Podcast: Play in new window | Download

The SECURE Act of 2019 rewrote the rules on inherited IRAs. The biggest change eliminated a Required Minimum Distribution (RMD) schedule for younger non-spousal heirs that allowed them to “stretch” the distribution period out for their lifetimes. The new rules require these individuals to instead distribute all of the money in the IRA within a 10 year period that begins when the original IRA owner dies. This much more consolidated time period forces a lot more money out of an inherited IRA, and should theoretically raise tax revenues for the U.S. Government.

Such changes cause us to re-evaluate IRA strategies and concoct new approaches to build and preserve wealth.

Saving for Retirement with an IRA vs. Whole Life Insurance

The most obvious question that came out of the rule change for life insurance agents was, will the new rule make cash value life insurance products a more attractive alternative to traditionally saving money in an IRA? I suspect a lot of that depends, but for the segment of the population who likes the risk-return parameters of stocks and seeks to buy those stocks inside an IRA, I seriously doubt whole life insurance is an absolute better substitution.

For those seeking to buy bonds–primarily or exclusive through bond funds as most typically investors do–whole life insurance and indexed universal life insurance become more realistic alternatives given their similar risk-return profile to bonds. But that doesn't always mean one should opt for life insurance instead.

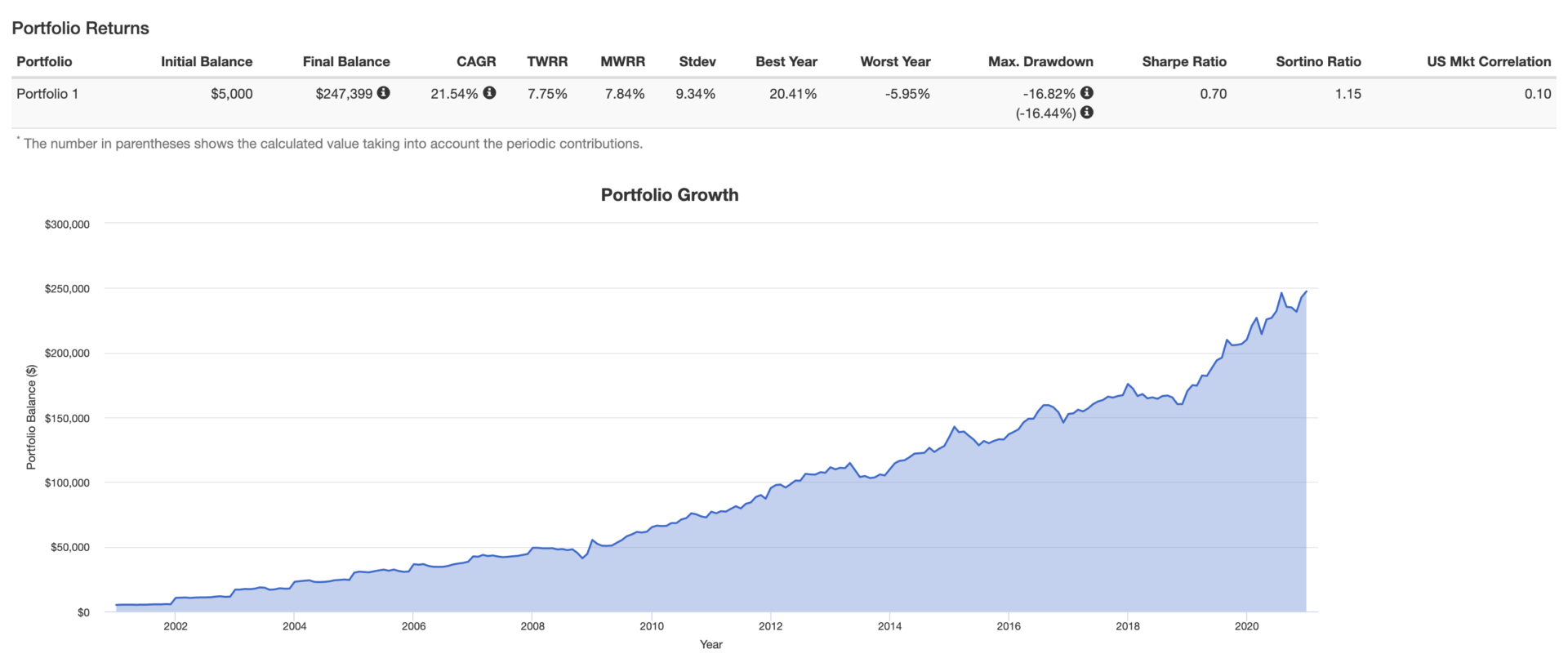

Using a well-designed whole life policy and the Vanguard Long-Term Investment-Grade Fund's (VWESX) historical performance we modeled a scenario putting whole life insurance against an IRA using 100% bond exposure over a 20 year period. The Bond Fund IRA beats the whole life policy in terms of cash value accumulation during this 20-year time period with $159,000 of cash in the whole life policy versus $247,000 in the IRA.

The whole life policy does, however, have a $394,000 death benefit after 20 years, which does mean it beats the IRA in terms of legacy value. It's unlikely, though, that someone in his/her mid 40's–the age assumed in our scenario–would begin saving money in an IRA with the sole intention of passing the money onto another generation.

Incorporating Life Insurance into an IRA Plan At Retirement

It is more likely that someone at or near retirement may earmark money saved as something they wish to leave to a child or grandchild. This was one of the major selling points of the “Stretch IRA” strategy.

What if the individual in our previous example chose the IRA and accumulated the $247,000 in account balance by the time of his mid 60's and decided that this money wasn't necessary for his retirement income needs? If his plans were to figure out a way to maximize the value of this investment as something he passed on to his grandchild, we might be able to create a boost in its value by incorporating life insurance into the plan at this time.

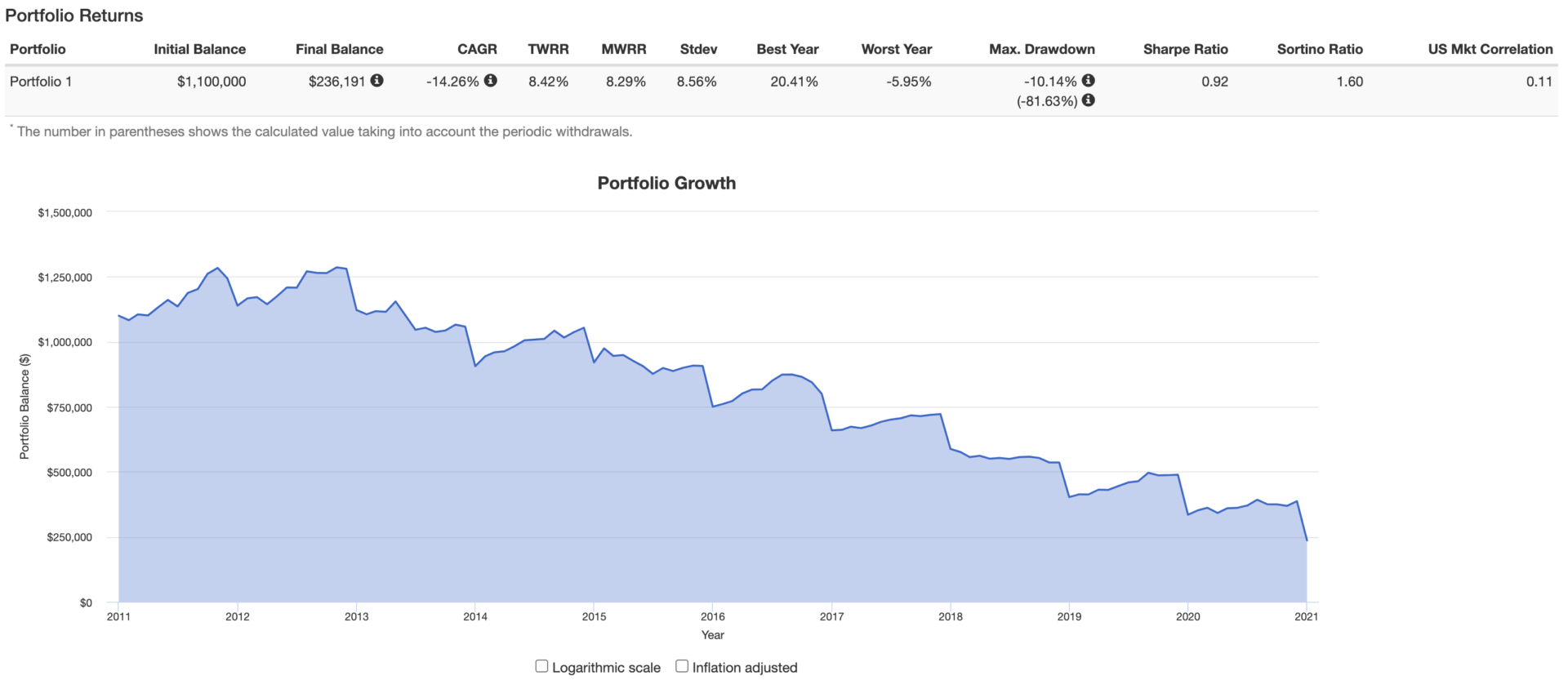

First, if we skip the life insurance discussion, and simply assume that the IRA will continue to grow at the same rate it did over the past 20 years, the IRA account balance should be approximated $1.1 million in another 20 years–the IRA owner is now in his mid 80's. If he dies at this time, he passes a $1.1 million IRA balance to his grandchild who now must withdraw all of the money in the IRA within the next 10 years. Assuming that the beneficiary/grandchild begins withdrawing $150,000 per year from the IRA for 10 years and then withdraws the remainder from the IRA at the end of the 10 year period, he should have netted about $1 million dollars from the inheritance–this is after he pays the taxes due on the distribution. This assumes that he leaves the IRA funds invested in bonds.

If instead, the IRA owner uses some of the IRA money to buy life insurance as part of his plan to maximize legacy value, he might gain an advantage in the following way.

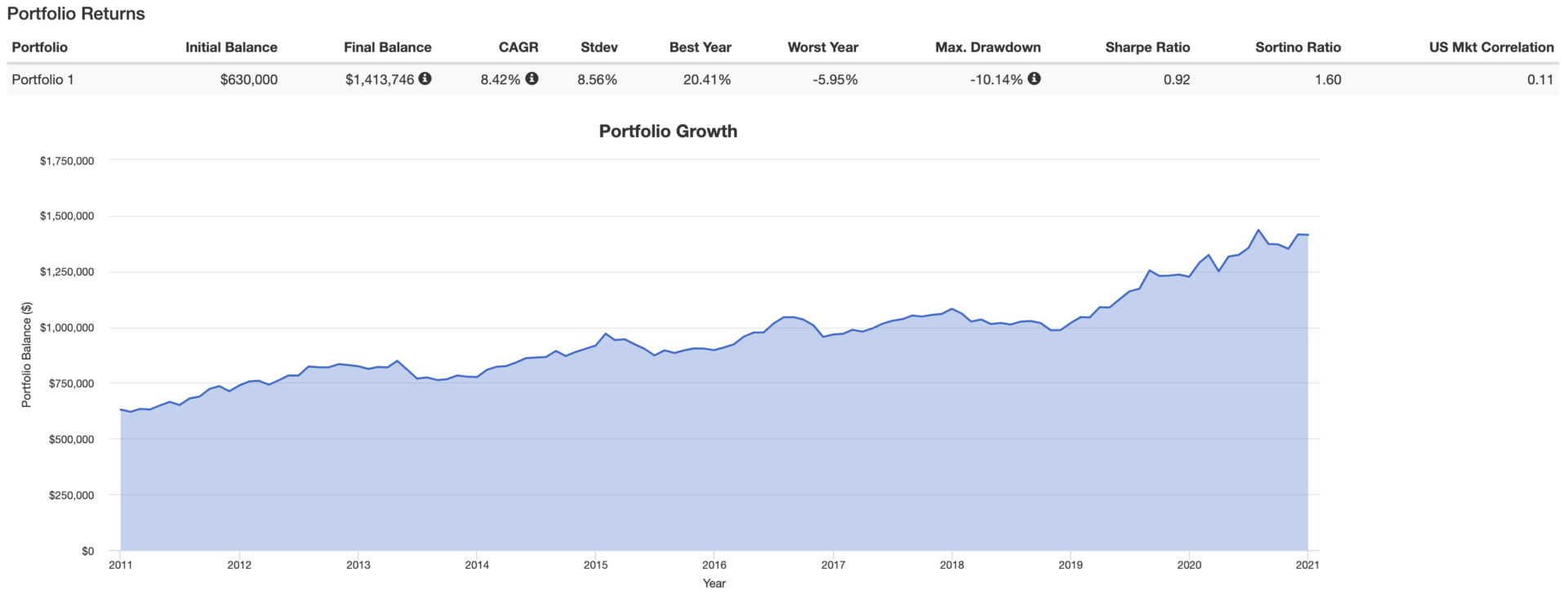

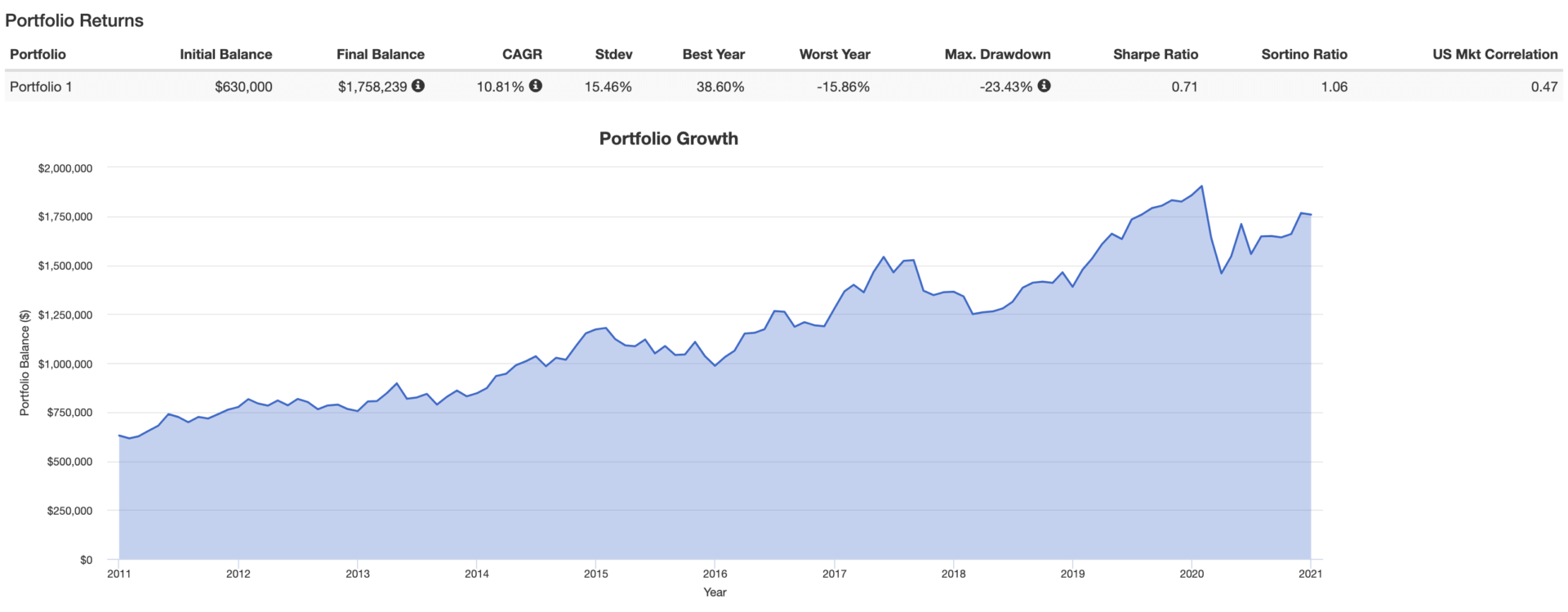

He'll begin by withdrawing enough money to net a $20,000 payment to a whole life insurance policy for the next 20 years. Assuming that he again dies after 20 years, his grandson will receive $240,000 in the IRA and a death benefit of $630,000. The $630,000 death benefit comes income-tax-free with no requirement to withdraw it from an account under any specific timeline.

The grandson is free to invest the death benefit any way he sees fit. He could buy the same bonds grampa did and achieve an account balance of $1.4 million after 10 years.

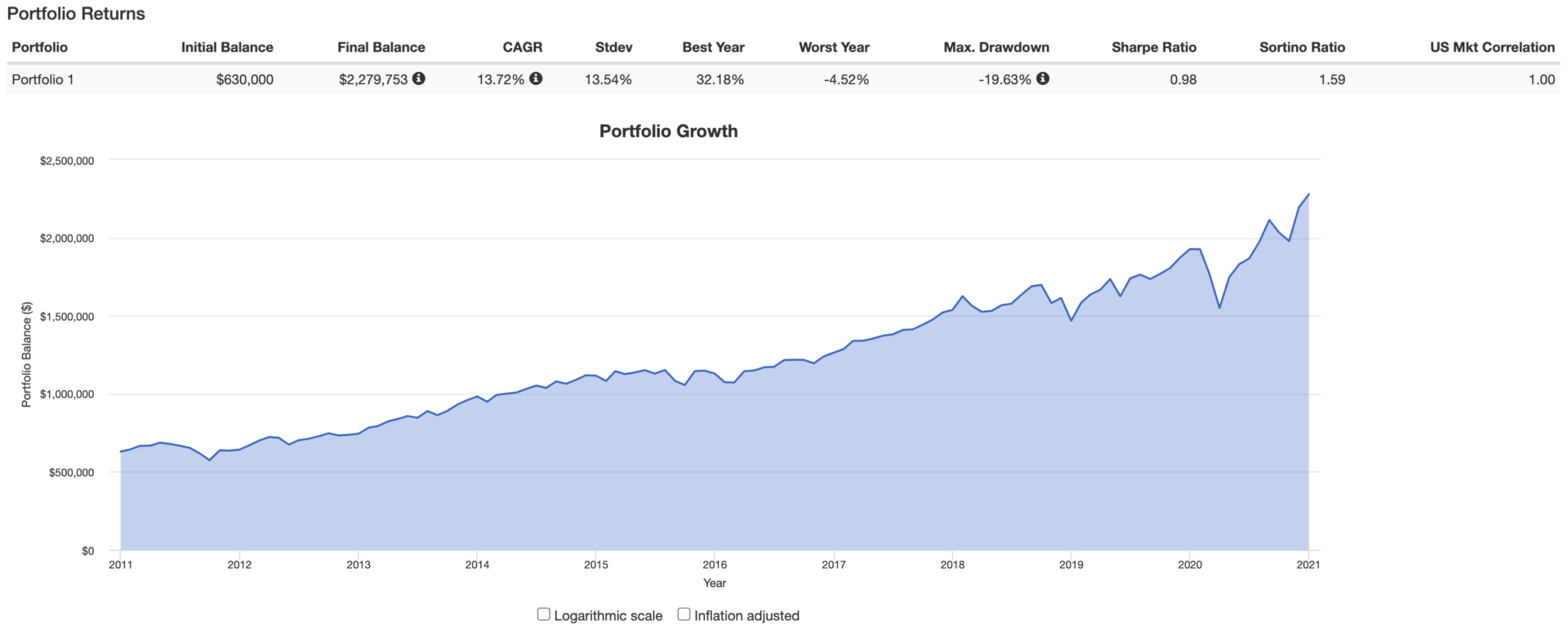

He could buy stocks and have around $2.2 million after 10 years–I used the historical performance of the Vanguard 500 Index Fund (VFINX) to forecast this balance.

Or he could buy some other income-focused investment that grows to $1.7 million in 10 years and is capable of generating $114,000 in annual income from dividends–I used the historical performance of the Reaves Utility Income Fund (UTG) and its current dividend yield to forecast this balance.

None of these scenarios even address the $240,000 that remains in the IRA that the grandchild inherits. This adds to the wealth created by the above-mentioned investment options using the life insurance death benefit.

Bottom Line

There are several ways one could incorporate life insurance to help build and preserve wealth. In the above example, we can greatly augment a $100,000 investment made over 20 years when using life insurance as a complement to a wealth-transfer/legacy plan. It's certainly not the only way life insurance can add value to one's financial strategy, but it certainly highlights one way to overcome the potential wealth lost from the rule changes brought about by the SECURE Act.