Three years ago this past Friday we published one of the most significant blog posts on this web site. This post, and a successor post we published last year remain some of the most popular content we’ve created.

For those unfamiliar with the original article, it reported on real historical data provided by a whole life insurance policyholder who was fortunate enough to purchase a decently designed blended whole life insurance policy back in the early 90’s.

The policy performed remarkably well and we noted originally that the compound annual growth rate of the policy was quite attractive and far greater than all of the typical reporting produced by plain vanilla whole life insurance policies–not a surprise at all.

Last year, we followed this up with a forecast on this whole life policy (unfortunately the data points end in 2009) and noted that it compared very favorable to a passive buy-and-hold stock market investment. This comparison has been lightly criticized for the following two reasons:

On the one hand, it uses forecasted data which diminishes its significance since the data is not empirical.

Second, it’s a comparison against one mutual fund, which would be a highly unlikely scenario (i.e. one would not simply buy one position in one fund and hold that as their retirement plan). I can accept these criticisms, though I think the second argument missed the point.

There’s more to analyze here and that’s what today is all about.

The Portfolios

There are a multitude of portfolios one could pick for the purpose of retirement planning, and I wanted to make a comparison of several portfolios to see how varying degrees of risk exposure compared both to each other and the blended whole life insurance.

I didn’t vet the portfolios in terms of backtested results, but rather took their core strategies as my guideline (i.e. used the theory behind their superiority since we don’t know what the future holds). The three portfolios chosen were:

- The Boglehead 4 Funds

- A portfolio I’ve long personally favored

- A 40/60 stock/bond portfolio

The Bogleheads 4 is pretty self explanatory.

My portfolio is a blend of mostly bond asset classes with large cap growth stocks and real-estate (as an aside, this has a been a portfolio allocation I favored recommending from back in my securities licensed years).

The 40/60 stock/bond portfolio was chosen over the traditional 60/40 split because it’s fairly well known within the investment industry (perhaps not so well known by the general public) that 40/60 has generally performed better than 60/40.

I used the backtesting tools at portfolio visualizer to compute results and compare to the actual historical numbers we have for a blended whole life policy.

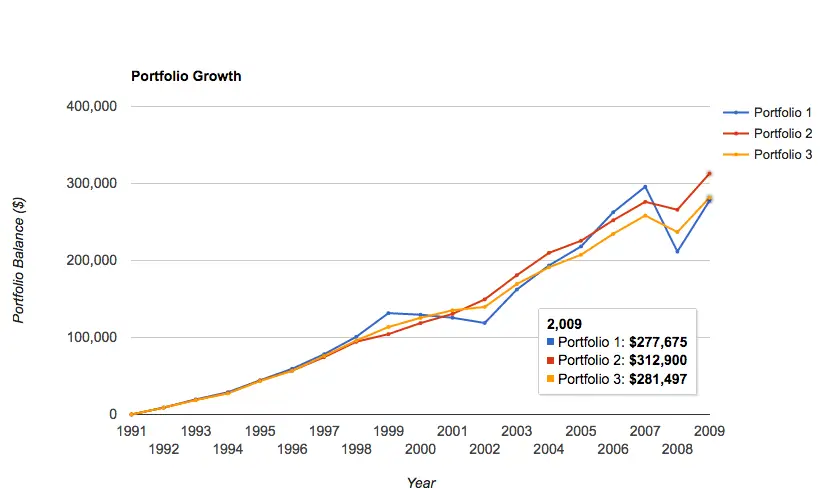

The Results

Interestingly, the worst performing portfolio was the Bogle 4 (the riskiest of the group), and my favored portfolio performed the best. Here’s a screen capture of the results:

But notice that all three portfolios returned less than the blended whole life policy did over the same time period. The blended whole life policy had an ending value at 2009 of $318,661.

Noteworthy Observations

Focusing for just a minute or two on the portfolios, there are some interesting observations to be made.

Perhaps the most interesting (most interesting to me at least) is the fact that my long favored portfolio performed quite well. This has a lot more to do with some interesting statistical attributes than my own personal ego. My favored portfolio has the lowest sharpe ratio of the three (meaning it’s the least risky per unit of return produced), and it also has the lowest correlation with the U.S. stock market.

For those interested in the numbers, they are:

- Portfolio 1 (Bogle): Sharpe Ratio: 0.33 / U.S. Stock Market Correlation: 0.96

- Portfolio 2 (My Pick): Sharpe Ratio: 0.63 / U.S. Stock Market Correlation: 0.76

- Portfolio 3 (40/60): Sharpe Ratio: 0.5 / U.S. Stock Market Correlation: 0.95

Now, these results are squarely in the wake of the 2008 financial catastrophe and one should prudently point out that if we observed time through 2015 we’d likely see different results.

That’s intuitive, give the portfolio with a lot of stock market exposure time to recover. However, the results don’t change very much.

The Bogle 4 and the 40/60 portfolio remain pretty close to one another, and my portfolio pick maintains a substantial lead (approximately $75,000 more than the other two). Analysis metrics (sharpe ratio and market correlation) change slightly in terms of actual values, but relatively speaking, stay the same.

We have argued for years that the risk/return relationship that most people reference has no factual underpinning. There’s an intuitive justification for it, but the empirical evidence clearly disagrees with the theory. This is a core concept behind Modern Portfolio Theory.

Major Takeaways

None of this is intended to make the argument for completely forsaking stock market investing. I don’t believe one should eschew stocks entirely. I would point out, however, that the mix of stocks necessary to accomplish certain long-term-savings goals may be a tad overstated.

Risk is a complex issue all investors/savers face and implementing a buffer to minimize the negative consequences of it can be tricky. The traditional investment tools we hear so much about are all pretty tightly correlated with one another.

As seen above, the difference in stock market correlation in two portfolios that have slight to heavy bond exposure (the Bogle 4 and the 40/60 portfolio) is almost insignificant. A portfolio comprised of less than 25% stocks and roughly the same allocation to real-estate with the remainder going to various bond allocations (i.e. very heavy bonds) is certainly less correlated to the stock market, but is still heavily affected by it.

We can’t overlook the power of life insurance contracts when intentionally designed to maximize cash values. Insurers have done a phenomenal job in managing the assets held in their general accounts and this means serious benefit to policyholders.

The blended whole life policy historically performed the best over this time period and its calculated correlation to the stock market is far different from the other portfolios at 0.19. The calculated sharpe ratio over the same time period for the blended whole life policy is 0.84. This means it has a superior risk-adjusted rate of return when compared to all three portfolios.

It’s important to note that the portfolios analyzed through the visualizer do not account for fees; the whole life policy does. A crude attempt to universally adjust for fees assuming one pays no more than 0.25% of assets (likely to be higher) suggests we adjust the ending values by 2%. It’s also well worth noting that none of these values account for tax consequences.

The whole life policy does not need to contend with taxes since it can accumulate cash values tax deferred and life insurance is far less restricted in terms of annual contribution amount. Executing this savings plan with this planned outlay even given increases in contribution amounts to various retirement savings plans could prove tricky–at least far more difficult than would be the case with a life insurance contract.

Ultimately, long term savings require a certain focus on risk mitigation and diversification. When done correctly, it's more nuanced than most financial advisors are trained for and/or willing to admit. The idea that time affords the ability to make big bets and will “long-term” produce highly favorable gains is a myth with scant amount of evidence to substantiate it.

Stocks still play an attractive role. The volatility of the stock market creates an opportunity to gain, but that gain must come with an absolute lack of immediate need for the money.

It’s also proven to be a poor long term strategy. That’s not to say one cannot gain from owning stocks over long periods of time–one likely can. But numerous alternative portfolios that are far less stock heavy have tended to perform better and provide far better risk adjusted rates of return.

Hi Brandon – maybe I missed it but where is the actual performance and numbers of the blended whole life policy? Do you have it on your site somewhere? It would be nice to see the actual year over year returns. Also do you have more details on your “preferred portfolio”? What exactly is in the portfolio? Thanks

Hello,

The historical values for the whole life policy can be found here.