Whole life insurance investment yield on assets is an indicator we use to judge how well the insurer will be able to maintain returns on its cash value products. It’s not a perfect metric, but when we look at it in terms of the general trend, we can make assumptions about how the trend of the cash value products might turn out.

This is especially true for annuities with floating rates and cash value life insurance products and is a great consideration for where whole life dividend rates will go. We know this because a large portion of insurance company profits comes from investment gains—and since dividends are paid out of operational surplus (operating profits) this metric helps us predict the direction of future dividend payouts.

The General Trend is Down

Not surprisingly, the generalized trend for most companies annual yield on assets has been downward. This is driven by historically low interest rates that many fixed investors have bemoaned for the last several years. Based on this fact, we don’t necessarily worry when we see an insurer’s yield trending down; we worry when it starts to trend down at a faster pace than the average.

Methodology

Using the five year historical yield on assets provided by Ebix Vital Signs® we regressed the yields given time to determine an annual move in the investment yield that 23 life insurers known for offering whole life insurance contracts. We used a simple two variable regression as opposed to a compound annual growth rate (though the two are somewhat similar) because we wanted to include any influence a good or bad year may have on the overall five year trend.

In other words, a compound annual growth rate, may under or over report the trend. For example, if the first year was a really bad year and the last year was an okay or good year, it would over report the trend because it ignore the middle three years.

It's also important to note that this is different than the five year average return that we've discussed in the past.

We then ranked all of the companies by trend highest to lowest.

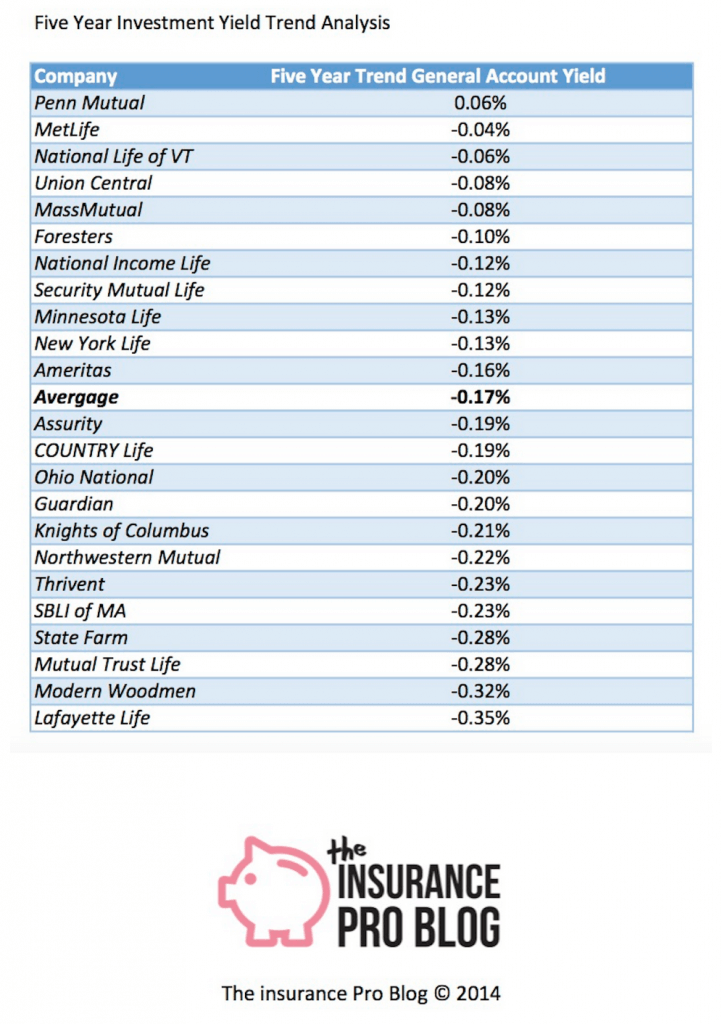

Results

Here are the results from our analysis:

Almost all companies have a five-year trend that is negative—there’s one company with a positive five-year trend. We’re not surprised by this general negative trend given the decline of interest rates.

There are MANY other Pieces to the Puzzle

This trend analysis is helpful as a single variable amongst numerous other variables to consider when selecting an insurance company for whole life insurance, and this becomes especially truer when one focuses on purchasing whole life insurance for cash value. But it’s important to note that it is only one variable and not a deciding variable. There are lots of reasons why a company may seem to have a yield on assets that is declining more rapidly than others, and we’ll be discussing that in more detail in the near future.