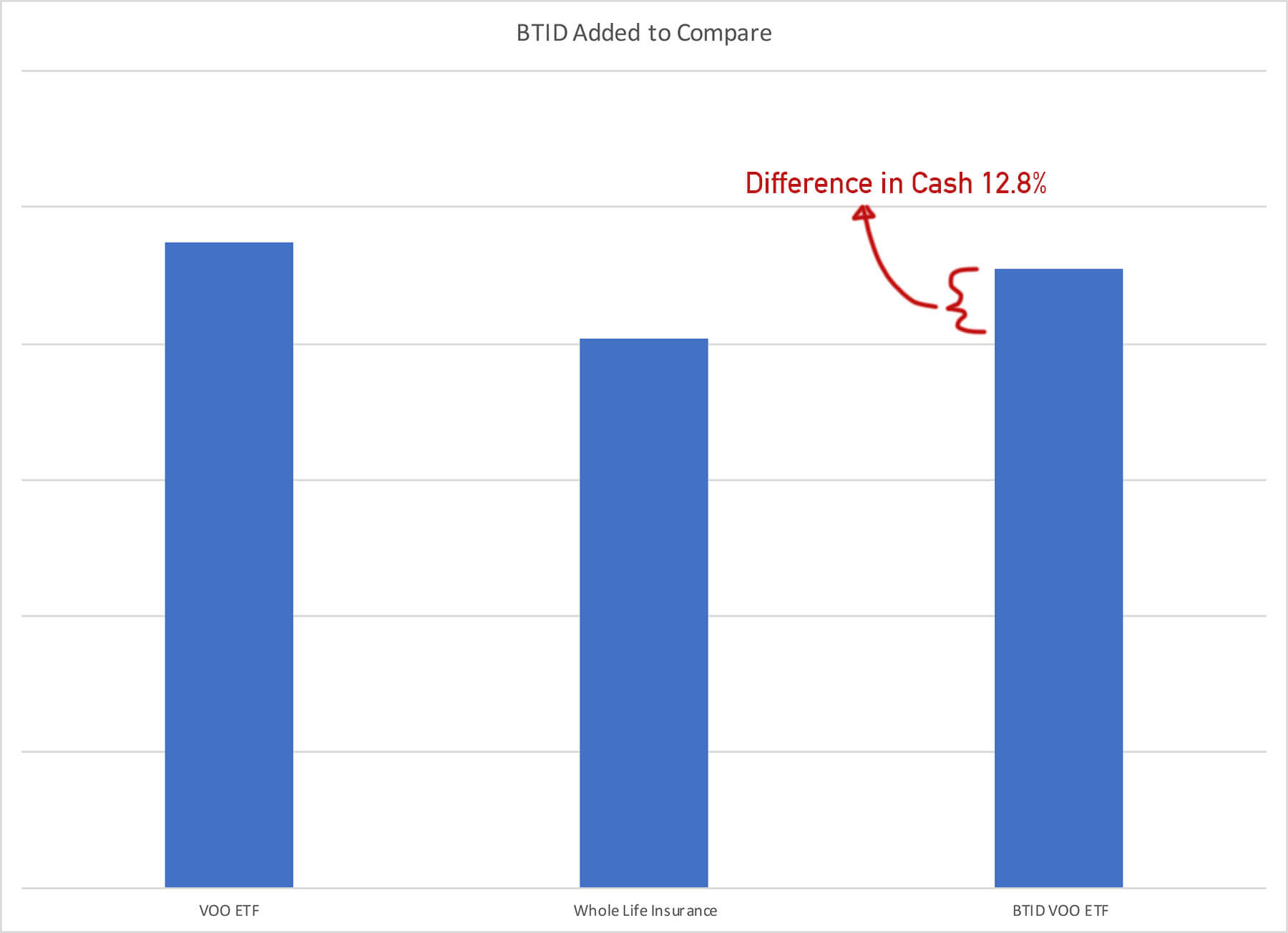

Results Part 2: Adding a Buy Term and Invest the Difference Component

Because I believe the death benefit I established by buying the whole life policy has significant value, and because there are plenty of self-proclaimed financial experts who would suggest it's the way to accomplish the same goal, I re-ran the numbers assuming that I did buy term and invest the difference.

At 26, the appropriate amount of term death benefit to match the whole life policy is super cheap (yay!). So there's a small adjustment, but a downward adjustment nonetheless, on the amount invested and therefore the amount of money I end up with by March 31st, 2020.

Here we see the original (not BTID) investment, the original whole life results, and now the adjusted values assuming that I bought term and invested the difference. The BTID scenario does result in more cash than the whole life policy, but the delta shrunk to 12.8%. Visually, as you can see from above, it's not a gigantic difference.

Also, if I again factor the effect taxes play on liquidation of the investment account, the difference shrinks further to just 8.7% between the ETF investment and the whole life cash value. Interestingly, buy term and invest the difference has a larger tax impact on the net results because I cannot count the dollars used to pay term premiums as the cost basis.

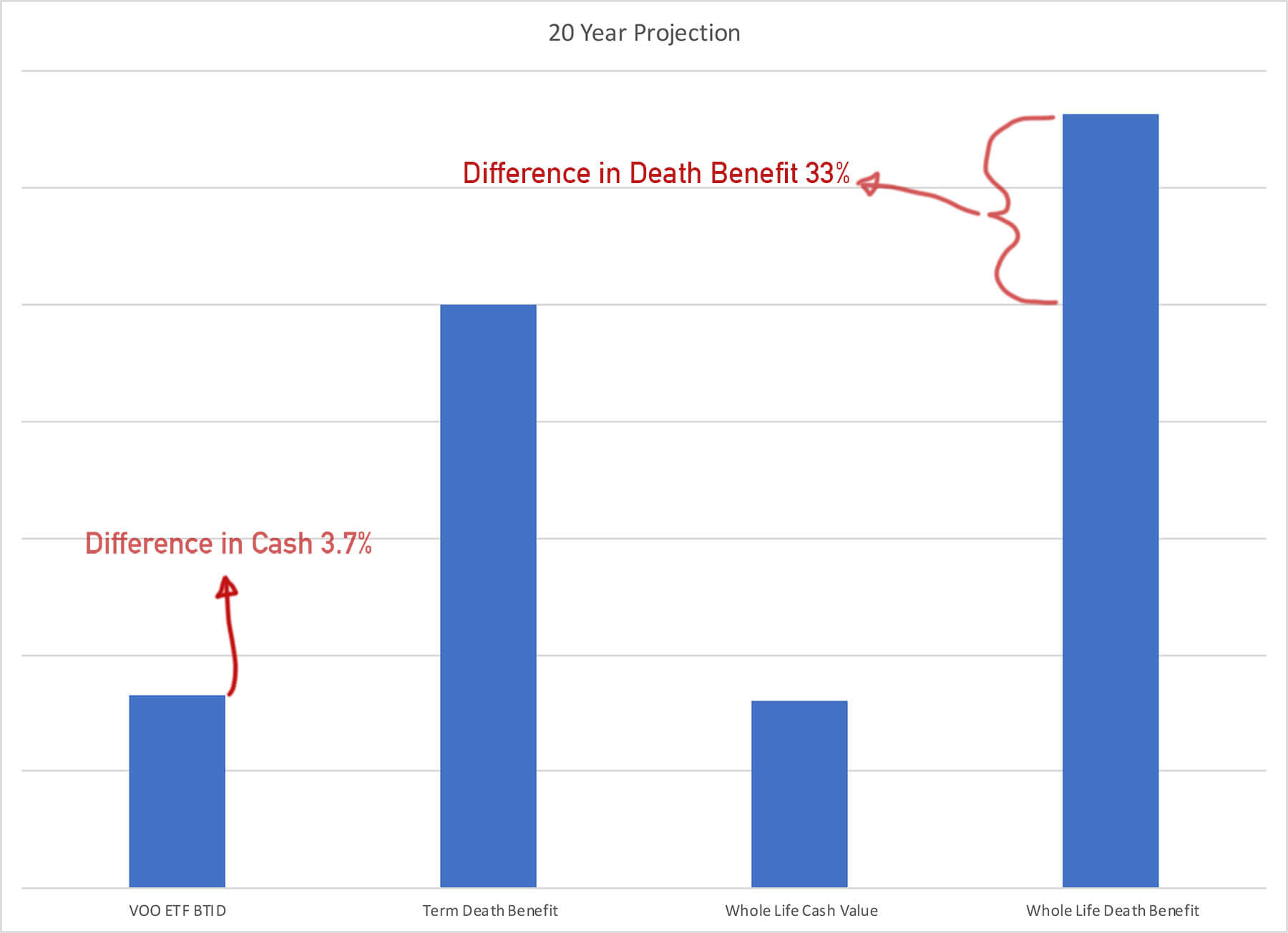

Results Part 3: Projections 12 Years Later

As insightful as these results are, they only span eight years. Any reasonable person would look at these results and note that eight years is unlikely to be a long enough period to declare either approach a winner or loser.

So I wanted to look at these figures as time stretched on.

To do this, I needed to make some projections using the current data to extrapolate where things might end up by the time I'm 20 years into this. I was mostly interested in the buy term and invest the difference comparison because there's no way I'm going to just give up the death benefit afforded by the whole life policy throughout this period.

Using the calculated year-over-year rate of return from the ETF investment (came out to 6.5% per year) I projected where the investment would end up 12 years from now. I used a simple future value calculation with a time value of money calculator to arrive at the balance.

To me, there's no reason to assume that this time either over or underestimates the results of an investment in the market, so this data is sufficiently long enough to make such an extrapolation (much more on this point in the next section).

Then I could simply run an in-force illustration on the whole life policy to project values 12 years from now.

The difference in cash is extremely minor at only 3.7%. In fact, the capital gains taxes due upon liquidation are larger than the difference between the ETF investment and the whole life cash value.

What's also noteworthy is that the death benefit on the whole life policy has grown substantially over this period and is now 33% larger than the term death benefit. So I'm very close in cash value results, and I've achieved significantly more death benefit by owning whole life insurance.

Also, note something by looking at the above chart. Look at the bars that represent the ETF value and the term death benefit. They are nowhere close to each other. This means the self-insuring goal I'm supposed to accomplish with buy term and invest the difference is nowhere near complete.

I arrived at my last year of the 20-year level term policy. If my ETF investment doesn't achieve an unprecedented return in the next 12 months, I'm going to need to buy some more term insurance that will very likely be 338% more expensive for the same death benefit, which will be far less death benefit than I have outstanding on the whole life policy at that time.

If I want to do that, my term premium will be 419% higher than I was originally paying.

This assumes, of course, that I can get life insurance at this point. I hope to be healthy in my mid 40's and capable of buying more life insurance if I want it, but there's no guarantee that will happen.

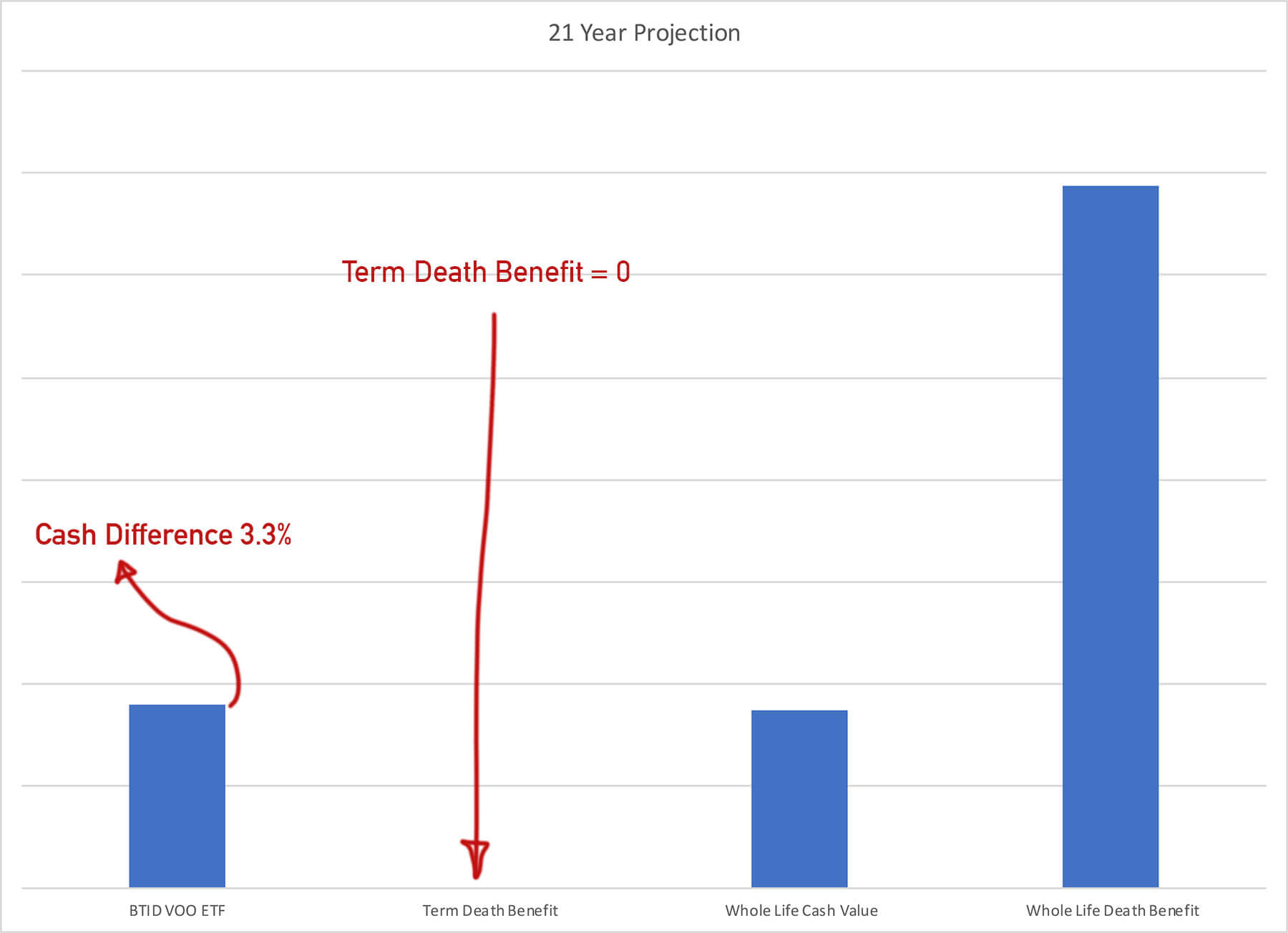

What happens in year 21 if I let the term insurance go?

Just one more year ticked by. The difference in cash has further shrunk to just 3.3%. Again, the capital gain taxes due if I sell the ETF will bring my net amount below the whole life cash value balance.

And I have no more term death benefit. Ignoring the capital gain tax for a second, the difference in cash result is minor but look at all the death benefit I've managed to acquire and keep without question.

Again death benefit that not just covers lost income from premature death, but also helps defray the costs associated with long term care planning. A death benefit that is growing quite substantially over the years (at this point it's more than double what it started out as).

Implications and Observations Given Results

The absolute and relative difference in terms of cash between my whole life policy and the hypothetical ETF investment is fairly minor. In fact, I expected the ETF to produce a much larger spread between it and the whole life cash values.

Because my period began in April and ended in March, the investment return results were different than the annualized returns you will see if you look at a stock quote for VOO or for the S&P 500 in general. The resulting returns for my hypothetical investment are actually better than the annualized returns quoted as January 1st through December 31st results for the same period.

In fact, during the eight years, there was only one negative 12-month result, April 2019 to March 31st, 2020, and that was only -6.98%. The other 12 month segments were positive and five of the remaining seven segments achieved returns greater than 10%.

Matter of fact, the average return over the eight years was 10.38%.

However, the calculated year-over-year return was 6.5% for the ETF investment (compound annual growth rate). This result is not all that surprising given the large analysis I did a few years ago to arrive at various stock market return probabilities.

Also noteworthy, a lump sum investment beginning in April 2012 and ending March 2020 would have grown annually by 10.12%. I include that just so you can see the difference between the actual period I used versus the calendar year returns.

As we explained in a previous blog post, lump-sum investing and systematic investing are different and yield very different results. Stock hawkers love to confuse these implications and results.

To repeat a comment made on this blog a time or 10, whole life greatly improves with time. It becomes significantly more efficient over the years.

You can plainly see that play out as the gap between the whole life cash value and the ETF investment results converge. For those super interested, the calculated year-over-year return on my whole life policy at this point (2020) is only 2.7%.

That's certainly not a result anyone gets excited about, but this is a policy that is only eight years old. Many people don't see results like this for a decade or two (design really matters, I say that often). But I'm not worried about the 2.7% year-over-year return I achieved to date, because I know that this result will improve dramatically over the next several years.

My Plans Given the Results

I'm planning to hold on to my whole life policy. My next premium is due in a few weeks and I will pay for it. I'm fortunate to be in a position to continue funding my whole life policy despite the current economic crisis facing the nation.

These results reinforce the priority whole life insurance plays in my financial life. I'd sacrifice a good number of other things before the old whole life policy.

I'm happy that I bought whole life insurance and glad that I did not take the premium and instead buy an ETF. In full disclosure, I have taken other money and used it to invest in stocks.

I have a decent amount of cash value at the moment and will have even more as time goes on. This will play a major role in my life in the future.

I feel completely safe to risk other money in the market and have done just that with the current market collapse. Some ideas have worked out better than others, nothing causes me serious pain in terms of bad ideas. It's not fun to see thousands of dollars get wiped out over a bad call, but it's also comforting knowing that I have a lot of money sitting somewhere supremely safe.

Some exclaim whole life insurance isn't worth owning unless you happen to own one for many years, then it's okay because you overcame all of the “expenses” of the policy.

I can't wrap my head around this logic. I also can't wrap my head around the toilet paper hoarding that is presently going on, so maybe someone with a basement full of TP can explain this to me?

Following this logic, any asset that has an acquisition cost isn't worth it. That's certainly a statement that few (if any) will get behind.

I also suspect that some will discount all of what I've documented here because I'm an insurance agent. Implying that these results only work out in this fashion because I'm an insurance agent and want to sell you life insurance.

Somehow the math that underpins these results doesn't matter? It's okay that they make this argument. It further supports my point that they don't have a real argument against whole life insurance.

I love whole life and am a huge advocate for positioning it appropriately within a client’s portfolio, but kinda feel like using numbers from 3/31/20 is exploiting data from the current circumstances to make the argument. What happens to the numbers/projections if we look at 3/31/19?

Mike, keep in mind that the 12 months period Apr 1st 2019 through Mar 31st 2020 is only down 6.98% and it’s the only negative 12 month period of the entire eight years. Additionally March 31st isn’t the low point for the market, so if I wanted to exploit the current situation, I could have moved the goal post to that exact date.

Yes current circumstances aren’t great for the market, but this is one of those situations where someone somewhere will come along and argue that this analysis benefits from the unfortunate down turn in the market no matter where I set the beginning and end date.

In addition, the data doesn’t deviate from traditional stock market results. The average return and standard deviation are well within the range of the stock market for much longer time periods. This is a common quality check anyone performing this sort of analysis should perform to ensure that the data subset is representative of the larger set it seeks to analyze.

I understand the differences in outcome but what is the input? Did you include the yearly premiums and if you did I would think you need to add that amount to investing in VOO.

Of course you are absolutely correct on the death benefit front

The amount invested in VOO is the same as the premium paid in the scenario.

A few problems. First, you spend a lot of time on this blog trying to explain how people should shop for cash value life insurance by, say, using a blended whole life policy with PUA rider. After educating the investor so much, why do you assume the investor is going to turn around and do a pretty dumb thing, like pay an advisor 1% AUM to be in an S&P 500 index fund? It’s not a reasonable assumption. If you’re going to include an AUM at all, it should be 0.25%.

Second, you’re deducting capital gains taxes, but you’re not explaining your assumptions. For 10.38% to get to 6.5% and adding back a 1% AUM, you’re talking about a long-term capital gains tax rate of 28.8%. That’s reasonable for some high-income investors but not for others, and it’s material because tax deferral is a big driver of cash value life insurance.

Third, you’re deducting taxes for the stocks but not surrender fees or taxes on the life insurance policy. You might say that the life insurance policy allows strategies like loans, dividends as return of premium, etc. to minimize taxation. Well, so do capital gains on stocks–include return-of-basis when selling specific tax lots, tax loss harvesting, charitable donation, and step-up at death. So dinging the stocks here without any strategy while blessing the life insurance policy is very unreasonable.

I didn’t say I was assuming a 1% AUM fee. I said I was adjusting yearly results by 1% to take into account things like AUM and asset turnover. Yes there are asset managers out there that charge 0.25% per year in AUM, but this is by no means the average AUM fee.

The ETF is merely an analog. It’s simply easier to run these calculations using the ETF instead of broad mix of diversified assets and having to compute each one. The ETF probably overstates the overall return versus someone who has a more diversified holdings, and that’s another driver behind the 1% adjustment.

Your assumption on my capital gains adjustment is way off. I assumed 15%. In fact, there’s no way for you to have calculated this because I didn’t give you enough information to calculate it.

This is whole life insurance, there is no surrender fee to a whole life contract. I don’t include taxes because functionally I’m not going to surrender the policy to use its case value. I don’t have a similar mechanism to use cash accumulated in the ETF. If I want access to it, I must cash it out and pay taxes on it. Yes there might be tax loss harvesting that could offset some of the taxes due upon liquidation (either full or partial) that might adjust some of the figures. But whole life doesn’t require any of that to work out in the fashion described. Charitable donations can reduce taxes, but again whole life doesn’t require this additional wrinkle. Step-up at death isn’t applicable to this specific discussion, but keep in mind that whole life insurance pays a much larger than the cash value benefit at death, which is just as tax free as a cost basis step up.

And as far as your suggestion on my unreasonableness, you’re making my point for me. Whole life doesn’t need the “strategies” you’re talking about, which is far more complex. I’m not saying that one shouldn’t do that. But with my years of experience talking to a lot of people about their finances from more than just the insurance slanted side of the discussion, I can tell you very few people care to work through what you’re talking about. If you are, great! If that means you think whole life insurance is inferior and you’d rather spend time working through investment strategies such as the ones you referenced, have fun.